TradingKey - When you see the "four interest-free installments" option at checkout, you might not realize this simple checkbox represents a financial revolution reshaping consumer habits.

The "Buy Now, Pay Later" (BNPL) model emerged in the early 21st century through services like PayPal Credit, later popularized by companies such as Klarna, Affirm, and Afterpay. This innovative payment method offers short-term, interest-free installment plans, redefining convenience in e-commerce and retail.

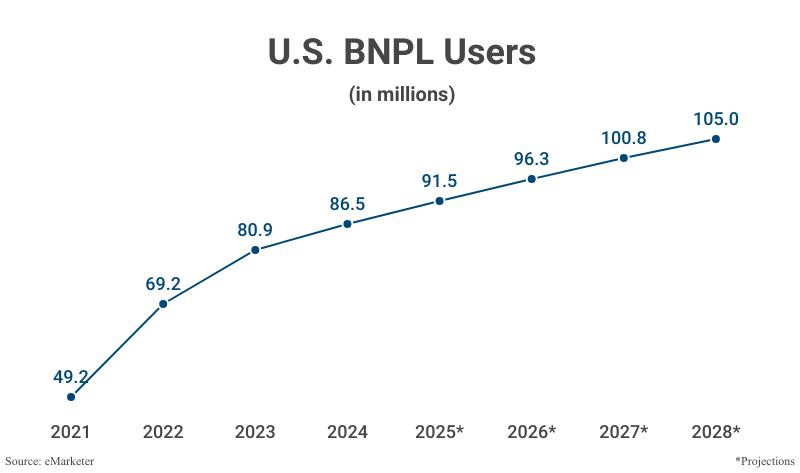

Today, BNPL has permeated mainstream U.S. consumption. Survey data reveals over one-quarter of American consumers have used BNPL’s short-term installment loans for purchases.

Yet convenience often conceals costs. A Bankrate survey found nearly half (49%) of BNPL users encountered financial difficulties after using the service. Breaking total costs into small installments dilutes awareness of overall spending, and when users juggle multiple active orders, actual debt levels can easily exceed expectations.

Unplanned overspending, missed payments, post-impulse-purchase regret, and complex return processes follow. When the promise of "pay tomorrow" becomes too effortless, are we compromising today’s financial health? As BNPL evolves from a niche payment method to a mainstream consumption tool, this question warrants deep reflection from every consumer.

What Is "Buy Now, Pay Later" (BNPL)?

"Buy Now, Pay Later" (BNPL) is an innovative consumer credit model that enables immediate receipt of goods or services while splitting payments into fixed, small installments.

For example, a $100 purchase can be divided into four payments of $25 each—typically without interest. By lowering the barrier of single-payment costs, this model significantly boosts purchasing willingness and capacity.

Today, platforms like Affirm, Afterpay, Klarna, and Zip have deeply integrated BNPL services into global e-commerce ecosystems. Data shows merchants offering BNPL options can increase revenue by up to 14%.

For consumers, BNPL is generally interest-free; providers profit by charging merchants transaction fees (typically 3–6% of the purchase amount) and imposing late fees on overdue payments.

BNPL’s rise is inextricably linked to e-commerce expansion. Between 2019 and 2021, the pandemic accelerated digital payment transformation, spiking demand for flexible, transparent payment methods. Today, BNPL has expanded beyond retail into travel, healthcare services, and daily essentials. Chargeflow projects the global BNPL market will reach $560.1 billion by 2025.

(Source: Shutterstock)

Why Do Consumers Prefer "Buy Now, Pay Later"?

BNPL’s rapid adoption stems from its ability to bypass traditional credit barriers. Unlike credit cards—which demand strict credit scores and income verification—BNPL requires only minimal credit checks, with approvals often granted in seconds. It functions as a streamlined alternative to credit cards: no complex procedures, yet immediate access to desired goods.

For consumers, it perfectly solves the "want to buy but temporarily short on cash" dilemma. Without cumbersome credit approvals, users simply link a bank card to split purchases into 3–6 (or longer) installments—most short-term plans even offer interest-free periods.

This model particularly appeals to three groups: financially vulnerable households, consumers sensitive to high credit card rates, and young adults with limited credit history.

Mainstream BNPL services provide zero-interest policies for timely repayments, drastically reducing financing costs. They also feature lenient default mechanisms—average late fees are only $7 (based on a typical $135 loan amount). Crucially, occasional late payments typically do not impact personal credit scores. This risk mitigation creates financial breathing room for economically unstable groups, enabling essential daily purchases through BNPL.

How Does "Buy Now, Pay Later" Differ from Traditional Credit Cards?

