Tesla Stock Hits Record High as Robotaxi Tests Ignite Market. Why Is Goldman Sachs Pouring Cold Water on Tesla?

AI Podcast

Tesla shares surged following news of fully autonomous Robotaxi tests without safety drivers, propelling its market capitalization to $1.63 trillion, surpassing Broadcom. Analysts predict significant expansion of its Robotaxi fleet. However, Tesla's traditional automotive business faces a 23% year-over-year sales decline in the U.S. due to expiring EV tax credits and boycotts. Goldman Sachs remains cautious, emphasizing the challenges of scaled expansion and profitability over technological advancement, citing intense competition from Waymo and Uber, and maintaining a "Neutral" rating with a $400 price target.

TradingKey - For Tesla (TSLA) investors, a challenging start to the year has now taken a significant turn.

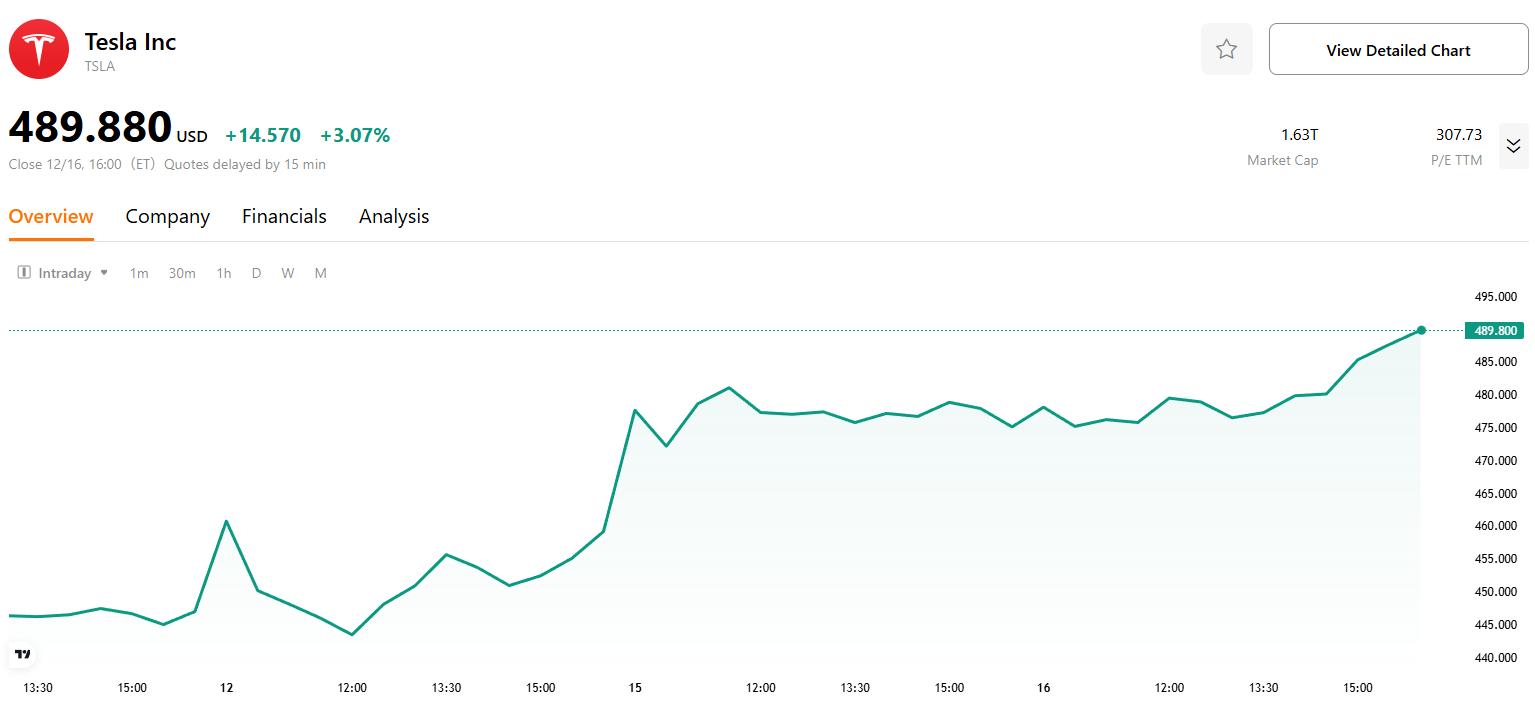

After a 36% stock plunge in the first quarter—its worst performance since 2022—Tesla shares surged overnight to a record $489.88, extending gains for a third consecutive session. The rally propelled its market capitalization to $1.63 trillion, allowing it to surpass Broadcom (AVGO) as the world's seventh-largest public company, trailing only tech giants like Nvidia (NVDA), Apple (AAPL), Alphabet (GOOGL), Microsoft (MSFT), Amazon (AMZN), and Meta (META).

The catalyst came from Austin, where Tesla this past weekend initiated fully autonomous Robotaxi tests with no safety supervisor or passengers inside. CEO Elon Musk briefly announced on social media, "Tests are underway, no one in the car," a mere six months after launching a Robotaxi pilot program with safety drivers in June.

Morgan Stanley (MS), for its part, expressed strong confidence in the development, predicting Tesla's Robotaxi fleet could rapidly expand from its current 50-150 vehicles to 1,000 by 2026. By 2035, this figure is projected to reach an astonishing 1 million vehicles, covering multiple cities across the U.S.

Wedbush analysts went further, issuing a Street-high price target of $600. They stated that "Tesla is making significant strides in advancing its AI revolution, placing autonomous driving and robotics at the core of its 2026 development."

Electric Vehicle Business Under Pressure

However, even as the stock reached new highs, Tesla's traditional automotive business is struggling.

