TradingKey - On October 29, 2025, the Federal Reserve announced a 25-basis-point cut to the federal funds rate—the second such reduction this year. This move has left many homebuyers wondering: Will mortgage rates now drop significantly?

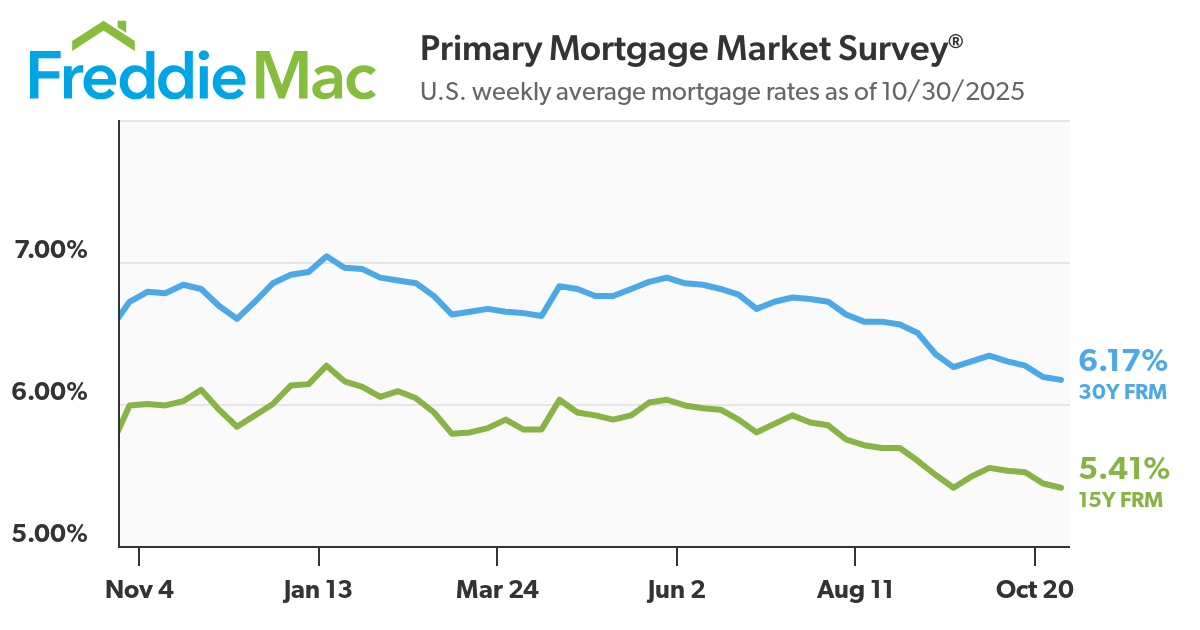

The good news is that mortgage rates are indeed trending downward. According to Freddie Mac data as of October 30, 2025, the average 30-year fixed mortgage rate has fallen to 6.17%, while the 15-year fixed rate has also declined to 5.41%—both at their lowest levels in nearly a year.

(Source: Freddie Mac)

However, for buyers who have been hoping that Fed rate cuts would sharply drive down mortgage rates, the reality is somewhat more complex. A Fed rate cut does not automatically translate into an immediate or substantial decline in mortgage rates.

That’s because the 30-year fixed mortgage rate is not directly tied to the federal funds rate. Instead, it is primarily driven by the yield on the 10-year U.S. Treasury note—which, in turn, is influenced by a range of factors including inflation expectations, fiscal deficits, employment data, and global capital flows. As a result, Treasury yields—and therefore mortgage rates—don’t always move in lockstep with the Fed’s policy decisions.

Did the Rate Cuts Actually Lower Your Mortgage Rate?

Looking back at 2024, markets had high hopes that the Federal Reserve would begin a rate-cutting cycle. Ahead of the September FOMC meeting, this expectation drove mortgage rates significantly lower between August and early September—the 30-year fixed rate briefly dipped to 6.08%, its lowest level in nearly two years.

But reality quickly offered a different answer. Despite the Fed’s 50-basis-point cut on September 18, 2024—which lowered the target federal funds rate to 4.75%–5.00%—mortgage rates did not continue their downward trend. Within just a few weeks, as markets reassessed persistent inflation and mounting federal budget deficits, the 10-year Treasury yield rebounded sharply, pulling mortgage rates back up.

Subsequent easing measures failed to reverse this pattern. In November 2024, the Fed cut rates again, yet the 30-year mortgage rate rose instead of falling, fluctuating between 6.8% and 6.9%. By December, even after another 25-basis-point reduction—bringing the federal funds rate down to 4.25%–4.50%—mortgage rates barely moved, ending the year still hovering around 6.8%.

This illustrates an important point: even when the Fed shifts to a more accommodative stance and short-term borrowing costs decline, long-term rates may remain elevated if inflation stays above target and Treasury yields keep rising.

