- Valuation risks are mounting: The S&P 500 trades at 22x forward earnings, well above historical norms, with Shiller CAPE at 38x—levels last seen before major corrections.

- Equity Risk Premium goes negative: Stocks now yield less than corporate bonds, a rare signal that equities may be overpriced relative to fixed income.

- Regulatory headwinds intensify: Governments are moving swiftly on antitrust and national security concerns, particularly targeting AI and semiconductor exports.

- Investor behavior is shifting: Smart money is rotating from high-multiple tech into quality compounders, emphasizing operational resilience over narrative hype.

TradingKey - With market sentiment shifting from champagne to panic doors in head-spinning tempo, investor sentiment can quickly flip from euphoria to terror. Today’s environment is reminiscent of late-stage speculation, the prices of assets climbing faster than fundamentals can justify, driven by retail FOMO, momentum, and institutional focus.

Best indicator? Multiples that climb into the fantasy world reserved for fairy tales, a goodly number of the largest tech names now trade hands at 22x forward earnings far higher than its 30-year history average of 17.0x and even its +1 standard deviation of 20.2x. This is not your normal risk-on cycle, the kind of thing that makes value investors uneasy and macro strategists dust off long-buried dot-com charts.

.jpg)

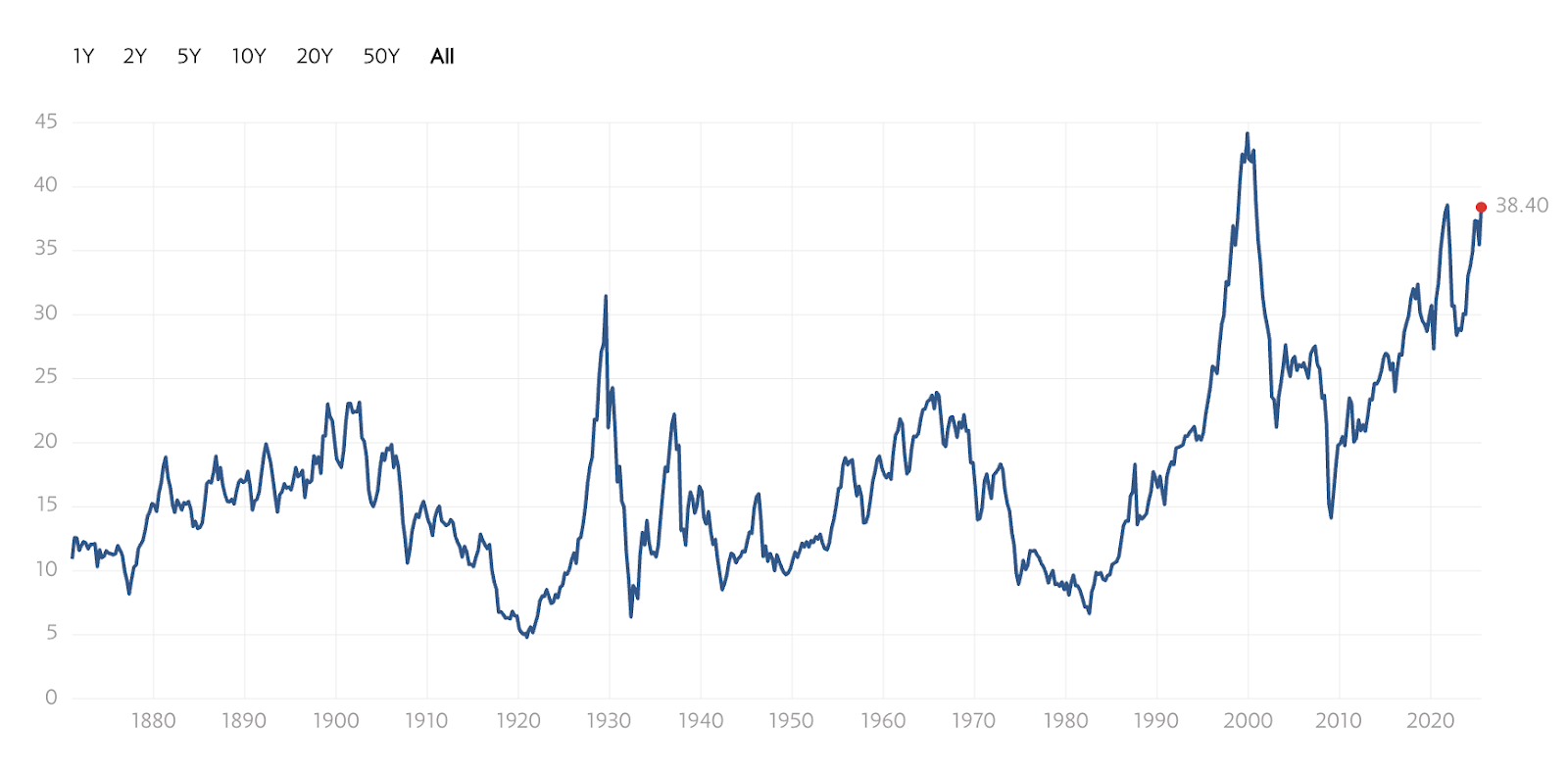

Further, Shiller’s cyclically adjusted price-to-earnings (CAPE) ratio reiterates the warning at 38x versus its long-run history of 28.3x, levels that are normally associated with high valuation risk. To compound the angst is the earnings yield (P/E inverse) going below the corporate bond yield, resulting in an Equity Risk Premium going negative, an unprecedented condition that suggests shares could be overstretched relative to bonds.

Relative to history, however, the current valuation environment is more like the dot-com bubble than the post-GFC recovery. Communication services and tech-heavy sectors remain extremely expensive relative to the broader index, raising concerns of targeted bubbles. Dividend yield is also 1.6%, contributing nothing to passive income attraction.

This setup does not promise an imminent breakdown, but it leaves less room for error. Earnings expansion needs to come robustly and sustainably to justify current prices. Without that, macro surprises, surprise rate hikes, or regulatory pushback can easily trigger a mean-reversion response. Buyers have to be careful: there is still potentially upside, but there is already.

