TradingKey - President Donald Trump recently posted on Truth Social, suggesting his administration is advancing a 50-year mortgage plan. Soon after, Federal Housing Finance Agency Director Bill Pulte posted on X: “Thanks to President Trump, we are indeed working on The 50 year Mortgage—a complete game changer.”

This announcement has sparked immediate widespread attention. For you as a potential homebuyer, it superficially offers a new path to address housing affordability challenges. Compared to traditional 30-year loans, the 50-year option may make loan approval easier for you and significantly reduce monthly payments—a compelling proposition amid historically high home prices and interest rates.

Housing, as a basic necessity, holds irreplaceable significance for you and your family. For you, housing security is not merely about financial stability but serves as the cornerstone for family formation and development—no one wants to face forced relocation during their children’s upbringing due to a landlord’s decision to sell or raise rents.

However, multiple mortgage experts urge caution. While monthly payments decrease, extending the repayment period by 20 years substantially increases the total interest you pay over the loan’s lifetime and drastically slows the accumulation of home equity. This means it will take you much longer to truly own your property outright, rather than continuously transferring wealth to lenders.

When you evaluate whether to choose a 50-year mortgage, consider how to comprehensively weigh short-term financial relief against long-term economic health. After all, a home purchase decision concerns not only securing shelter today but also impacts your financial freedom and family stability for decades to come.

What Is a 50-Year Mortgage?

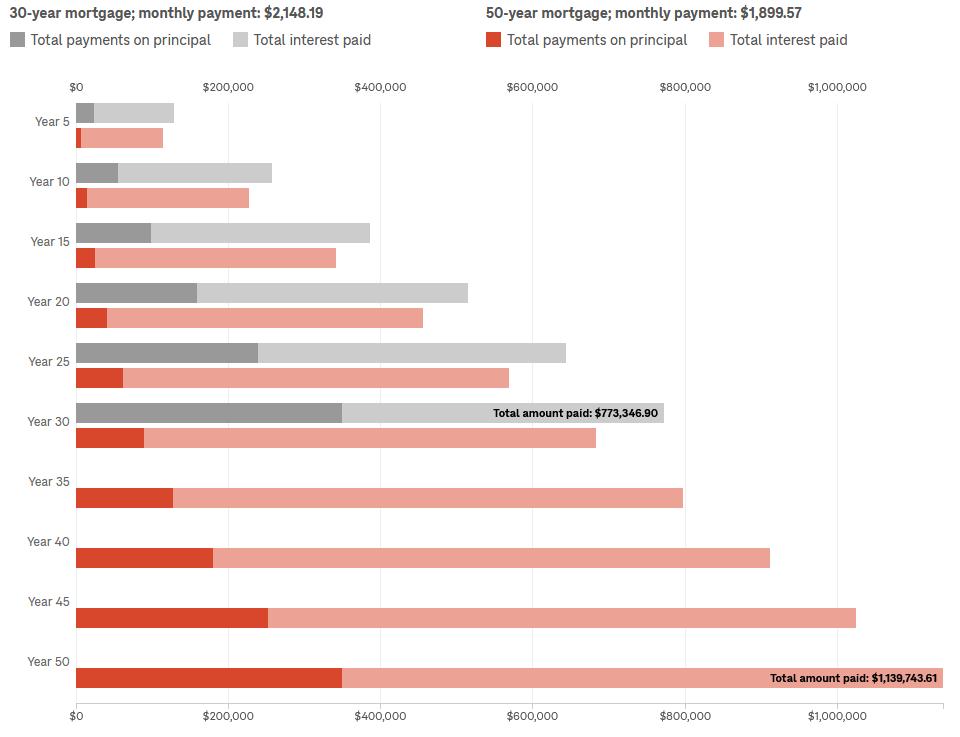

The 30-year mortgage has existed for over 90 years. As the most mainstream home financing option, it has helped millions of Americans achieve homeownership through lower monthly payments and fixed interest rates. A 50-year mortgage, as its name implies, extends the repayment term by a full 20 years—from 360 months to 600 months.

