TradingKey - On Thursday, U.S. President Donald Trump announced a large-scale financial market intervention plan, directing Fannie Mae and Freddie Mac to purchase mortgage-backed securities (MBS) totaling $200 billion.

Widely viewed as "Trump-style quantitative easing (QE)," the move aims to lower mortgage rates, reduce borrowers’ cost burdens, and revitalize the housing market.

"This will further reduce mortgage rates, decrease monthly payments, and make homeownership more economically feasible," Trump stated on the social platform Truth Social. He emphasized that the initiative is feasible because the two government-sponsored housing entities currently hold ample cash reserves.

Federal Housing Finance Agency (FHFA) Director Bill Pulte responded later that evening via X: "We are implementing this directive. Thank you, President Trump—Fannie Mae and Freddie Mac will commence executing the relevant plan."

Trump also criticized former President Biden’s housing policy management, asserting his administration had "failed in numerous aspects," including neglecting the housing market. "I have fixed the mess he left behind!" he wrote.

Reflecting on his first term, Trump noted his decision to pause the sale of Fannie Mae and Freddie Mac—strategic assets he described as now yielding considerable returns. "Though some ‘experts’ advised selling them at the time, this proved a farsighted policy choice. Today, they have grown into vital financial pillars with doubled market value and $200 billion in cash reserves. I am now authorizing representatives to deploy these funds to purchase an equivalent amount of mortgage bonds," he said.

Additionally, on Wednesday, Trump proposed restricting financial institutions from investing in single-family homes to address housing affordability for ordinary families. According to informed sources, alongside these policy actions, the White House is drafting a new executive order focused on alleviating Americans’ cost-of-living pressures. This includes exploring measures such as permitting the use of retirement accounts or college tuition savings accounts as sources for home down payments.

Right now, global investors and ordinary families preparing to buy homes are closely watching whether this policy will genuinely lower mortgage rates as intended? And what impacts will it have on ordinary people’s housing finance decisions?

(Source: Freepik)

Why Is Trump Intervening in the MBS Market?

In recent years, "affordability" has become a cornerstone of Democratic political narratives, with persistent criticism directed at the Republican president for failing to address rising living costs and persistently high prices.

As expenses for food, transportation, and housing continue climbing, Americans’ perception that "life is getting more expensive" intensifies—making "affordability" a pivotal election issue. Though Trump has occasionally downplayed this problem, attributing today’s inflation to the Biden administration, voter dissatisfaction over economic pressures has already begun eroding his support.

Trump’s bold bond-buying initiative—executed by Fannie Mae and Freddie Mac ("the two government-sponsored entities")—echoes the Federal Reserve’s pandemic-era quantitative easing. Back then, massive purchases of bonds including MBS lowered borrowing costs and stimulated economic recovery.

Unlike the Fed’s money-printing approach, this time the funds come from existing liquidity on the entities’ own balance sheets.

FHFA Director Bill Pulte specifically noted that neither the Federal Reserve nor the Treasury Department will participate. This means capital is drawn from current reserves—not newly printed currency—thus avoiding market fears of exacerbated inflation.

As part of this housing policy package, Trump recently announced plans to restrict financial institutions from acquiring properties—particularly banning purchases of single-family homes—to curb large investors from driving up prices and crowding out ordinary families.

How Does Buying MBS Affect Mortgage Rates?

To understand the significance of Trump directing Fannie Mae and Freddie Mac to purchase $200 billion in MBS for ordinary homebuyers, we must first clarify two concepts: What is MBS? And how is it linked to mortgage rates?

What Is MBS?

Think of MBS as bonds created from "bundles of mortgages."

Specifically, whento help banks acquire these loan bundles or issue/purchase MBS, thereby accelerating capital circulation and expanding access to homeownership banks lend money to many homebuyers (issuing residential mortgages), they don’t wait decades for repayments. Instead, they package these loans into a financial product—the MBS—which they sell to investors. This allows banks to recoup cash immediately and issue new loans.

Fannie Mae and Freddie Mac, U.S. government-sponsored entities, serve as the "backbone" of America’s housing finance system.

Their primary role is to help banks acquire these loan bundles or issue/purchase MBS, thereby accelerating capital circulation and expanding access to homeownership.

How MBS Purchases Impact Your Loan Rate

Trump’s directive for Fannie Mae and Freddie Mac to buy $200 billion in MBS uses market mechanisms to push mortgage rates downward through a clear cause-effect chain:

- Increased Demand Raises Prices

When the two entities massively buy MBS, demand for these securities surges. Just as frenzied demand drives up prices for any commodity, MBS prices rise accordingly.

- Price Increases Lower Yields

Bond markets follow a fundamental rule: when prices rise, yields fall. Investors paying more for the same bond receive lower returns.

- Banks Price New Loans Based on These Yields

When setting rates for new mortgages, banks reference MBS yields.

If MBS yields drop, banks cannot profitably issue new high-rate mortgages—nobody would buy the resulting MBS packages. To ensure liquidity and continued sales, banks must lower mortgage rates.

In simple terms, by buying massive amounts of MBS, the entities suppress the returns investors accept. This forces banks to reduce rates on new mortgages—ultimately letting ordinary borrowers secure lower monthly payments.

This isn’t America’s first such maneuver. The most notable example came in early 2020 when the Fed’s massive MBS purchases drove 30-year fixed mortgage rates below 3%—a historic low.

Can It Truly Reduce Mortgage Pressure?

During past economic crises, the Federal Reserve repeatedly purchased mortgage-backed securities (MBS) to suppress mortgage rates. Then, many families secured refinancing at rates of 3% or lower.

