- Nuclear is back, led by SMRs, uranium demand, and energy security focus.

- Renewables are scaling fast, with solar, wind, and storage dominating new investments.

- Oil & gas stay relevant, offering strong cash flow and transition-linked upside.

- Diversification wins, blending growth, yield, and resilience across the energy stack.

TradingKey - In the struggle to power the 21st century, the story of energy is no longer winner-takes-all, it’s a three-lane highway. It has on one side the nuclear energy shattering decades of Dormancy with new-generation technology and renewed political support. On the other hand, renewables are advancing at warp speed, moving from fringe utopianism to industrial stalwart. And in between, the aged oil and gas, long presumed in decline, are evolving into sleek, cash-flush players still crucial to global stability.

We are no longer facing an "either-or" scenario of fossils or green growth or yield, but rather a matured reality: the energy of the future is multi-dimensional, hybrid, and interconnected. For strategic thinkers, the greatest opportunities are neither at the corners, but in the crossroads. From uranium to hydrogen, solar farms to shale basins, the world of energy is expanding, and the smart money is learning how to straddle the three axes.

These three are the trifecta of energy. And now's the time to learn how to invest in them.

Nuclear Power: Stable, Scalable, Strategic

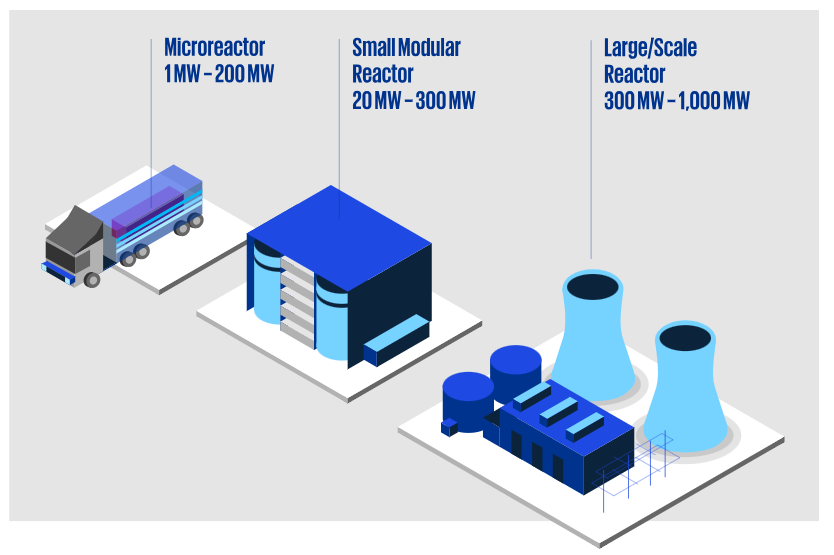

Nuclear is regaining the spotlight as an important pillar in the world energy transition. Historically excluded due to regulatory pains and social opprobrium, it’s now being appreciated for its unparalleled ability to offer rock-solid, zero-emissions baseload power. With demand for electricity surging, particularly from data centers, electrified transportation, and industrial decarbonization, nuclear power can offer a rock-solid base in an increasingly unpredictable grid mix.

Small Modular Reactors (SMRs) are taking the industry into a new era of flexibility and cost competitiveness. Aggressive investments by governments and companies in next-generation nuclear energy are in progress, and demand by investors is returning. Stocks such as Cameco (CCJ), the leading uranium producer, and Constellation Energy (CEG), the home of the largest US fleet of nuclear facilities, are gathering speed. Another key supplier of nuclear components, alongside defence-related systems that are nuclear-related, bucking the trend, is BWX Technologies (BWXT).

Source: drmcnatty.com

More speculative exposures to early-stage SMR development are also present in the likes of NuScale Power (SMR) and Centrus Energy (LEU). Now that global energy security has moved center stage, and carbon non-negotiability has become a fait accompli, the niche bet image of nuclear power is being abandoned in favor of center-stage position as a structural necessity.

Renewables: From High Potential to High Priority

The renewable sector has transformed from an environmental dream to the pillar of industrial strategy and economic planning. Solar, onshore wind, and battery storage are increasing at twice the growth of any other sector, with technology-driven decreases in costs and spirited policymaker support unlocking massive deployment pipelines.

