The Ultimate AI Investment Guide: Opportunities, Risks, and Strategies for the Next Generation of Technology Markets

By: Viga Petar Mario

1. Introduction

TradingKey - OpenAI’s recent multi-billion-dollar partnerships—with Nvidia, AMD, and Broadcom—have flooded headlines and lifted markets, but they’ve also sparked a new round of debate: Is Sam Altman steering us toward a runaway tech bubble, or are we witnessing the foundations of a new economic epoch? Every major inflection point in technology—dotcom, mobile, crypto—brought a wave of hype followed by both breakthrough winners and sobering failures. Today, with AI powering everything from code and content to chips and cloud, the stakes and scale have never looked bigger.

Owning and controlling the production of advanced chips and foundational AI models is reshaping the industry’s profit landscape, but agile application developers and expert integration providers are also establishing powerful positions within the expanding ecosystem.

For investors, the real challenge is cutting through hype and momentum to spot the durable strategies and risks that will define AI leadership. As consumer enthusiasm and enterprise pilots put new business models to the test, only those attuned to blind spots and breakthrough trends will capture lasting opportunity. In this fast-evolving market, separating signal from noise isn’t just useful, it’s essential. The next chapter in AI will be written by those who understand both the forces driving transformation and the pitfalls that could shape the correction ahead.

2. Industry Overview

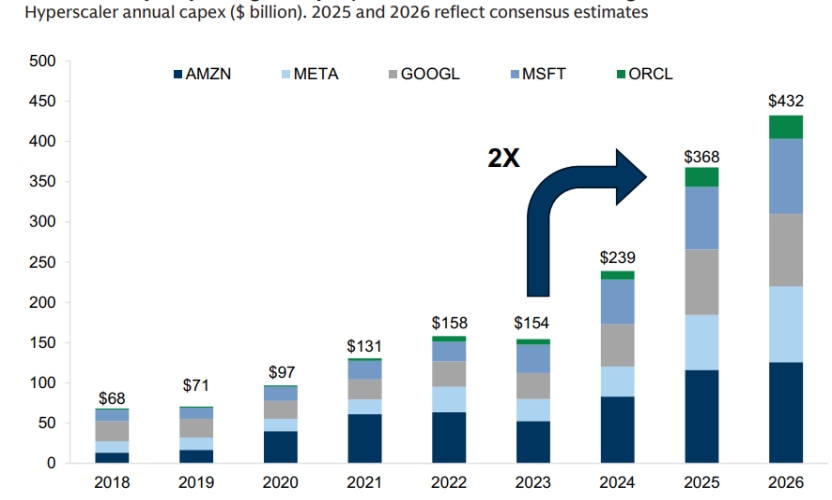

The global AI industry is not just reshaping technology, it is redefining the architecture of entire economies, pushing society into a new infrastructure era marked by exponential compute, energy, and capital demands. Unlike past digital revolutions driven by software or internet platforms, today's AI expansion relies both on the continuous expansion of algorithms and physical construction of concrete, steel, and silicon wafers. Data centers, once a niche backbone for cloud workloads, have become strategic assets, with total power consumption expected to more than double in the coming years, triggering multi-trillion-dollar waves of corporate capex and spurring new financing solutions, public-private partnerships, and innovative energy strategies.

Source: Goldman Sachs

AI’s economic impact is rapidly permeating consumer, enterprise, and industrial domains. Adoption speeds outpace monetization: ChatGPT’s weekly users are growing much faster than the company’s revenue. Consumer engagement is high, but there remains significant untapped potential to convert this usage into commercial returns. Within enterprises, companies are pursuing AI to drive operational efficiency, reduce friction, and unlock productivity, yet relatively few have achieved tangible profit gains. Rapid adoption has yet to translate into realized business value for most organizations. The industry is still developing, and there is substantial room for new entrants to succeed, whether they are disruptive startups, government-backed projects, or large, vertically integrated technology leaders.

