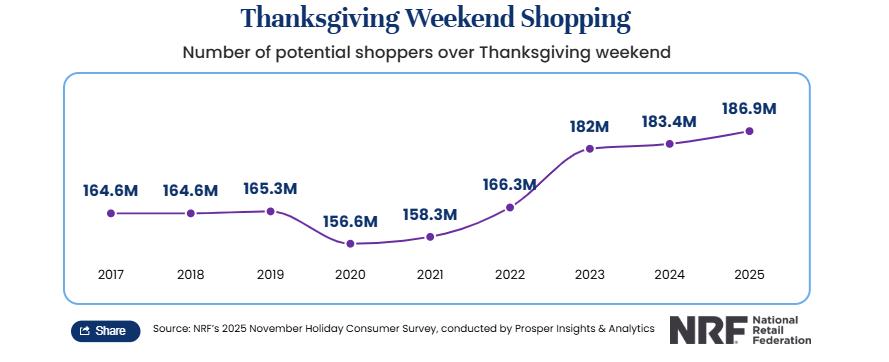

TradingKey - As you carefully prepare cranberry sauce and pumpkin pie for your Thanksgiving table, Black Friday looms right around the corner. According to the National Retail Federation (NRF), nearly 187 million Americans plan to shop during this year’s Thanksgiving weekend—a record-breaking number.

You’ve likely noticed that Black Friday has long transcended its "one-day" boundary, evolving into a weeks-long shopping marathon. Crowds lining up at store entrances, flashing countdown timers, and "Only 3 left!" warning labels—all are meticulously designed to trigger your sense of urgency.

Whether you’re enthusiastic about chasing every discount or typically avoid this shopping frenzy, the strategies that follow will reshape your understanding of "saving money." We’ll help you identify product categories that appear discounted but are actually traps, and share battle-tested price-tracking techniques.

While others are misled by marketing phrases like "Buy more, save more," you’ll grasp one crucial truth: the most expensive shopping bag is often the one filled with items you don’t need.

1. Create a Needs-Based Shopping List

As Black Friday’s promotional wave crashes in, your most effective defense is surprisingly simple: a shopping list written on paper. Research shows handwritten lists strengthen commitment more effectively than digital notes, helping you stay clear-headed amid the sales frenzy.

Studies reveal 16% of shoppers admit over half their Black Friday purchases are impulse buys. Clearly defining "who you’re buying for, what you need, and how much to spend" fundamentally prevents this trap. This isn’t an ordinary list—it’s your financial shield against marketing storms. If an item isn’t on it, no discount should sway your resolve.

The real shift happens in your mindset: from "Is this a good deal?" to "Is this a good deal for me?" When standing in crowded stores or scrolling through flashing web pages, this list helps you resist checkout counter upsell tactics.

Popular items often sell out quickly, potentially leading to panic purchases you’ll regret later. Savvy shoppers prepare not just primary plans but backup options. For instance, if your preferred gaming console is out of stock, have you identified functionally similar alternatives? This prevents disappointment-driven spending on unnecessary items.

Sales strategies exploit scarcity psychology with messages like "Buy now or lose forever." Your backup plan is the weapon against such tactics. Sometimes better discounts appear on near-sale dates or with brands you hadn’t considered. Stay flexible—use saved funds for other necessities rather than settling for unsuitable choices.

Before clicking purchase, review your wallet balance: confirm fixed expenses (rent, utilities), then set an unbreakable total budget.

Black Friday spending shouldn’t come at the cost of depleting emergency funds or compromising essential bills. Before the sale season begins, ensure necessary payments are covered and funds earmarked for debt repayment or long-term savings remain untouched.

2. Don’t Shop on Credit You Don’t Have

Never shop with money you don’t possess.

Have you calculated this: when credit cards charge 22%–24% interest, is a 20% or 30% discount truly worthwhile? Many are still paying off last Christmas’ debt, trapped in a cycle of "postponing payment for one month, then another."

Holiday spending should come from only two sources: a dedicated holiday savings fund or genuine surplus after covering all necessities (bills, rent, emergency savings).

Black Friday’s biggest misconception equates discount percentages with actual savings. When using high-interest debt to buy unplanned items, surface-level discounts vanish under interest charges.

First, determine your debt-free budget limit, then hunt for optimal discounts within that range—not the reverse of being lured by sales then scrambling to finance them.

Remember: a $100 item debt-free is always cheaper than a $70 item carrying 24% interest. At checkout, ask yourself: "If I had to pay cash, would I still buy this?"

(Source: Freepik)

3. Avoid Impulse Purchases

When drawn to a promotional item, try this simple yet powerful strategy: add it to your cart, then force yourself to wait exactly 24 hours before deciding whether to buy it. This "cooling-off period" helps overcome 90% of impulse buying urges. After 24 hours, you’ll be surprised to find you no longer need nearly half the items in your cart.

These 24 hours aren’t mere procrastination—they’re a critical window for emotional highs from shopping to naturally subside. When flashing "limited-time offer" and "low stock" alerts no longer dominate your decisions, you can return to rational thinking: Does this item truly align with your needs and values? Is it on your pre-made shopping list? If not, no matter how tempting the discount, it isn’t worth dipping into hard-earned savings.