The Risk Beneath the Surface

Even if valuations converge ultimately through earnings catch-up, there remains an equally large lurking risk, regulation. Governments around the world, burned by past failures to restrain tech titans, are now being far more assertive. Export restrictions of high-technology chips, most famously to China, have become political flashpoints. American policy is not only reactive but is now establishing what companies can sell where, and to whom. For companies such as Nvidia, these laws have direct impacts on billions of possible revenues, all by the stroke of a bureaucratic pen.

Regulators across Europe are creating sweeping regimes for platform dominance, user content protection, and algorithmic disclosure. And they're not holding back, hefty fines, interoperability obligations, and outright structural changes are on the table. For investors who ever thought tech to be immunized from the hand of governments, that myth is fast evaporating. Back home, China’s own home crackdowns of its own tech titans, from commerce to schooling, remain sharp reminders that innovation does not grant exemption where national interests are concerned.

From Opportunity to Oversight

Why these risks are even more potent is that they can materialize very rapidly. Correc-tions to valuation come warningly-usually slowing growth, skyrocketing costs, hawkish central banks. But regulation? It falls like an anvil. Some new rule, forbidden transaction, surprise antitrust probe, and the market prices on the spot. For high-multiple stocks where projected cash flows are already discounted based on assumption of perfection, that is no insignificant development. 10% downward revision of revenue estimates can mean 30-50% reduction of share price. We have already seen that. More than once.

That has altered institutional capital's approach to treating mega-cap tech. It is no longer about all-out exits, the vast majority of these companies still print money on insane margins, but about adjusting expectations. Silicon Valley-style unlimited runway for platforms to scale unchecked is no longer being given by the market. It now rewards companies that show operational leverage, regulatory flexibility, and revenue diversification that is not so geography, product, or loophole based.

