- Market volatility is inevitable, but layering multiple hedges, from diversification to options, reduces the risk of severe drawdowns.

- Traditional hedges like bonds are less reliable today, making safe havens such as gold and tactical volatility instruments more important.

- Active management and hedge funds provide flexibility to pivot across asset classes when macro shocks hit.

- The most resilient portfolios combine redundancy and adaptability, turning volatility into a navigable, and sometimes profitable, force.

TradingKey - Every investor, whether an experienced hedge fund manager or a new player with a brokerage app, eventually runs into the world of volatility. Markets do not move in linear fashions, but rather lurch, dip, spike, and then fall again without notice. International events, changes in the economy, and geopolitical shocks all act to put investors on alert. But rather than turn and run from this volatility, savvy investors plan for it, putting together strategies to ease the impact. It is not a question of investing in a lone silver-bullet hedge but of interweaving multiple levels of protection, each of them addressing various dimensions of risk.

This approach, blending diversification, derivatives, safe-haven assets, and active management, doesn’t eliminate volatility. Nothing can. What it does is transform volatility into something survivable, and in some cases, profitable. Much like a ship using multiple stabilizers to stay upright in rough seas, a portfolio with several hedges can continue its journey even when waves hit unexpectedly.

The Bedrock of Diversification and Risk Parity

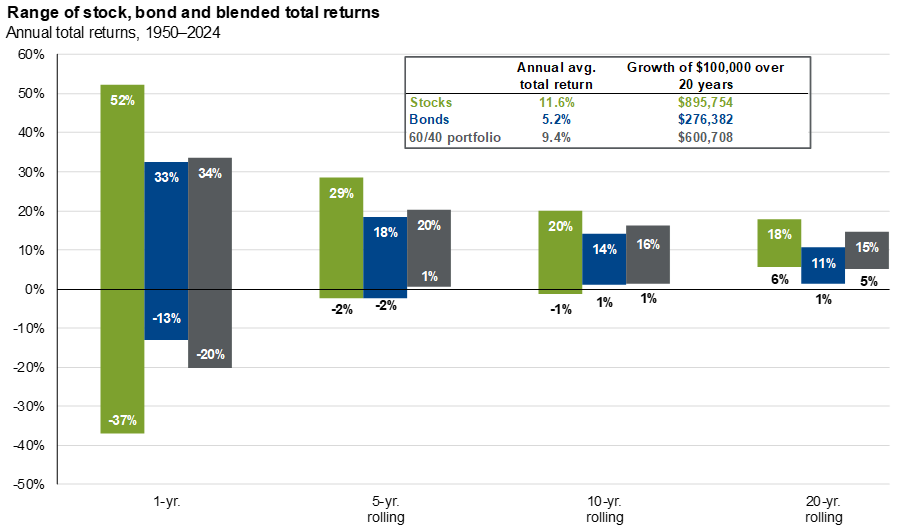

Diversification is the oldest and most tried-and-true form of hedging. Diversifying investments into multiple classes of assets such as equities, bonds, property, and commodities makes an investor less dependent on a specific market outcome. It's a pretty basic piece of reasoning: an asset can tank, but another can come back. But traditional diversification, though efficient, is no longer enough in an age of ever-more globally interlinked markets. Equities can suffer a sell-off and drag bonds with them, leaving seemingly diversified holdings more exposed than a manager had desired.

This is where more sophisticated methods such as risk parity enter the picture. Unlike traditional diversification, which frequently balances holdings by dollar value, risk parity allocates capital by volatility contribution. That translates in practice to more exposure to low-volatility assets such as government bonds and less to high-volatility ones such as stocks. Equating each component’s risk contribution, portfolios are more robust to a single segment’s outcome overwhelming others.

Derivatives as Tools for Control

For investors who are prepared to move beyond the essentials, derivatives represent an elaborate way of managing market fluctuations. Options, for instance, can act like an insurance policy. Purchasing a put option lets a buyer of stocks sell the stock at a specific rate, and essentially place a floor below potential losses. More elaborate structures, like collars, pair puts and calls to establish a bottom and a cap and determine a range within which returns may fluctuate safely.

Beyond options, there are instruments designed specifically for volatility itself. Volatility swaps and variance swaps allow investors to trade the expected level of market turbulence directly. These tools are not about betting on whether stocks will rise or fall but about whether the ride will be smooth or bumpy. For portfolios exposed to large downside shocks, such instruments can serve as cushions during market panics. Futures contracts tied to volatility indexes, like the VIX, are another way of hedging, often spiking in value when traditional equities plummet.