Investors wanting to participate in this megatrend now have a list of increasing numbers of high-quality stocks to select. NextEra Energy (NEE) has the leadership position in renewable generation in the U.S. market, offering exposure to the wind, solar, and battery sectors with the utility balance sheet.

First Solar (FSLR) is still a growing, vertically integrated solar manufacturing entity with global scope. Enphase Energy (ENPH) has the microinverter solutions and energy management systems that are quickly becoming standard in the distributed solar market. Brookfield Renewable Partners (BEP) has a diversified hydro, wind, solar, and storage project profile across several continents.

.jpg)

In global scope, Ørsted and Iberdrola are market leaders in offshore wind and connected renewable infrastructure. With countries racing towards decarbonization goals, they will be the leaders of the next phase of the energy transition.

.jpg)

Source: ourworldindata.org

Oil & Gas: Cash Machines in a Transitional Economy

While the long-term shift to cleaner sources of energy is inevitable, oil and gas remains at the center of the world’s near-term energy needs. The industry has evolved, with a focus on capital discipline, returns for shareholders, and transition-compatible investments instead of aggressive growth.

These firms, such as Chevron (CVX) and ConocoPhillips (COP), have focused on this strategy by paying dividends to shareholders while making select investments in carbon sequestration, LNG, and lower-carbon fuels. EOG Resources (EOG) has differentiated by virtue of lean efficiencies coupled with strong free cash flows, largely in U.S. shale basins. Midstream players such as Enterprise Products Partners (EPD) and Energy Transfer (ET) also offer high-yielding opportunities with stable transportation and storage revenue flows.

These companies are no longer mere hydrocarbon extractors; they are, in ever greater numbers, transforming themselves into players in the energy transition, making investments in low-carbon technologies as well as in infrastructure that underpins global commerce and energy security.

A Converging World: Merging Strengths,Containing Risks

Most compelling about the current environment for investing in energy is that it’s no longer a zero-sum game. Nuclear, renewables, and fossil fuel technologies all are working alongside each other. SMRs and larger scale nuclear deployments provide stability to the grid by reducing renewable intermittency. Smart grids and battery storage are increasing the dispatchability of renewables. Natural gas still acts as a flexible backstop during periods of peak demand or shortages of supply.

It is generating investment opportunities through the entire energy stack. From the grid operators to the lithium miners, from hydrogen infrastructure to the natural gas liquefaction, the next phase of energy requires several inputs and solutions. Investors that develop balanced exposure through the system are better positioned to benefit from growth, as well as resiliency.

Strategic Allocation: Building a Diversified Energy Portfolio

In order to take advantage of this changing environment, diversified thinking may be appropriate. One potential modern day portfolio would be:

- Nuclear: Cameco (CCJ), Constellation Energy (CEG), BWX Technologies (BWXT), NuScale (SMR), Centrus Energy (LEU)

- Renewables: NextEra Energy (NEE), First Solar (FSLR), Enphase Energy (ENPH), Brookfield Renewable (BEP), Ørsted, Iberdrola

- Oil & Gas: Chevron (CVX), ConocoPhillips (COP), EOG Resources (EOG), Enterprise Products (EPD), Energy Transfer (ET)

It enables cross-sector exposure to long-term energy transformation with short-term dividend and cash-flow access. It also reduces the risk of regulatory risk, policy change, as well as macroeconomic volatility.

Conclusion

The world energy system is undergoing radical change, but it will not be built on a single pillar. Nuclear offers reliability and scale. Renewables offer exponential growth and social momentum. Oil and gas, in transition, still underpin global energy commerce and economic progress. It isn’t taking sides for investors, it’s taking the long view.

The center will continue to be occupied by energy in all its incarnations, and the toughest portfolios will be the ones that factor in the complexity, interconnectedness, and opportunity that define the new era. The trifecta of energy, the union of the new nuclear, the new renewables, the old hydrocarbons, isn’t a proposition anymore. It’s the blueprint of the decades ahead.