Here's How Smart Investors Are Positioning

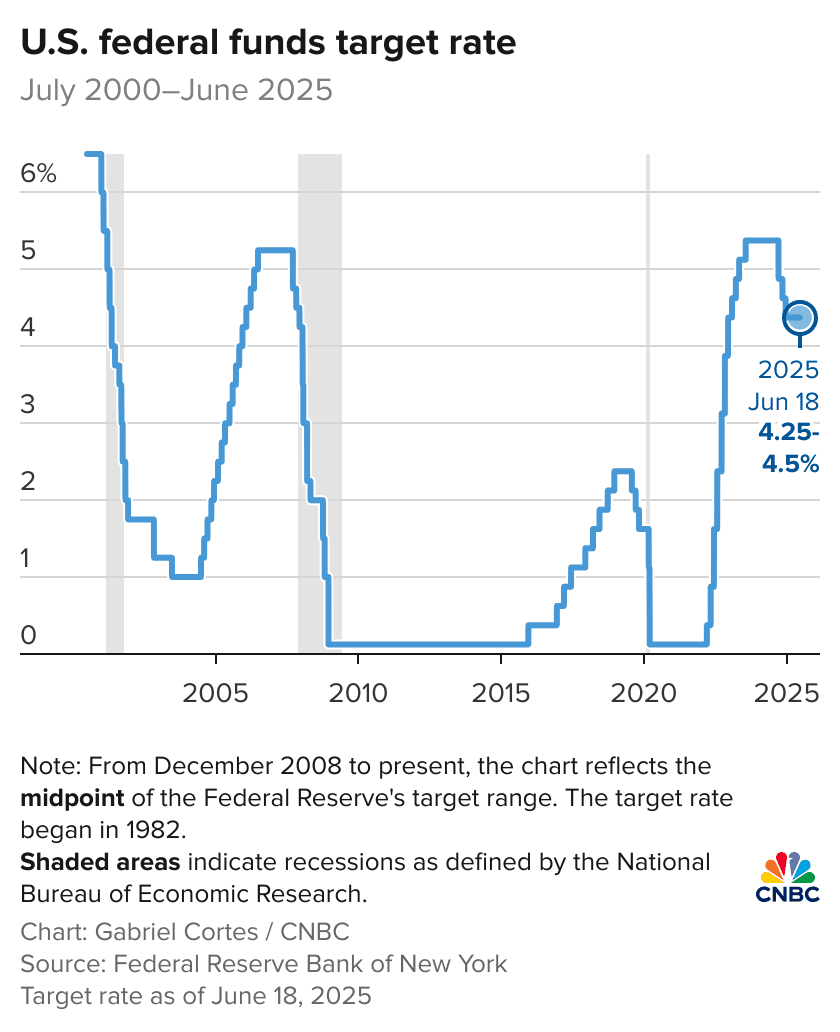

People who have witnessed multiple market cycles would realize that valuation bubbles do not burst because people have lost confidence. They burst because of tightening liquidity or a narrative failing. Both challenges amplify in our time. Although the Fed is not tightening again, the policy remains restrictive. Capital is no longer free. At the same time, the AI-headlined thesis underpinning today’s recovery has scant tolerance for disillusionment. A single earnings miss, adoption slowdown of cloud, or regulatory setback can reverse the narrative instantaneously.

Smart money is not necessarily shorting the market, but rotating. From active trades into quality. From ultra-long-duration growth into compounders that have price power and actual cash flow. From United States-focused exposure into selective internationals where innovation is reasonably priced and policy risk is better understood. Risk-adjusted return now rules narrative-adjusted fantasy.

Source: www.cnbc.com

A Time of Disciplined Conviction

None of that means that tech is not worth investing in. Quite the opposite. There is an innovation process. AI, edge computing, productivity of automation have the potential to rival past industrial revolutions. Markets, however, are given to exaggeration, and that is where you show caution. It is easy to purchase greatness. It is harder to invest anything for what is great. Investors who balance conviction and discipline, optimism and risk-awareness, are massively better able to compound in the long term. History has ever rewarded the prudent and punished the greedy. This one won't prove an exception.