By embedding the 24-hour rule into your shopping habits, you not only avoid costly regrets but also cultivate spending wisdom aligned with long-term financial goals. True savings aren’t about the size of a single discount—they’re about every purchase standing the test of time.

4. Beware of Marketing Traps

The next time you see an advertisement boasting "huge savings," remember this is a carefully engineered marketing tactic. Black Friday’s core purpose is to get you to spend more.

The phrase "buy more, save more" completely inverts financial logic—in reality, larger purchase volumes mean higher total spending. Retailers often create urgency with tactics like "offer ends in two hours" to trigger your fear of missing out (FOMO).

You may not realize many enticing "50% off" deals are meticulously crafted. Retailers sometimes quietly raise "original prices" before promotions to make discounts appear deeper, or artificially manufacture scarcity to pressure rushed decisions.

Financial advisors state bluntly: "These sales events aren’t designed for your benefit."

5. Use Cashback Apps and Browser Extensions

Cashback platforms and rewards programs can genuinely enhance your budget—but only when used wisely. When reward mechanisms tempt you to buy unplanned items or increase spending to accumulate more points, they transform from useful tools into financial traps. Your budget plan should drive spending decisions, not point incentives.

Mastering cashback apps and browser plugins is essential for online shopping. Even small cashback percentages compound significantly over time, delivering substantial quarterly returns.

For example, use CamelCamelCamel to review 120-day price histories. Compare prices across retailers with PriceBlink or Google Shopping. Consolidate coupons through aggregators like CouponCabin.

Shopping portals aren’t ordinary links. Take Capital One Shopping: even non-cardholders benefit from its automatic testing of 200+ promo codes, commonly earning 35% cashback at partner retailers like Nike. Even better is its "threshold cashback" feature: spend $50 at Walmart and get $50 back immediately—effectively receiving free merchandise. The technique is simple: install the browser extension beforehand or access merchant sites exclusively through the dedicated app.

6. Check Credit Card Offers

Spend 30 seconds verifying whether your credit card offers exclusive benefits for this retailer. Many cardholders don't realize banks frequently partner with specific merchants to provide limited-time discounts, accelerated rewards points, or statement credits—but these perks typically require pre-activation through online banking or mobile apps. Skip this step, and even credit card transactions won't trigger the benefits.

7. Approach "Buy Now, Pay Later" Services Cautiously

"Buy now, pay later" (BNPL) services like Klarna or Afterpay let you split large purchases into 4–6 weeks of small, interest-free installments—especially convenient for big-ticket items like sofas or TVs. Before using them, ensure you’ve budgeted specifically for the item to guarantee the timely completion of all installments.

They also enable you to simultaneously earn cashback and rewards points for future shopping. PayPal Pay in 4, for instance, offers 20% cashback (up to $250 per transaction) when eligible, with returns redeemable as actual cash. If you can guarantee full repayment on schedule and the service charges no interest, this combination may deliver real value.

However, BNPL’s fragmented debt structure makes total liabilities easy to lose control of. Unlike a single credit card statement, these micro-installments scatter across multiple merchant platforms, where they’re easily forgotten.

Missed payments not only incur extra fees but can also erase initial discounts through accumulated interest. Experts recommend using BNPL only when purchases fully align with your budget and you can 100% guarantee on-time repayment—otherwise, this seemingly convenient payment method may become a months-long financial burden after the holidays.

Learn more: Is "Interest-Free" Truly Free? How "Buy Now, Pay Later" (BNPL) "Painless Spending" Fuels Mounting Debt

(Source: Freepik)

8. Avoid Scam Traps

As you immerse yourself in Black Friday’s promotional frenzy, scammers lie in wait. To protect your personal information and funds, cultivate these critical habits: shop only on well-known retailers’ official websites, and always verify the URL begins with "https://" and displays a padlock icon before checkout.

No legitimate merchant will ever request sensitive details like your Social Security number via email or text—a key red flag for phishing attempts.

Phishers often exploit holiday shopping anxiety through spoofed coupons, fake order confirmations, or "account anomaly" alerts to steal payment information. Stay vigilant when encountering deals that seem "too good to be true." Prices significantly below market averages are often danger signals.

Pay special attention to urgent notices claiming "delivery failure" or "package stuck in transit"—these frequently disguise malicious links as logistics updates.

The correct approach: ignore suspicious messages and check order status directly through official apps or customer service channels. Before entering any payment details, spend ten seconds verifying the site’s authenticity—this brief pause may save you thousands of dollars in losses.

Conclusion

Before clicking "Buy," honestly ask yourself: Will this item add meaning to my life, or merely clutter my storage? Am I choosing it because I genuinely need it, or simply because I’m dazzled by the discount sticker?

You have the power to redefine the holidays’ meaning—the warmest memories never come from gifts piled under the tree, but from moments shared with loved ones. When financial discipline becomes your compass, you’ll enter the new year proud of your wise choices—not shadowed by debt.

Black Friday is indeed an opportunity for real savings, but the true winners are those who enter this shopping storm with clear plans and firm boundaries. After shopping, spend a few minutes recording each item’s return policy and safely storing digital or paper receipts. These small habits will save immense hassle during returns or warranty claims.

When you uphold predetermined limits, spending won’t become compromise. You’ll enjoy the joy of finding genuine bargains while avoiding post-holiday bill anxiety.