TradingKey - Gold prices surpassed the $4,000-per-ounce milestone for the first time in October 2025, marking another defining moment in the strong performance of safe-haven assets this year.

This rally is driven by far more than a simple surge in market risk aversion. While a weaker U.S. dollar and sustained gold purchases by central banks worldwide have provided support, the deeper catalyst lies in the fact that a growing number of large institutional investors including sovereign wealth funds, pension funds, and hedge funds are reevaluating gold’s strategic role in their portfolios.

Although gold itself generates no interest or dividends and has relatively limited industrial applications, its unique stability during turbulent times is attracting increasing attention.

Ray Dalio, founder of Bridgewater Associates, has noted that gold is an excellent tool for portfolio diversification.

Gold does not corrode, is highly durable, and carries no reliance on institutional credit backing. Unlike art, real estate, or other valuable assets, gold offers globally recognized liquidity, divisibility, and permanence. These qualities have enabled it to serve as a trusted store of value for thousands of years.

So, is gold worth including in your portfolio? How should you invest in gold, and how can you strike the right balance between gold and risk assets like the S&P 500? This article will break down these questions one by one, helping you make clearer, more rational asset allocation decisions in an age of uncertainty.

(Source: Shutterstock)

Why Is Gold Worth Including in Your Portfolio?

Gold prices have risen more than 50% so far this year, and analysts widely believe that, against the backdrop of a government shutdown, growing expectations for Federal Reserve rate cuts, and intensifying geopolitical risks, gold still has room to climb. Goldman Sachs even forecasts that by the end of 2026, gold could reach $4,900 per ounce.

But the rationale for holding gold goes far beyond betting on short-term price gains. Gold offers several compelling advantages:

- Protection Against Inflation

One of gold’s most valued traits among investors is its ability to preserve purchasing power over the long term.

Inflation silently erodes the value of cash, while gold has historically held its ground—or even gained ground—against it.

A telling example is housing. In 1929, the average price of a typical U.S. home was about $6,500. By 2024, that figure had risen to roughly $420,000, reflecting a dramatic decline in the dollar’s purchasing power.

But if we look through the lens of gold, the picture changes significantly. In 1929, 10 kilograms of gold was worth approximately $7,300—enough to buy a house. By 2024, the same 10 kilograms of gold was worth about $830,000.

This is not a suggestion to hoard physical gold, but rather an illustration of a deeper truth: over the long term, gold has significantly outperformed cash as a store of wealth.

- Portfolio Diversification

Can gold help make your investment portfolio more diversified?

The answer is yes—but only if allocated appropriately.

True diversification means spreading risk across different asset classes (such as stocks, bonds, real estate, and commodities), sectors, market capitalizations, and geographic regions.

Gold’s unique value lies in the fact that its price movements often do not move in lockstep with the stock market. During periods of equity market turmoil or heightened economic uncertainty, gold tends to hold steady or even rise in value.

Therefore, whether through physical gold, gold ETFs, or gold mining stocks, you can add a layer of “safe-haven cushion” to your portfolio without increasing systemic risk. However, if your entire portfolio is concentrated in gold, that is not diversification—it is a concentrated bet, which can actually amplify volatility and risk.

Which Is the Better Investment: Gold or the S&P 500?