The investment narrative is unique: historic market cycles (railroads, electrification, telecom, internet) reappear, but strategic assets have shifted from commodity resources to digital infrastructure and AI-driven compute factories. Power supply and grid modernization now determine industry tempo, with energy availability increasingly influencing site selection and investment flows. Capital markets have broadened to accommodate these needs: private credit, joint ventures, asset-backed securities, and new development models channel unprecedented funding into AI’s material foundations.

From a global view, AI infrastructure investments are also instruments of geopolitical strategy, with nations leveraging data centers and technology alliances as tools of influence and national security. While market concentration and capex surges echo past bubbles, current solid balance sheets, diversified financial structures, and measured valuations argue against imminent collapse, suggesting the AI industry’s supercycle is still in its early chapters, with vast opportunity for broadening leadership, sectoral returns, and the emergence of next-generation technology champions.

-61f533f7a4c9482b88ca5cf6afc7ad23.jpg)

Source: Goldman Sachs

3. AI Ecosystem Breakdown

The AI ecosystem is made up of three key layers—infrastructure, core tech, and applications—that stack up to fuel innovation and real-world business values. Infrastructure handles the nuts-and-bolts physical and power needs for computing, core tech dives into hardware muscle and data models, and applications turn AI into hands-on fixes across industries, creating a smooth, interconnected tech setup.

3.1 Infrastructure Layer

The infrastructure layer is the bedrock of the AI world, supplying the raw physical and energy muscle to keep AI humming—think power grids, energy sources, data center setups, and cooling gear. These pieces deliver reliable power, space, and a steady environment, acting as the unseen backbone of the entire AI supply chain.

3.1.1 Energy Supply: This is all about generating power from things like nuclear plants, gas-fired stations, or renewables such as wind and solar, to feed the massive appetites of AI data centers.

Why It Matters: A single AI data center can guzzle as much electricity as a whole nuclear reactor. Pairing small modular reactors (SMRs) with green energy looks like a solid long-term fix for AI's power hunger, and it's pulling in tons of investor cash.

Key Players:

· Constellation Energy (CEG): America's top nuclear outfit, running several plants and gearing up SMRs to power AI hubs.

· Vistra Corp (VST): A mixed-bag energy firm blending gas and nuclear, ready to crank out huge amounts of power for AI setups.

· Oklo Inc. (OKLO): Pioneers in SMR tech, building tiny nuclear reactors with backing from Sam Altman; they've got a 12GW pipeline for data centers and look set for big growth.

3.1.2 Power Grid: The grid is the delivery network that shuttles electricity from plants to users like AI data centers, featuring high-voltage lines, substations, and smart tech for smooth, reliable flow.

Why It Matters: With AI centers ballooning, worldwide power needs could jump 15-20% by 2030, mostly thanks to AI. Upgrading grids with smarts and weaving in renewables is where the smart money's going.

Key Players:

· NextEra Energy (NEE): The biggest U.S. renewable player, heavy on wind, solar, and smart grids to supply clean energy to AI operations.

· Duke Energy (DUK): An old-school power heavyweight dishing out steady supply while pouring funds into modernizing the grid for AI's rising demands.

3.1.3 Data Centers: This covers the physical and networking bones for AI computing—server racks, storage units, network hardware, and the buildings themselves—serving as the hub for high-powered computing and data processing in AI.

Why It Matters: The global data center market is on track for 10%+ yearly growth to 2030, driven hard by AI's need for more grunt. Things like prefab centers and edge setups are opening up fresh investment angles.

Key Players:

· Equinix (EQIX): Top global data center REIT, offering super-connected spaces that back major AI cloud services.

· Digital Realty Trust (DLR): Builds and runs data centers tailored for AI firms' massive scale needs.

· CoreWeave (CRWV): Leads in AI cloud setups, with networks tuned for GPUs to speed up training and inference.

· Nebius Group (NBIS): Runs efficient GPU clusters, prioritizing green power and worldwide growth.

· Cipher Mining (CIFR): Industrial-scale operator focused on HPC and dense computing for AI tasks.

· Iris Energy (IREN): Specializes in renewable-powered centers with high-density designs, ideal for AI clouds and HPC.

3.1.4 Cooling Systems: Using methods like liquid, air, or immersion cooling to tame the heat from powerhouse AI chips, keeping gear stable and lasting longer.

