- Focus on financial stocks with solid balance sheets, stable earnings, and strong capital ratios.

- Prioritize undervalued names using P/E, P/B, and ROE to gauge quality and pricing.

- Monitor macro trends like interest rates and regulations that heavily influence the sector.

- Diversify across sub-sectors—banks, insurers, asset managers—for balanced exposure.

TradingKey - Choosing high-quality financial stocks is something greater than opting for leaders or high P/E multiples from the headlines. The finance sector, banks, insurers, asset managers, and fintech businesses, shares extraordinarily diverse structure and business-cycle sensitivity. Yet, at all levels of all verticals, there are, at all times, common qualities worth considering: cushioned capital buffers, repeat revenues, and conservative underwriting or lending behaviors. Investors looking to build an enduring allocation must first look at the economic engine of the business.

In banks, this would mean looking at net interest margins and return on tangible equity. For insurance businesses, underwriting ratios and float management are more indicative. For asset-light fintechs, customer cost of acquisition and gross profit retention offer better indicators than vaunted user growth on its own. The common thread here is clarity: how predictable are the revenues, how sustainable is the core business, and how prudent is the management team at deploying capital?

Not all growth is created equal. Sometimes, financial businesses enjoy stellar topline growth and hide weak profitability beneath. Others, local banks or specialized insurers, grow slowly but cumulatively over decades. The solution lies in taking measurements of earnings persistence, credit discipline, and visibility across the balance sheet, and not quarter-to-quarter metrics.

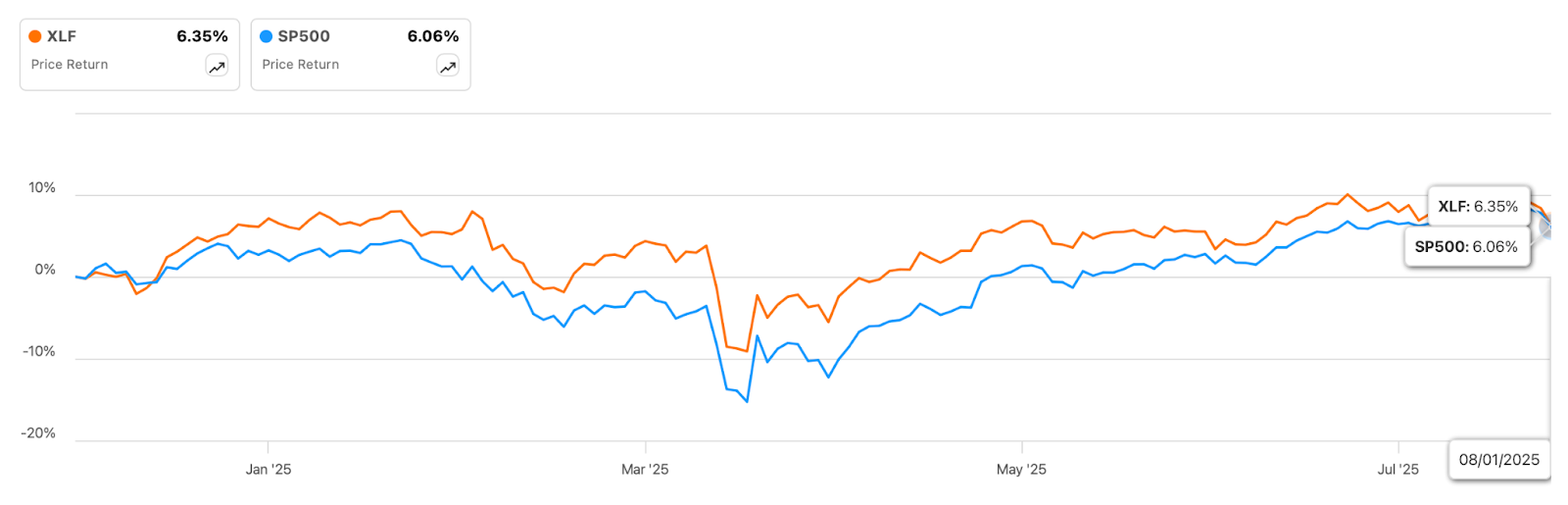

As of August 1, 2025, financial stocks (XLF) have delivered a year-to-date price return of 6.35%, slightly outperforming the broader S&P 500 index’s 6.06% gain, highlighting stable investor interest in the sector despite intermittent volatility earlier in the year.

