- Broadcom quietly powers AI's backbone, leveraging custom silicon and hyperscaler ties while adding diversification through high-margin software like VMware.

- Apple and Tesla are embedding AI into products, turning iPhones into smart assistants and vehicles into autonomous, robotics-powered platforms.

- Microsoft, Amazon, and Google are scaling AI infrastructure, each taking a different route—Azure and Copilot, AWS and chips, Gemini and full-stack integration.

- Nvidia remains the keystone of the AI revolution, owning the data center GPU stack and monetizing both hardware and orchestration layers across the AI economy.

Broadcom: The Silent Back of AI

TradingKey - Broadcom has quietly become one of the most important players within the AI hardware ecosystem. It does not dominate the headlines as Nvidia does, but its penetration goes very deep. Its custom AI chip business is thriving by volume, and its hyperscaler relationships, including Google, Meta, and Apple, give it fixed seats within the inference and training workloads. All that chip growth is supplemented by its own high-margin software business, including its VMware purchase, to give an unusually diversified tech giant.

There are, however, risks. Investing in China has become a geopolitical minefield, and custom silicon, as its scale goes, does not enjoy the type of price power that Nvidia does. But investors are betting that Broadcom can address all levels of the tech stack and drive sustained EBITDA growth, and ultimately, a premium re-rating.

.jpg)

Source: simplywall.st

Apple: A Product Life Cycle with an AI Twist

Apple does what Apple does best: building an ecosystem that makes money. As its iPhone growth slows, everyone is holding its breath as it adds AI to the next refresh cycle. As Apple Intelligence and on-device AI models power everything from Siri to productivity, Apple is quietly innovating its experience layer. It’s not out-engineering OpenAI, the latter is creating seamless AI that works.

That alone is a competitive moat. Apple’s prioritization of privacy also protects it from regulatory flare-ups that threaten data-starved competitors. iPhone 17 is the first real measure of consumer desire for embedded AI, and investors are watching whether AI-powered upgrade cycles soar or sputter.

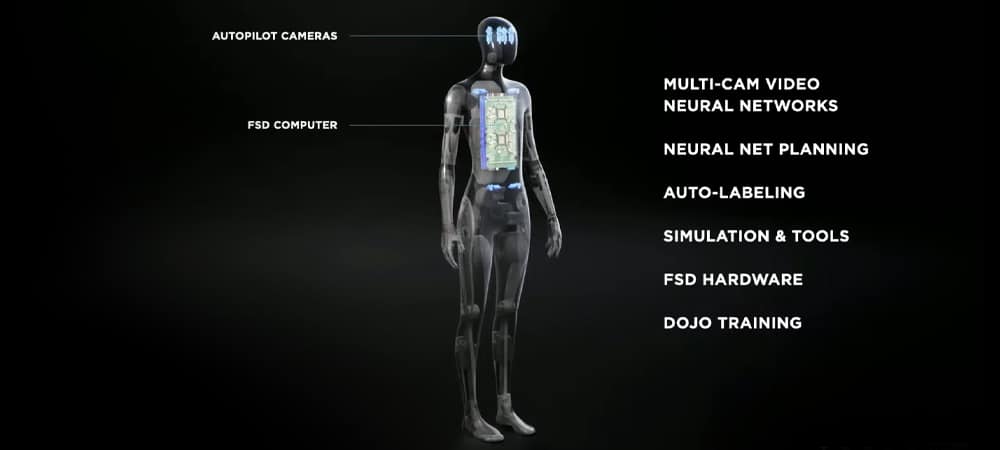

Tesla: AI Robotics Bet is Now

Tesla is no longer just a carmaker. That’s Elon Musk’s ruling as the automaker increasingly transforms into an AI business that is leadership-focused on autonomy and robotics. Full Self-Driving (FSD) is seeing better adoption, and Grok, the xAI chatbot being developed by Musk, is seeing direct deployment into Tesla’s car stack, creating an AI-native user experience.

The market, however, is divided. Bulls consider Tesla as the only vertically integrated AI-robotics play, untapping monetization possibilities of Optimus as well as energy storage. Bears fret about deteriorating car margins and regulatory headwinds. Nevertheless, Tesla has moved on from car sales to monetization of intelligence setting up for the long AI play.

Source: metamandrill.com

Microsoft: Platform Strength for AI Arms Race

Its strength is its end-to-end AI leverage. From its cloud of Azure to its deepest embed of OpenAI models within enterprise applications, it has become the underlying layer of infrastructure for AI deployment across the globe. And that’s beginning to manifest in numbers: double-digit, steady growth for Azure, all-time cloud bookings, and widespread Copilot adoption across Office and developer applications.

Their only problem? Market saturation. As everyone scrambles to put on AI, Microsoft’s challenge is that of differentiation. That’s why fast vertical mergers are its priority – healthcare, schools, government – and trimming underperforming hardware bets. This is no longer growth for growth’s sake. It's a hyperscale profitable AI.

Meta: The Ad Engine Meets AI Ambition

Meta is executing one of the sector's most aggressive AI capital investment plans. Its more than $60 billion CapEx roadmap for this year is reflective of its vision: not only supporting ads with smarter models, but controlling open-source AI, LLM stacks, and metaverse-related platforms. Its own custom silicon, made up of its own AI chips that it has designed, is aimed at reducing its reliance on third-party vendors and enhancing efficiency.