Why It Matters: AI rigs run way hotter than old-school servers, so cooling affects efficiency and bills big time. Cutting-edge options like liquid cooling can slash energy use by 30%, making it a game-changer for data center edges.

Key Players:

· Vertiv Holdings (VRT): Delivers cooling and power solutions, riding the wave of AI's cooling boom.

· Schneider Electric (SBGSY): Liquid cooling pros, teaming with NVIDIA on AI designs; their 2025 Motivair acquisition cements top-dog status.

3.2 Core Technology Layer

3.2.1 Hardware and Computing Layer

The hardware and computing layer is the driving force of the AI ecosystem, providing computational power for data processing, model training, and inference. It includes storage and memory, networking, logic and chipsets, and system integration, relying on the infrastructure layer while enabling the data, model, and application layers.

3.2.1.1 Storage and Memory: Think of this as AI's memory vault: holding and fetching huge data piles. High-bandwidth memory (HBM) speeds things up, while SSDs store training sets and models.

Why it matters: Big AI models gobble terabytes of memory and petabytes of storage. HBM3/3e and HBM4 demand is eyeing 30%+ annual growth from 2025-2030, hitting efficiency and costs head-on.

Key Players:

· Micron Technology (MU): Top dog in HBM and DRAM, with 2025 HBM3e shipments exploding from AI server hype.

· Western Digital (WDC): Zeroes in on big-capacity enterprise SSDs and HDDs for AI centers.

3.2.1.2 Networking: The fast lanes in data centers: high-speed switches and cards for seamless server-to-server data flow, enabling spread-out AI jobs.

Why it matters: Training needs insane bandwidth between nodes; 400G/800G Ethernet and InfiniBand are booming, with a $20B market by 2025. It's all about scaling and speed.

Key Players:

· NVIDIA (NVDA): Snagged Mellanox to rule AI networking with InfiniBand and Ethernet.

· Arista Networks (ANET): Cloud and AI switch experts, grabbing more share in 2025.

· Cisco (CSCO): Rolled out Silicon One P200 and OCS-2023 router for long-haul AI center links, handling data surges.

3.2.1.3 Logic and Chipsets: AI's brain: GPUs, TPUs, ASICs, and quantum processors tackling heavy math, neural nets, and tweaks. Quantum uses qubits for mind-bending complexity, potentially revolutionizing AI niches.

Why it matters: Chips are compute kings; AI chip market hits $150B by 2025, over half the hardware pie. Performance dictates model zip and smarts.

Key Players:

· NVIDIA (NVDA): Reigns supreme with Blackwell GPUs like B200 for training/inference.

· Advanced Micro Devices (AMD): Challenges with MI300 accelerators, big 2025 revenue bumps.

· IonQ (IONQ): Quantum leader with killer algorithms and low errors, building versatile processors for AI tweaks, drugs, and materials.

· D-Wave Quantum (QBTS): Annealing specialists—practical, no ultra-cold needed—for optimizing AI in logistics, finance, emergencies.

3.2.1.4 Motherboards and System Integration: The framework: piecing together chips, memory, networks into full AI servers for turnkey platforms.

Why it matters: AI server demand surges 40% in 2025; smart integration boosts output, cuts costs—key hardware glue.

Key Players:

· Super Micro Computer (SMCI): AI server integration pros, linking with NVIDIA/AMD for peak performance.

· Dell Technologies (DELL): Enterprise AI servers, 2025 models with liquid cooling and GPU clusters.

3.2.2 Data and Model Layer

This is the smart core of AI, turning raw data into polished models with backing from infrastructure and hardware. It includes acquiring/processing data, integrating/analyzing it, developing/optimizing models, and deploying/distributing them—sparking application-layer breakthroughs. Market forecasts: $45 billion in 2025, over $120 billion by 2030, at 22.5%-25% CAGR.

3.2.2.1 Data Acquisition and Processing: AI's raw materials workshop—gathering data from sensors/web, storing it securely, and prepping it by cleaning and formatting for use.

Why it matters: Solid data underpins model training; junk in means junk out, risking biases. Streamlined handling speeds up development and trims expenses.