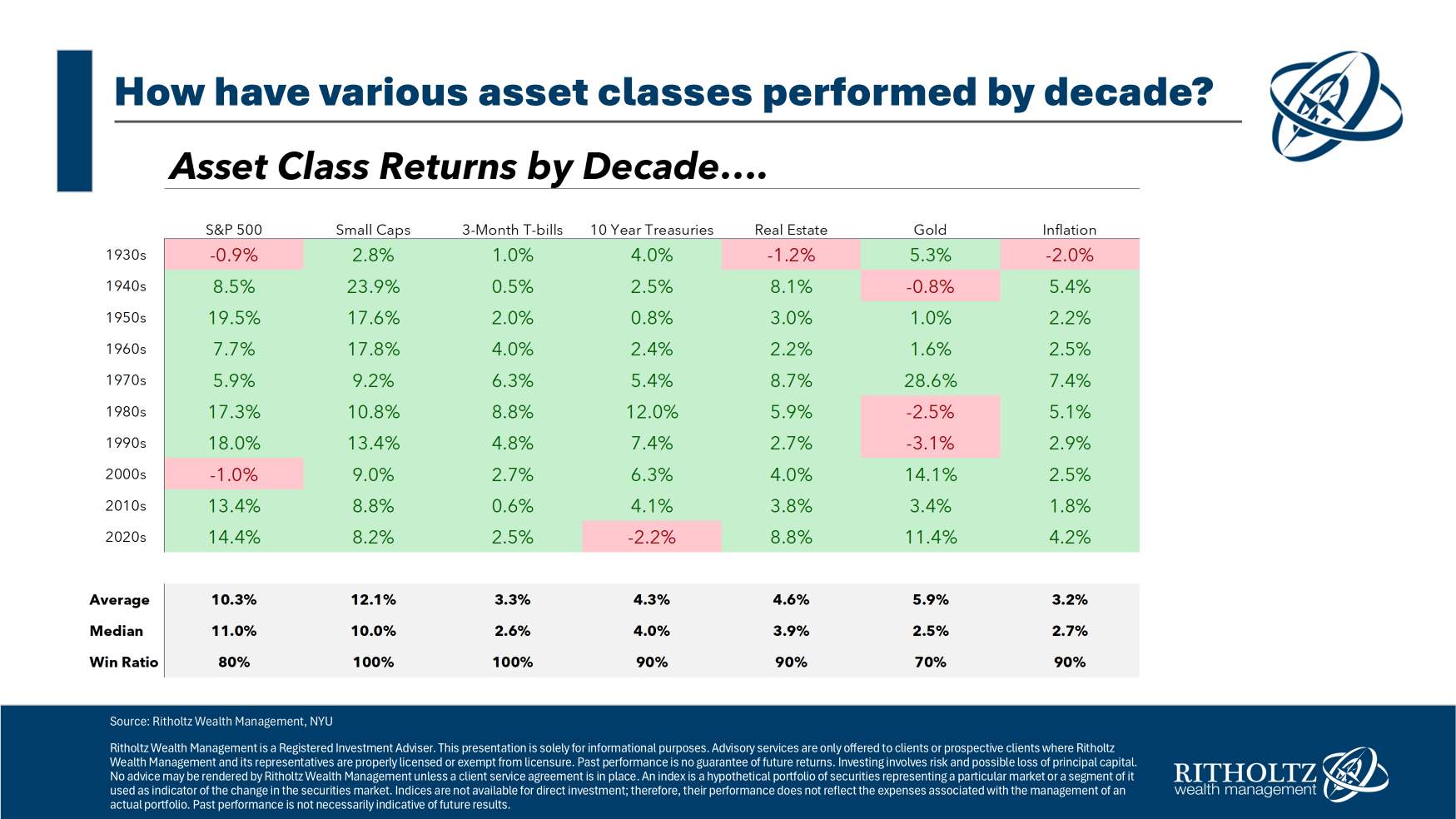

Over the past decade, gold prices have indeed risen significantly—from around $1,200 per ounce in 2015 to over $4,000 in 2025, a gain of more than 230%. This has led many investors to wonder: Is gold worth a heavy allocation? And compared to the S&P 500, which is the better choice?

The data shows that the S&P 500 has still outperformed over the past ten years. As of the end of 2024, its annualized return was approximately 14.4%, compared to 11.4% for gold. This edge stems largely from U.S. equities benefiting over the long term from corporate earnings growth, technological innovation, and a stable capital return mechanism, making the S&P 500 a powerful engine for compounded wealth creation.

However, this does not mean gold is “inferior.” Its value becomes clearest during the S&P 500’s most vulnerable moments—when inflation surges, geopolitical conflicts erupt, or markets experience severe turbulence. In those periods, gold often strengthens, providing critical downside protection for a portfolio.

2022 was a textbook example: the S&P 500 fell nearly 20% due to aggressive rate hikes, while gold outperformed the broader market, driven by safe-haven demand.

The key lies in understanding their fundamental differences. Gold offers stability, inflation hedging, and portfolio diversification benefits, making it an ideal choice for conservative investors or those navigating periods of high uncertainty. On the other hand, the S&P 500 delivers higher long-term returns through capital appreciation, but with greater volatility.