Of course, derivatives are not without cost. Options premiums and swap pricing eat into returns, especially if markets stay calm. But the point of these tools isn’t to maximize profits in placid waters, it’s to ensure survival when the storm hits.

-32142a25fd1f453d8ecc0a376e2d36a6.jpg)

Source: https://www.cmcmarkets.com

Market-Neutral and Non-Direct Strategies

All hedges do not depend on speculating where the market will move to next. Some aim to neutralize market direction entirely. Equity market-neutral strategies are a perfect case in point. Equally weighted long and short positions are taken by these strategies to neutralize the performance of individual securities and to eliminate general market movements by cancelling them out. If the long position appreciates more than the short declines, the investor earns money irrespective of whether the overall market goes up or down.

Arbitrage strategies work similarly. Merger arbitrage, for example, profits from pricing inefficiencies when a company is to buy out another. When the overall market is in turmoil, the potential for profits from the discrepancy in offer price and current pricing can be kept relatively insulated. These strategies will not result in huge windfalls, but they provide stability when direction-driven funds are shaken by volatility.

The issue is implementation. Non-directional strategies are skill-intensive, resource-intensive, and disciplined. But to investors who do have access to them, they provide an important additional layer of protection in uncertain times.

Safe Havens and Tactical Tools

For ages, investors have sought refuge in so-called safe-haven assets when the unknown appeared to be looming. Gold has been the classic example, deemed valuable not because of its return but because it will maintain value when currencies and markets weaken. In recent decades, oil has served the same stabilizing function, providing a hedge against inflationary shocks and geopolitical interruptions. Government bonds, even the prudent balance to equities, still play a major role, though their dependability has suffered in an age of low rates and high debt.

Along with these classical refuges, new tactical tools have come into play. Volatility exposure accessible through exchange-traded funds connected to the VIX offers direct exposure to volatility spikes when equity markets fall. Defined-outcome ETFs, another new creation, construct exposure with in-built buffers or caps so investors can enjoy the upside while capping downside. These products, while peripheral, are the new-age arsenal at the disposal of those who want to hedge portfolios off volatility.

The value of safe-haven assets is psychological more than economic. They offer a ballast, which helps to reassure investors that a portion of the portfolio will be steadfast when all else trembles. That reassurance frequently averts the panicky decisions that make bad things worse in the markets.

-e67861cee8d5444ca6cb3d1f7a7ae48d.jpg)

Source: https://econofact.org

The Role of Active Management and Hedge Funds

Though passive investing has been the name of the game for most of the past decade, bouts of volatility cause investors to recall the importance of active management. Active macro managers and hedge funds excel in periods of turmoil because they are built to be agile. The funds can switch currencies, interest rates, stocks, and commodities quickly in a changing dynamic. Some of these funds are global macro managers and make money off of huge-scale economic developments and not stock-specific movements. Others are event-driven managers and make money off of corporate events or changes in policy.

For institutional investors, allocating to hedge funds has once again become attractive, not just for returns but for their role in dampening portfolio volatility. Their ability to pivot quickly, often using leverage and derivatives, provides an agility that traditional asset allocations lack. While access to such strategies can be limited for retail investors, their resurgence underscores the point: in uncertain markets, flexibility is an asset in itself.

Why Multiple Hedges Count

The major pitfall of most investors is over-reliance on a single hedge. Gold-only investments can fall behind when the economy is expanding. Option-only investments will lose money when markets are calm. Sole reliance on bonds is no longer a guarantee of safety, especially when rates skyrocket. Each hedge is a correction of one risk but an exposure of others.

The real strength is in layering. Diversification distributes exposure widely, risk parity keeps things balanced, options limit losses, volatility instruments earn from choppiness, and core holdings moor portfolios amid shocks. Active management then brings it all together with the ability to react to singular events. Layering doesn’t make for a perfect umbrella, but it sharply diminishes chances of unprecedented drawdowns. It’s the choice of being tossed aside by a hurricane vs. enduring it with some distress but still afloat.

Looking Ahead

Volatility will never vanish from markets. In fact, the interplay of globalization, geopolitics, and rapid technological shifts almost guarantees more frequent surprises. For investors, the choice is clear: either endure volatility unprotected, or build portfolios designed to absorb and adapt to it. The latter doesn’t just preserve capital, it preserves confidence, allowing investors to stay invested rather than sell in fear. Multiple hedges aren’t paranoia, they’re planning.

They understand that no single approach is totally air-tight and resilience is found in redundancy. When markets are free to swing sharply within a matter of a couple of hours, that redundancy is a necessity, not an option. It’s the investors who think this way who will not eliminate volatility but will learn to cope with it, transforming the unknown into a source of strength.