Cost Structure

BNPL’s core appeal lies in short-term interest-free periods—major platforms offer zero-interest plans for timely repayments, though late payments incur fixed late fees (typically $7–$10).

Credit cards operate on a fundamentally different pricing model, charging 15%–25% annual percentage rates (APR) on unpaid balances. This compounding interest structure can trigger debt snowball effects, trapping consumers in long-term repayment cycles.

Access Thresholds

BNPL approval typically requires only basic identity verification, with 90% of applications approved within seconds—opening doors for those with thin credit histories.

Traditional credit cards rely on the FICO scoring system, demanding comprehensive income documentation and established credit history. This excludes approximately 45 million "credit invisibles."

This gap positions BNPL as a driver of financial inclusion but raises concerns about over-extended credit access.

Repayment Mechanisms

BNPL enforces rigid installment structures—a $1,000 purchase must be split into four fixed $250 payments, with terms rarely exceeding six months.

Credit cards offer flexible frameworks: a $1,000 bill might require only a $150 minimum payment, rolling the remainder to the next month—but accruing interest on the balance.

Consumer Psychology

BNPL reshapes purchasing decisions through "small, painless" framing—transforming a $750 laptop into "four payments of $187.50" to drastically reduce payment pain and stimulate immediate spending.

Credit cards cultivate habitual borrowing through revolving credit limits, where consumers easily fall into the "minimum payment trap."

(Source: Freepik)

Are You Sliding Into a "Buy Now, Pay Later" Debt Trap Without Realizing It?

When consumers use "Buy Now, Pay Later" to pay for grocery bills, this behavior has shifted from a spending habit to an economic warning signal.

Data reveals that in 2024, 15% of U.S. adults used BNPL—up from 14% in 2023. More alarmingly, approximately 34% to 41% of BNPL users reported missing payments in the past year. Gen Z users face even higher delinquency rates at 51%, sparking serious concerns about consumer debt and defaults.

When a $1,200 smartphone becomes "4 interest-free installments of $300 each," or a $1,500 laptop splits into "6 payments of $250," the payment pain from the total price is dramatically diluted.

More dangerously, multiple platform installments compound: you might finance electronics on Platform A, clothing on Platform B, and home goods on Platform C. Each monthly payment seems reasonable individually, but their total may exceed 30% of your monthly income—breaching the debt safety threshold.

"Interest-free" terms often carry harsh conditions. Some platforms require "all installments to be paid on time" to qualify for zero interest, otherwise retroactively charge interest. Others waive interest only on the first installment while imposing high fees on subsequent payments.

Hidden costs like account maintenance fees and prepayment penalties often lurk beneath the surface. While some BNPL services aren’t yet integrated with credit bureaus, delinquency records are shared among platforms, restricting your access to other services. For credit-linked BNPL options, missed payments directly damage your credit score, jeopardizing future mortgage or auto loan applications.

Young professionals just entering the workforce are especially vulnerable—the tension between stable income and strong consumption desires, combined with BNPL’s low barriers, pulls them into debt quagmires before they develop financial planning skills. Often, they only recognize the severity of their situation when debt spirals beyond control.

How to Avoid Falling Into the "Buy Now, Pay Later" Debt Trap?

- Define Clear Usage Boundaries

Use BNPL only for essential purchases—such as replacing a malfunctioning core appliance or buying occupation-critical equipment—rather than for discretionary entertainment or luxury items.

Before each use, record the full amount in expense tracking software instead of focusing solely on monthly payments. Research shows that when consumers make decisions based on total price rather than installment amounts, unnecessary spending decreases by 35%.

- Read Loan Terms Carefully

Before confirming a purchase, spend two minutes verifying these key details: the actual interest-free period (some platforms waive interest only on the first installment), late payment fee rates (typically 0.05%–0.1% per day), and whether delinquencies affect credit records.

Be cautious of vaguely worded terms. Prioritize BNPL services operated by banks or licensed financial institutions—these products face strict regulatory oversight and have lower rates of hidden fees.

- Practice Sound Debt Management

Meticulously track each BNPL installment’s amount, repayment date, and monthly payment in a dedicated ledger to ensure timely repayment. Simultaneously maintain an emergency fund to prevent debt delinquency during unexpected events.

Conclusion

The "Buy Now, Pay Later" wave is reshaping America’s consumption landscape. It represents not merely a payment innovation but a fundamental shift in consumer culture and debt structures. As millions of households ease immediate pressures through installment payments, this model is quietly transforming community commerce, regional consumption data, and even national debt composition.

We must acknowledge BNPL’s genuine value: it opens doors for those with thin credit histories, provides buffers for urgent needs, and creates financial flexibility for young families.