Source: https://seekingalpha.com

Understanding Valuation beyond the P/E Ratio

Good work on valuation does something better than quote the trailing P/E multiple. In certain businesses, there are substitute metrics that provide better insight. For example, banks are better valued using price-to-book (P/B) or return on equity (ROE), and insurers are regularly traded using price-to-embedded value or combined ratios. Fintechs, on the other hand, justify higher multiples if they themselves are platform businesses with SaaS-like margin growth ahead.

Investors' valuation benchmark should be not then-current metrics, but normalized cycle earnings. A 1.1x book value bank can be dull alongside a 15x sales fintech, but if the bank produces 13–15% ROE consistently with disciplined exposure to risk, it could be offering a better long-term compounding proposition.

Valuation too needs to be contextualized. A high multiple would be justified if supported by secular tailwinds (like digitization or rising financial penetration), but an inexpensive one may be concealing unseen risks (like poor allocation of capital or vulnerability to risky geographies). Relative valuation, an apples-versus-apples comparison of an organization with peers and also with its own history range, adds depth to the story and thwarts fraudulent deals or over-hyped trends.

The Role of Interest Rates and Regulation

Finance sectors rise and fall on macro cycles, majors of which are rates and regulation. Comprehension of how each sub-industry responds to them can provide an understanding of both threat and opportunity. The increase of rates has the benefit of making banks' profitability grow as it widens net interest margins but injures lenders of mortgages or bond-based insurers. Volatility rates, on the other hand, can reverse market-sensitive streams of income on asset managers.

Regulation also controls or catalyzes. The 2008 regime made rules tighter, specific for big banks, and thus minimized risk but also compressed profitability. Fintechs, meanwhile, worked predominantly in greys, recording minimal regulation but now under increased supervision around the topic of lending activity, data usage, and local financial products. The further development of the digital standards of governmental control over the stablecoins or AI-based systems of making decisions will identify the winners and losers of the next decade.

There's also a lesson here for investors: Pick finance stocks whose management understand the regulatory environment and actively take steps to deal with it. Those businesses that think of being compliant as an asset, as opposed to something to be ticked off the checklist, will be better in the long run than others.

Source: St. Louis Fed

Seeking Quality amid Volatility

Durability has got to be the most underappreciated trait of quality finance stocks. In crisis-prone businesses, quality resides just as much in the poor as the good months, and it equates to stress performance. The stocks that withstand credit downtimes without capital dilution, increase book value at an even pace and without shareholder dilution, and emerge from regulatory turbulence better and stronger, those are cycle stocks to own.

Investors must be alert to history of crisis performance, management commentary consistency, and return of capital discipline. A business that buys back shares at low stock prices rather than issuing stock for empire building remains a long-term alignment indicator. Here, the goal is to develop a portfolio of financial names where valuation remains reasonable, return is repeatable, and surprises, where they happen, are mostly to the upside.

In this hyperactive world of disruptive technology, dollar volatility, and global regulation, the quality bar continues to rise. So does the reward for those capable of separating durable compounding machines from PR-seeking hype. Pragmatic exposure to quality fundamentals at sensible prices has absolutely nothing to do with calling the cycle, and has everything to do with owning the right economics, and the right custodians, come the settling of dust that inevitably arrives.