For this reason, heavily overweighting gold is generally not advisable.

Most experts recommend combining both assets to balance risk and return.

Mark Mirsberger, a certified public accountant and CEO of Dana Investment Advisors, noted: “We still see diversified balanced portfolios utilizing bonds and asset classes other than gold as more attractive and flexible than using material gold positions.”

How to Invest in Gold?

The most convenient and cost-effective approach for most investors is typically through exchange-traded funds (ETFs) that track the price of physical gold, rather than buying coins or bullion directly.

ETFs are widely regarded as highly liquid, low-cost, and easy to integrate into a diversified investment portfolio.

What Percentage of Your Portfolio Should Be Allocated to Gold?

Most financial advisors do not view gold as a core growth asset. Instead, they tend to position it as a hedge during turbulent times.

The reason is that gold’s value depends entirely on market sentiment, inflation expectations, and macroeconomic risks. This means that if gold prices stagnate over the long term, you are holding a “zero-yield asset.”

In addition, gold prices typically move inversely to the U.S. dollar. When the U.S. economy is strong and the dollar appreciates, gold often faces significant upward resistance.

(Source: Shutterstock)

Ray Dalio, founder of Bridgewater Associates, has long regarded gold as a critical hedge against currency devaluation and declining trust in institutions. He has emphasized that gold is the only asset investors can hold without relying on another party's promise to pay or generate interest, and recommends increasing gold allocations to 10%–15% during periods of heightened market stress.

How Risky Is It to Buy Gold at Record Highs?

With gold prices at all-time highs, many investors are paying close attention. However, chasing gains at peak prices in hopes of further short-term upside is a highly risky strategy.

You must recognize clearly that gold is a volatile, non-income-producing asset. It pays no dividends, generates no interest, and lacks earnings support. As a result, while gold prices can surge significantly over a few months, they can also drop sharply when policy shifts occur or the dollar strengthens.

When making decisions, be especially cautious of allocations driven by FOMO—fear of missing out. Unrealistic return expectations or attempts to “time the top” for quick profits often backfire.

Gold is better suited for long-term holding as a risk-mitigation tool and inflation hedge within a portfolio, not as a speculative instrument.

Moreover, gold is not regulated as rigorously as stocks or mutual funds under securities laws. This means that transactions involving physical gold, coins, or non-listed gold products often lack a unified, transparent oversight framework, making them vulnerable to fraud—such as selling counterfeit bars, overstating purity, or luring you to sell your gold jewelry at low prices only to resell it at a steep markup.

If you decide to allocate to gold, we recommend prioritizing regulated, highly liquid investment vehicles, such as major gold ETFs (e.g., GLD, IAU) or standardized products purchased through banks or large, reputable brokerages.

The Bottom Line

All investments involve risk and trade-offs.

Gold can effectively diversify a portfolio and hedge against inflation, but it also has clear limitations. It generates no cash flow, its price is driven by sentiment and macroeconomic expectations, and its movements are difficult to predict. Buying near historic highs further magnifies price risk. Additionally, the gold market lacks consistent regulatory oversight, making it prone to financial fraud—so choosing reputable and trustworthy trading channels is essential.

From an investment perspective, gold should always be viewed as a foundational asset class within your portfolio. Like any other asset, it should be evaluated holistically across four dimensions: expected return, volatility, correlation with other assets, and liquidity. On that basis, you can then make modest tactical adjustments according to the macro environment—such as monetary policy, geopolitical risks, and fiscal sustainability.

This perspective differs from mainstream thinking. Many treat gold as a short-term speculative tool, chasing price swings. While most people ask, “Will gold go up or down?” or “Should I buy or sell now?”, the more meaningful question is: What percentage of your long-term portfolio should be allocated to gold?

For most investors, a 5%–15% allocation to gold is a reasonable range, depending on your risk tolerance, overall asset mix, and assessment of systemic risks. For example, during periods of loose monetary discipline, high debt levels, escalating geopolitical tensions, or rising capital control risks, you might lean toward the 15% end of the range. In times of economic stability and strong market confidence, a 5% weighting may be more appropriate.

But remember: gold is not a productive asset. Over the long term, its returns typically lag behind income-generating assets like stocks. Yet its “insurance value” during crises remains irreplaceable.