The extended term reduces monthly payments but significantly slows the pace at which the loan balance is paid down.

What Are the Advantages of a 50-Year Mortgage?

The most significant advantage of a 50-year mortgage lies in its ability to effectively reduce your monthly repayment burden. Compared to traditional 30-year options, the extended repayment period allows you to spread the loan amount over a longer timeframe, thereby easing monthly financial pressure.

Specifically, if you apply for a $350,000 home loan with a 6.22% annual interest rate, choosing a 50-year repayment plan could save you approximately $250 per month. For many families, this additional cash flow can translate into tangible improvements in quality of life—whether used for daily expenses or children's education.

Financial experts note that this repayment structure is particularly suitable for first-time homebuyers in today's high-price housing environment. When facing property prices of $400,000 to $500,000, the $200–$300 monthly savings may mean qualifying for a loan or even considering homes with better conditions.

An industry observer stated: "For budget-constrained families, this flexibility is not merely a numerical change but a key to unlocking homeownership."

More importantly, by distributing repayment pressure, the 50-year mortgage provides greater financial flexibility. During early career stages when income may fluctuate, lower monthly payments allow you to plan your life more comfortably while building home equity.

What Hidden Costs Will a 50-Year Mortgage Impose on You?

When considering a 50-year mortgage, the most critical factor to watch is its long-term financial impact. While monthly payments are lower, you must face this reality: If you purchase a home at age 30, a 30-year loan would let you fully own the property by retirement at 60, whereas a 50-year loan would keep you in debt until age 80. In retirement, you would not only pay property taxes and maintenance costs but also continue mortgage repayments—significantly affecting your quality of life in later years.

Another frequently overlooked issue is the slower accumulation of home equity. In the early years of any mortgage, most payments cover interest rather than principal. The 50-year term’s extended duration further slows your principal repayment pace.

More severe is the dramatic surge in total cost.

Take the same example: a borrower with a $350,000 loan at 6.22% annual interest could save about $250 monthly with a 50-year mortgage. But over the full loan term, the total cost would increase by $366,000.

Lenders will likely charge higher interest rates for 50-year products to compensate for the additional 20 years of default risk, further eroding the monthly payment advantage.

(Source: NPR)

For you, the extended repayment period also means facing more life uncertainties. Starting at age 40 (the average first-time homebuyer age), a 50-year repayment term spans nearly your entire adult life, increasing exposure to risks like job loss, health issues, or family emergencies.

More concerning is that this debt may ultimately be inherited by your next generation rather than leaving them transferable assets. As Pete Carroll, Director of Public Policy at Cotality, warns: "What we’re passing on isn’t wealth and assets—it’s debt."

Simultaneously, 50-year loans fail to solve the biggest homebuying barrier: the down payment requirement. They merely defer repayment pressure rather than genuinely enhancing your purchasing capacity.

Therefore, when evaluating this option, we recommend calculating not just monthly savings but also comprehensively assessing lifetime financial health—and this debt’s profound impact on your retirement plans and family legacy.

Why Would It Push Up Home Prices?

When you see lower monthly payments, you might perceive financial breathing room. But housing economists caution that this is the core of the "affordability paradox": when credit conditions loosen, home prices often rise—not fall—due to limited housing supply.

A 50-year mortgage not only fails to change this pattern but may intensify upward price pressure—it doesn’t reduce your homebuying costs but enables you to bid higher prices for scarce housing resources.

History has repeatedly validated this pattern. In the early 2000s, when adjustable-rate and subprime loans became widespread, millions achieved homeownership—only to face mass defaults when rates rose, ultimately triggering the 2008 financial crisis.

