- Wealth isn’t built on moonshots, it's sustained by capital discipline and risk protection through cycles.

- Smart allocation is purposeful, not passive, each dollar must serve a role: offense, defense, or optionality.

- Downside protection, rebalancing, and behavior-aware investing are compounding tools, not just safeguards.

- Liquidity is not laziness, it’s strategic patience that fuels opportunity when volatility strikes.

TradingKey - It's easy to fall in love with the positives of investing in, 10X stories, decade-long compounders, as well as moonshot bets that make headlines. But long-term wealth isn't built upon that which you hold near the top. It's built upon how you invest capital and more importantly how you defend it when tides turn. In volatile markets as well as converging macro cycles, it's your allocation framework as well as protection for the downsides that get you stay in the game, compounding regularly while everyone otherwise rings up Homers.

This isn’t a lecture on defense. It’s a conversation on framing up your offense so it won’t shoot itself in the foot. Allocation of capital is the road map that guides your money into places that it’ll grow. Risk management of the downside is protection that keeps it from a bad break wiping out years of gains.

The Foundation: Strategic Capital Allocation

Let's start with the foundation, your capital allocation process. Strategic allocation isn’t just spreading money across categories. It’s about putting each dollar to work with clear intent, aligned with your personal timeline, income profile, and goals. A 35-year-old founder with non-predictable income and a long runway will manage capital deployment very differently from a 60-year-old with a short runway to a transition to retirement, even if they share similar levels of net worth.

One possible modern model of allocation might split capital equally between equities, fixed income, real assets, private investments, and cash. Equities supply growth with drawdowns. Bonds provide stability and income, especially in higher rate markets. Real assets in the guise of real estate or infrastructure insulate from inflation while producing uncorrelated cash flows. Cash is underutilized but dry powder, ready to be spent on dislocations.

That's where intentionality comes in. Allocating 50% to equities doesn’t mean blindly buying index funds and hoping for the best. It could mean incorporating a layer of factor exposure (e.g., quality or low volatility), being anchored with a GARP-type blue chip stock, or concentrating on secular growth plays in assigned risk buckets. Allocation is intentional when it makes each dollar belong to a purpose: offense, defense, optionality, or income.Without that, portfolios end up being a hodgepodge of trades.

.jpg)

Source: b2broker.com

The Art of Downside Protection

Most investors concern themselves with gains maximization, yet they tend to forget that capping losses has a more significant long-term impact. A 50% decline requires a 100% return to break even. That simple mathematics should reframe risk in our thinking.

Downside management isn’t being afraid. It’s thinking about what will go wrong without freezing up your ability to be a participant for the upside. This is where a stop-loss, a position sizing, hedging, and a cash buffer come into play. It also involves being certain about a max drawdown tolerance long before you ever get into a position.