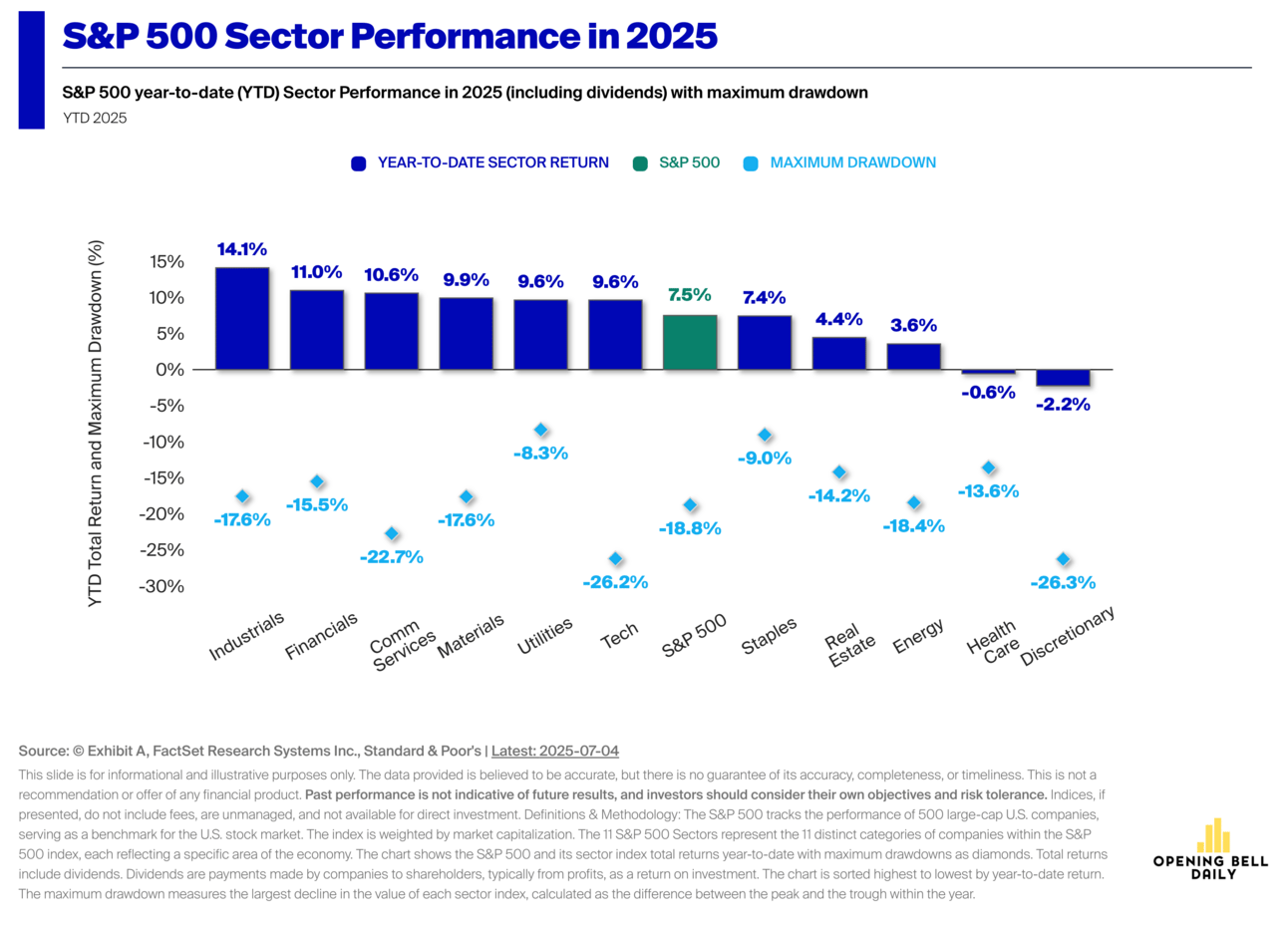

Thus far in 2025, finance stocks have rebounded 11% year-to-date and are one of the S&P 500's top three best performing sectors as they worked through a 15.5% maximum drawdown, showing stamina and investor enthusiasm for the sector's earning potential.

Conclusion

Picking high-quality financial stocks is all about finding a balance between fundamentals and valuation discipline. In a transitioning macro backdrop, there is a need to focus on healthy balance sheets, consistent earnings, and fair value. Along with proper management of risk, this approach offers stability, income, and long-term growth possibilities, and thus the financials belong to a full portfolio.