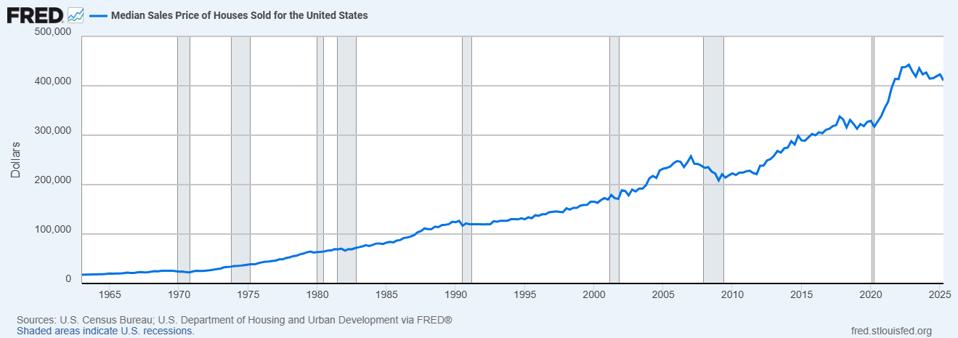

A recent example occurred during the pandemic: when 30-year mortgage rates first dropped below 3%, buyers rushed into the market, driving the U.S. median existing-home price from $274,500 in 2019 to $413,800 in 2022—a surge exceeding 40%. The increased purchasing power from low monthly payments became a catalyst for higher prices.

When your home equity grows slowly, you may find it difficult to sell or relocate even with job changes or shifting family needs. This reduced liquidity further tightens market supply, creating a vicious cycle that pushes prices higher. Ironically, policies designed to improve housing accessibility may ultimately make homes even more unattainable for the next generation.

Can It Solve Housing Affordability?

On the surface, a 50-year mortgage appears to be a practical bridge between stagnant wage growth and persistently rising home prices. But this view often overlooks the fundamental issue in housing markets: supply-demand imbalance.

No matter how lenient loan terms become, true affordability can never be achieved without sufficient housing supply.

U.S. Census Bureau data shows America faces a severe shortage of approximately 4.7 million housing units due to decades of underbuilding. Housing economists broadly agree that the real barrier isn’t loan duration but the scarcity of available homes.

For this reason, many experts question the effectiveness of 50-year loans as a solution. More relaxed financing essentially subsidizes demand, increasing the number of buyers with purchasing power but not adding a single brick of new housing. Ultimately, the monthly savings you gain could be entirely offset by rising home prices.

Genuine improvements in housing affordability will come from expanding construction, optimizing land-use policies, and implementing macroeconomic measures that stabilize long-term interest rates. These structural solutions offer far more sustainable financial health for homebuyers like you than merely extending debt cycles.

What Should Homebuyers Consider?

Before deciding on a loan, we recommend evaluating these key dimensions:

- Compare Total Costs

Low monthly payments may mask dramatically higher total costs. Always compare total interest payments between 30-year and 50-year options—not just monthly amounts.

- Adjust Homebuying Strategy

Prioritize smaller homes or increase your down payment (even by just 5%). This fundamentally improves affordability more effectively than extending debt by 20 years.

- Improve Credit Health

Every 20-point increase in your credit score may lower rates by 0.3%–0.5%. Spending three months repairing your credit report is far more cost-effective than carrying debt for two extra decades.

The Bottom Line

The 30-year mortgage once enabled ordinary families to own homes before retirement and build assets transferable to the next generation. But a 50-year loan alters this essence—when you buy a home at age 30, the likelihood of still repaying it at 80 increases significantly. This not only prolongs your debt cycle but also means your heirs may inherit property burdened by unpaid loans.

Such a solution masks the core contradiction in housing markets: home price growth has consistently outpaced family income growth. The 50-year loan makes high prices appear affordable through longer repayment terms while avoiding the fundamental need to increase housing supply.

It’s critical to recognize:

- Short-term payment reduction ≠ long-term burden reduction: total interest costs may increase by over 40%, and home equity accumulation slows significantly;

- Surface accessibility ≠ true affordability: when lower payments attract more buyers to a limited supply, home prices may rise further.

Real housing solutions require policymakers to boost supply while individuals make rational decisions within their means. When monthly payments look tempting, remember the safest financial choice is keeping your debt period shorter than your working years. This isn’t just smart financial planning—it’s responsibility for your future freedom.