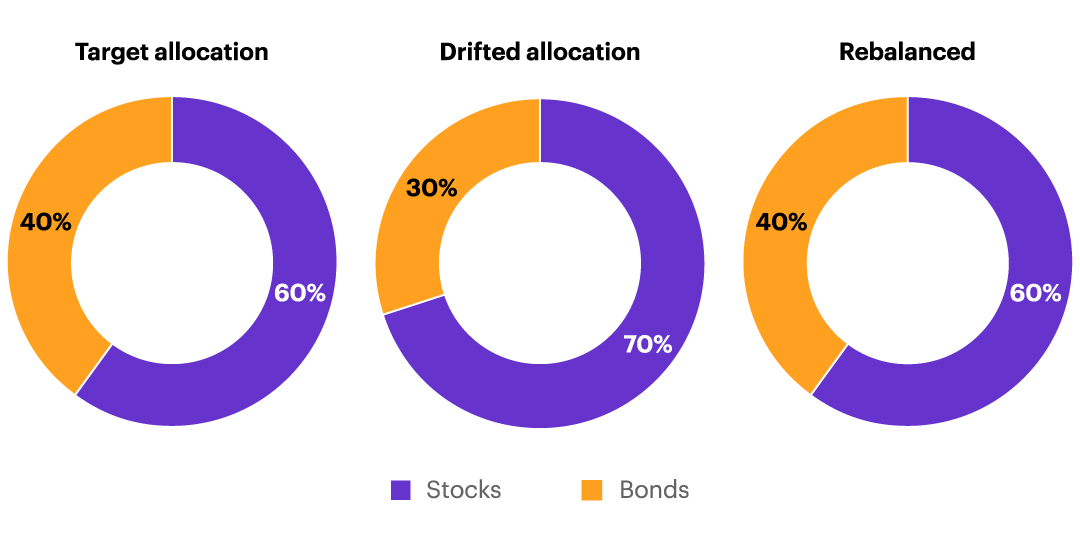

One of most under-appreciated bottom-down tools? Rebalancing at the asset level, systematically buying underperformers and trimming winners, helps enforce discipline and keep portfolio risk in check. In the long game, that small behavioral edge compounds.

Some go looking for put options, tail risk hedges, or structured products that limit upside for limited-downside protection. Highly advanced as they are themselves, these instruments are no more effective than the system behind them. No strategy replaces sound judgment. The time to build defenses is during calm markets, not amid a storm.

Source: us.etrade.com

Behavioral Allocation: The Human Factor

Even a beautifully formed portfolio can be put in danger if a panicky investor in command is confronted with volatility. That's when behavioral risk management enters. It isn't sufficient to create a portfolio that's good with numbers. It must be created for you, your personality, your quirks, your tolerance for emotional fray in a 30% drawdown.

And for some that means allocating excessively to cash in risk-off scenarios even if underperforming. Others establish auto-pilot regimes: rebalancing algorithms, pre-programmed macros for reduction or addition in turbulence, and bucketing (e.g., “core” vs. “explore”) that separates speculative from long-term funds.

The goal isn’t outperforming the market in every stage. It’s being invested long enough, without blowing up, to enable compounding to do its stuff. Behavioral risk management helps ensure your own emotions don’t become your portfolio’s biggest threat. Very often, the superior allocation decision of capital is one that makes it comfortable for you to sleep peacefully at night.

The Optionality of Liquidity

Liquidity is one of the most poorly comprehended forms of capital. Investors delude themselves into thinking that it's inactive to hold cash. However, liquidity, when strategically held, is optionality. It provides flexibility to do something when markets incorrectly price securities. It moderates involuntary sales. It's what makes being able to buy the dip different from being eager to buy it.

Especially in stressful times, i.e. 2020, 2022, or any black-swan shocker, liquidity delivers asymmetric value. In a stampede for funds, a long-term investor waits to profit from fire-sales. Maintaining 10-20% in short-term T-bills or high-yield savings accounts isn’t market timing, it’s being prepared.

The idea is to set aside that dry powder out of emotional capital. That cash shouldn’t chase FOMO rallies, it’s meant for moments when markets misprice opportunity. It is reserved capital spent as a strategic military tool, not a tactical one.

.jpg)

Source: www.statista.com

Managing Risk Across Time Horizons

One of the more overlooked dimensions of capital allocation is time. Not all capital must be for the same duration. Funds may be needed in 1-3 years (liquidity-intensive), while other buckets are built for a 20-30 year time horizon for compounding (risk-optimized).

When you match assets with both expected and unexpected liabilities, your likelihood of being pushed to liquidate risk assets in falling markets shrinks. This time-related approach is exactly what most institutional allocators do most of the time: liability-driven investment. It works equally as well for individuals.

And if it involves a drawdown risk, time is in your corner if you get it right. A 30% drawdown stings far less if you won’t need that capital for a decade. But it is calamitous if it covers your costs next year. Time-match durations. Avoid forced liquidations. That is risk control.

Final Thoughts: Sustainable Compounding versus Hype around Returns

In our noisy markets today, risk management for the downside and capital allocation might be unsexy stuff, until they're all that stand between you and an irreversible loss. It is that hidden alpha that never makes a newspaper headline, yet powers long-term wealth. Think of allocation as being your playbook, and risk management as being your defense line.

Both of them allow you to play offense without popping your balance sheet. They keep your emotions in check, capital strong, and process repeatable. Since the true edge isn't necessarily about finding that next 100-bagger. It's about devising a system that enables you to stand upright long enough to be in possession of one when it does.