According to Cox Automotive data, Tesla's U.S. sales plummeted 23% year-over-year to 39,800 units in November, marking their lowest level since January 2022. This downturn was not coincidental; the expiration of the $7,500 federal EV tax credit at the end of September, coupled with ongoing consumer boycotts related to Musk's political activities, has stifled sales growth.

Automotive revenue declined by 20% and 16% in the first two quarters, respectively, with deliveries falling 13%. The 12% revenue growth in the third quarter was primarily driven by a rush to buy ahead of the tax credit's expiration, rather than a genuine recovery in demand. Furthermore, the entry-level Model Y and Model 3 variants introduced in October have failed to reverse the downward trend.

Renowned investor Michael Burry earlier this month criticized the stock as "overvalued."

Goldman Sachs's Skepticism

Facing the market's frenzy, Goldman Sachs (GS), in a research report published on December 15, poured cold water on the enthusiasm. While acknowledging that the safety driver-free tests demonstrate Tesla's progress in autonomous driving technology,analyst Mark Delaney's team stated that the market's focus must shift from technological breakthroughs to two core challenges for commercialization: the pace of scaled expansion and profitability.

The report highlighted that intense market competition, particularly from the rapid deployments by rivals like Waymo and Uber (UBER), could limit Tesla's profit margins in this sector.

More critically, Goldman Sachs views the vehicle cost itself as a "relatively less critical variable" for profitability, noting that autonomous driving operators can amortize vehicle costs over extensive mileage in commercial operations.Therefore, the ability to rapidly capture and operate in more areas is more crucial than the cost per vehicle.

Goldman Sachs predicts the U.S. autonomous ride-hailing market will reach $7 billion by 2030, butcompetitors have already established dense networks. Waymo has built urban networks with its first-mover advantage, while Uber is rapidly expanding leveraging its existing mobility ecosystem. Although Tesla has garnered attention for its technological breakthroughs, it still needs to prove its commercialization capabilities.

The fierce competitive landscape led Goldman Sachs to maintain a "Neutral" rating on Tesla, with a 12-month price target of $400—implying 15.8% downside from current share prices.

The analysts concluded, "We continue to expect autonomous driving to be a key growth driver for Tesla, but we expect competition to limit the level of improvement in its profitability."

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.