(Source: Shutterstock)

In September 2025, the Fed cut rates once more by 25 basis points, lowering the federal funds rate to 4.00%–4.25%. This time, the mortgage market responded more positively—the 30-year fixed rate quickly dropped to 6.13%, its lowest level in nearly three years and notably below the 6.4% seen earlier that month.

Does this signal a turning point?

For now, conditions do appear more favorable. Although recent inflation data has shown slight upticks, it has declined significantly from the peaks of 2022–2023. Combined with the Fed’s signals of further rate cuts ahead, markets are now pricing in a more sustained easing cycle, creating room for mortgage rates to gradually drift toward the 6% range.

The Mortgage Bankers Association (MBA) projected in October 2025 that the 30-year fixed rate would average around 6.4% by the end of 2026, dipping slightly to 6.3% in 2027. Fannie Mae’s housing outlook is more optimistic, forecasting a decline to 5.9% by the end of 2026. While their forecasts differ, both agree that mortgage rates will remain above 6% throughout 2025.

For you, this suggests that the current period may represent a relatively favorable window over the past one to two years. If you’re considering buying a home or refinancing a high-rate mortgage, rather than waiting for the elusive “lowest point”—which is nearly impossible to time—focus instead on your personal financial situation and long-term goals, and proactively assess whether taking action now makes sense for you.

How Are Other Mortgage Products Affected?

Adjustable-rate mortgages (ARMs) and Home Equity Lines of Credit (HELOCs) are more directly tied to Federal Reserve policy—because their rates are typically linked to short-term benchmark rates, such as the Secured Overnight Financing Rate (SOFR) or the Prime Rate, both of which quickly reflect changes in the federal funds rate.

Adjustable-Rate Mortgages (ARMs)

If you hold an ARM, your interest rate usually resets annually or semi-annually after an initial fixed period (e.g., 5 or 7 years).

Once the Fed cuts rates, your next scheduled rate adjustment will likely decline accordingly. This means that during the current easing cycle, ARM borrowers may experience relief in borrowing costs sooner than those with fixed-rate mortgages.

However, if inflation rebounds in the future and the Fed resumes rate hikes, your monthly payment could rise sharply. Therefore, ARMs are best suited for borrowers who plan to sell or refinance within a short time frame.

Home Equity Lines of Credit (HELOCs)

HELOC rates are variable and typically adjust monthly, making them highly sensitive to Fed policy changes.

According to Bankrate’s latest data as of October 29, 2025, the average HELOC variable rate has fallen to 7.90%, a notable decline from its peak of around 10% in January 2024.

For you, this rate cut brings tangible benefits:

- If you already have a HELOC, your rate will automatically decrease—no need to apply for refinancing or pay fees.

- If you’re considering a new HELOC, this may be a relatively low-cost window, especially for large expenses like home renovations or debt consolidation.

What’s Happening in the Housing Market?

According to data from the Mortgage Bankers Association (MBA), for the week ending October 24, 2025, purchase mortgage applications rose 5% week-over-week, and total applications (including refinances) increased by 7.1%, indicating that some buyers are actively taking advantage of the current rate environment.

The core issue in today’s market remains a severe imbalance between supply and demand—particularly in the price range affordable to first-time homebuyers, where inventory is extremely scarce. When the number of buyers far exceeds available homes for sale, prices are unlikely to drop significantly—even with lower rates—because sellers know they hold a scarce asset.

Data from the Federal Reserve Bank of St. Louis shows that the median price of single-family homes has risen steadily since Q1 2009 (when it was $208,400), reaching $410,800 by Q2 2025—more than doubling over that period.

(Source: Shutterstock)

Should You Really Wait Until Rates Drop Below 6% to Buy a Home?

In short: Don’t wait for the “perfect rate.”

Mortgage rates certainly matter—they directly affect your monthly payment and total interest costs—but they’re not the whole story when it comes to the true cost of homeownership.

Home prices are equally critical, and they’re driven primarily by supply and demand. The market still faces a structural shortage, especially in the price range affordable to first-time buyers, where inventory remains extremely limited. When demand is strong and supply is tight, sellers often hold firm—or even raise prices—rather than lower them, even as rates decline.

The real opportunity to save money comes only when both rates and home prices fall simultaneously. While rates have recently eased, home prices in many cities continue to rise. Even with heightened recession risks, history shows that Fed rate cuts tend to stimulate housing demand, which—when combined with limited supply—can actually push prices higher, not lower.

As industry experts often say, don’t expect rate cuts alone to suddenly make the housing market “affordable.” Although current buying conditions have improved slightly compared to the peak, overall affordability remains far below pre-pandemic levels.

Before applying for a mortgage, we recommend obtaining quotes from at least several lenders and carefully comparing the Annual Percentage Rate (APR), fees, and repayment terms. At the same time, focus on your personal finances: improve your credit score, lower your debt-to-income ratio, and increase your down payment as much as possible—all of these steps can significantly improve the mortgage rate you qualify for.