However, there are challenges for the firm. Reality Labs continues to bleed, and regulatory scrutiny from EU as well as US watchdogs is anything but easing off. But the core business is going great. As long as that flywheel keeps going, Meta’s AI push is viewed more as an infrastructure play for the longer term but less of a moonshot.

.jpg)

Source: www.statista.com

Amazon: The Shovel Seller of AI

While everyone is racing after front-end applications, Amazon is all-in on AI infrastructure. AWS dominates the world cloud market, and its own chips, Trainium and Inferentia, are designed not to compete with Nvidia, but to sell below that to hyperscale users. Add Anthropic, Amazon’s largest external AI bet, to the equation, and the strategy is simple: build the gear that everyone needs to use to get AI out into the world.

Retailer margins are narrow, but Amazon ad business is thriving. And AWS still provides most of the profits. When AI is as pervasive as forecast, Amazon is going to be the tollbooth taking revenue for each deployment, all of them, either through compute, or through APIs, or through models.

Google: AI-First or Playing Catch-Up?

Google entered the AI business early but maybe too late to productize. Bard’s rocky rollout gave its competitors time to catch up, and its cloud business, although growing, still lags behind AWS and Azure. Google is still not out of the race, though. Its Gemini models are rapidly maturing, and its AI development kit for developers and companies is becoming ever more formidable.

Its own large pivot is integration. Gmail, Docs, Android, and search being Gemini show that scale-distribution focus is what its full-stack approach is based on. Model strength can turn into user utility for Google if it does work, and the valuation premium that it once had could return. Until that does, caution is still deserved.

.jpg)

Source: businessinsider.com

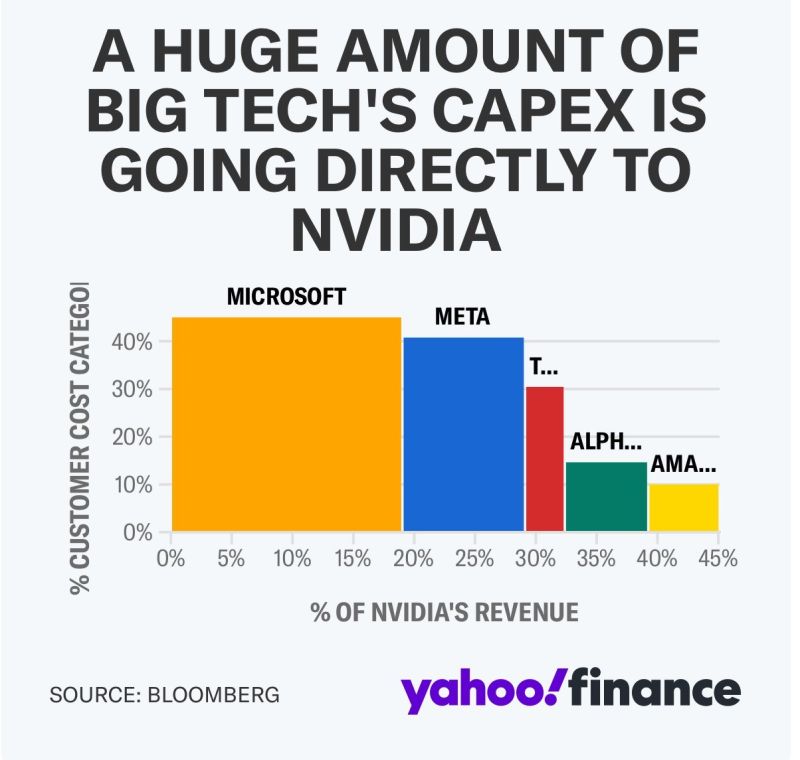

Nvidia: King of the AI Stack

Nvidia is no longer just a chipmaker, but is now the core of the AI economy. From its H100s and H200s to its newly announced Blackwell line, Nvidia dominates the data center GPU market virtually monopolistically. Its full-stack of software, from its CUDA to AI model orchestration, has given it a full-stack moat that is hard for its competitors to reproduce. In spite of geopolitical risk and growing export controls, the order book of Nvidia is strong, demand is unbeaten, and margins are historical.

Pricing compression and CapEx cycles going back to normal are concerning analysts, but for now, Nvidia still has the strongest quality revenue stream into AI infrastructure. It is the enabler of each of the broad AI projects, from model training to inference workloads.

Source: www.trendlinehq.com

Final Thought: Where Innovation and Market Power Meet

They're not only technology companies, but they're creating the future of AI, cloud, hardware, and consumer platforms. They each have a unique strategic piece: Nvidia builds the compute, Microsoft and Amazon sell the scale, Google and Meta use the software, and Apple and Tesla put it into everyday life. Not all equally will be rewarded, and even the most prepared investors can have their strategies derailed by macro headwinds or regulatory shocks. But what is true is that this generation not only leads the next industrial cycle. It is the industrial cycle. Investors would do well to grasp the distinction between trend and trendsetter.