However, the market remains skeptical about the effectiveness of the $200 billion MBS purchase plan led by Trump’s directive to Fannie Mae and Freddie Mac ("the two government-sponsored entities").

Housing economists widely believe these measures will have minimal impact on America’s nationwide affordability crisis, with highly uncertain market effects.

Richard Green, Director of the USC Lusk Center for Real Estate, emphasized that the U.S. housing pain point has always been "a persistent shortage of supply." Merely encouraging lower borrowing costs or restricting buyer types cannot resolve root causes. "The $200 billion sounds substantial, but at the national scale, its actual impact is limited," he noted.

He specifically warned that if purchases further inflate home prices, borrowers benefiting from lower monthly payments would soon face higher down payment barriers. "Simply put, lowering mortgage rates sounds appealing—but if it doubles the cash you need upfront, it’s hardly a relief."

"From a macro perspective, this is merely a short-term emergency measure unlikely to decisively address today’s complex housing challenges," stated Daryl Fairweather, Chief Economist at real estate services firm Redfin.

She estimated the plan might reduce 30-year fixed mortgage rates by 0.25–0.5 percentage points but stressed this falls far short of solving deep-seated issues.

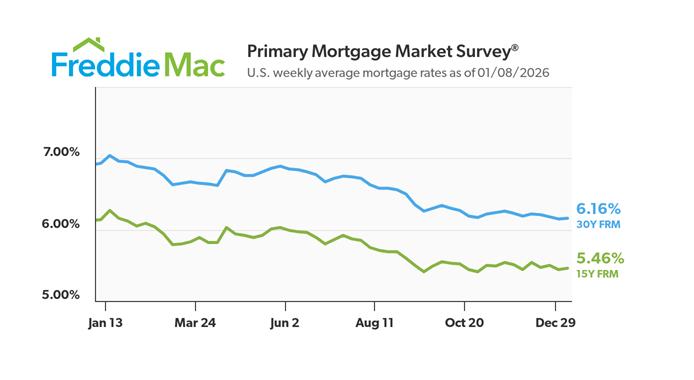

According to recent Freddie Mac data, the current average rate for 30-year fixed mortgages stands at approximately 6.16%. Since September 2022, this figure has never dipped below 6%. Prior to this—during the pandemic’s ultra-loose policy phase—many borrowers locked in rates at 3% or lower.

(Source: Freddie Mac)

Though rates have slightly retreated from last year’s peak near 7%, persistently high prices for housing, food, and energy continue to overwhelm households. Interest costs have decreased marginally, yet real affordability pressures remain acute.

St. Louis Fed data reveals that as of mid-last year, total outstanding U.S. residential mortgage debt reached approximately $21.1 trillion. Behind this colossal figure lies widespread anxiety among families seeking stable homeownership without drowning in unaffordable payments.

Simultaneously, voices caution about risks inherent in such large-scale capital intervention. Trump’s plan taps into the cash reserves on the two entities’ balance sheets—funds originally designated as emergency buffers for crises like market rescues or self-protection during systemic shocks.

"Using the firewall’s funds for market rescue is, in some ways, gambling that the housing market won’t collapse," commented a retired financial official.

Moreover, the Federal Reserve still holds roughly $2 trillion in MBS assets and is gradually "shrinking its balance sheet," having reduced holdings by $700 billion since their peak in June 2022.

Against a backdrop of plateauing global inflation and tightening monetary policy, the operational room to significantly suppress long-term borrowing costs is inherently constrained. Under these conditions, modest bond purchases are unlikely to reverse the trend—a reality that warrants tempered expectations.

(Source: Freepik)

How Should We Respond?

- For Homebuyers

If you plan to buy a home within the next 3–6 months, consider waiting one to two months to observe whether the policy genuinely drives down mortgage rates—but keep two points in mind.

First, there are diminishing returns to waiting. Avoid obsessing over timing the absolute bottom. For instance, if rates drop only ~0.3 percentage points after monitoring, it’s likely sufficient to act decisively. Home price appreciation could quickly erase this marginal benefit.

Second, prepare in advance. Secure your down payment, organize credit reports, and research reputable lenders. When bond markets shift, or opportunities arise, you’ll be ready to apply immediately—avoiding missed chances.

If your purchase is urgent (e.g., closing required within a month), hesitation is unnecessary. Instead, scrutinize personalized offers from banks or lenders. During competitive periods, some institutions grant extra discounts to borrowers with high down payments and strong credit—a direct, cost-saving advantage often surpassing nationwide rate cuts driven by policy.

- For Existing Mortgage Holders

If you already have a mortgage at a fixed rate above 6.5% with a long remaining term (e.g., 15+ years), begin tracking refinancing opportunities emerging from market discussions.

Generally, refinancing makes sense if the new rate is at least 0.5 percentage points lower than your current rate and you plan to keep the home long-term—but factor in process costs like fees and appraisal expenses.

A reasonable calculation shows savings typically offset these costs within 6–12 months, after which true savings begin.

Discuss procedures and cost breakdowns early with your lender while estimating potential interest savings. If policy impacts are minimal (e.g., only ~0.2% rate adjustment), the hassle involved may not justify the costs—delay action in such cases.

- For General Investors

Investors in MBS funds or real estate finance stocks may see short-term price gains from this policy, but should cautiously weigh two latent risks.

First, actual policy effects may underperform expectations. If the $200 billion bond-buying plan fails to significantly reduce mortgage rates, related assets could surge initially before correcting sharply.

Second, housing policy direction remains unclear. Trump’s recent proposals—like restricting large institutions from buying single-family homes—could disrupt real estate supply-demand dynamics if strictly enforced, triggering market volatility.

Thus, rational judgment is essential when approaching these investment vehicles.