Key Players:

· Informatica (INFA): Pros in data cleanup/integration, with 25% growth in AI governance revenue for 2025, streamlining enterprise prep.

· IBM (IBM): Watson amps up collection/storage, enhancing cloud processing for big models in 2025.

· Amazon (AMZN): AWS S3/Glue handle storage/cleaning, building pipelines for generative AI.

3.2.2.2 Data Integration and Analysis: The control room for data—merging sources, organizing/securing them, and mining insights with AI for business gains.

Why it matters: Integration breaks silos for full AI inputs; management ensures compliance (e.g., GDPR); analysis turns data into decisions, potentially hiking accuracy 50% by 2025. Key for transformations in retail/finance, where it sways project outcomes.

Key Players:

· Informatica (INFA): Robust platforms for fusing data, speeding AI-driven real-time choices.

· Teradata (TDC): Vantage excels in management/analysis, boosting finance AI insights and utilization.

· Oracle (ORCL): Cloud tools refine integration/analysis, with 20% AI revenue uptick in 2025 for governance.

3.2.2.3 Model Development and Optimization: AI's lab for crafting neural nets from prepped data, managing iterations to fine-tune performance and cut biases.

Why it matters: Development trains networks for predictions/decisions; optimization refines via feedback, shortening cycles and lifting accuracy. Market to $200 billion in 2025, powering from labs to business, especially generative AI where data/model synergy drives output quality.

Key Players:

· Google (GOOGL): TensorFlow for development, with 2025 Gemini tools leveraging data for efficient large-model training.

· IBM (IBM): Watson Studio hones enterprise models with data insights.

· Amazon (AMZN): AWS SageMaker speeds generative AI iterations.

· Microsoft (MSFT): Azure AI uses AutoML for efficient model tweaks in generative apps.

3.2.2.4 Model Deployment and Distribution: The shipping point for AI—placing data-trained models on cloud/edge and sharing pre-trained ones (open-source giants) for broad rollout.

Why it matters: Deployment enables low-latency, real-time responses; distribution cuts redo costs and accelerates adoption. 40% growth in 2025 market, fueled by cloud, critical for competitiveness in self-driving/medical AI.

Key Players:

· IBM (IBM): Watsonx streamlines deployment, broadening enterprise reach with data-powered services in 2025.

· Amazon (AMZN): AWS Bedrock shares pre-trained models, easing costs for devs.

· Microsoft (MSFT): Azure AI deploys for over 70,000 firms in 2025, optimizing pre-trained solutions.

· Google (GOOGL): Vertex AI handles quick deployment/distribution, tailoring pre-trained models for edges.

3.3 Application Layer

The capstone where AI hits the ground, building on lower layers to create products/services. Via enterprise, consumer, and sector-specific uses, it weaves AI into business and life for economic/social wins. Market: $80 billion in 2025, $250 billion by 2030, 25%-30% CAGR.

3.3.1 Enterprise Applications: AI's business backbone in CRM, ERP, HR, marketing automation, and analytics—automating, deciding, and efficientizing to slash costs and sharpen edges.

Why It Matters: Handles routine work, forecasts (e.g., sales), and optimizes (e.g., supply chains) for better ops. Broad appeal drives steady demand; Gartner sees over $100 billion by 2030, key to monetizing AI via revenue boosts.

Key Players:

· Salesforce (CRM): Einstein blends analytics/customer tools for solid leadership.

· ServiceNow (NOW): AI IT management thrives on digital shifts, growing fast.

· UiPath (PATH): Automation powerhouse with high demand for process streamlining.

3.3.2 Consumer Applications: Blends AI into everyday with assistants, recommenders, social analytics, virtual helpers, and custom content based on user habits.

Why It Matters: With mobiles/smarts everywhere, user numbers soar—Statista pegs $50 billion in 2025. Boosts experiences/ads, fueling consumer spending and AI's mass impact.

Key Players:

· Amazon (AMZN): Alexa's voice smarts and recommenders personalize shopping with huge data troves.

· Alphabet (GOOG): Assistant's language prowess and YouTube algorithms extend watch times, securing search/ad leads.

· Meta (META): Algorithms fine-tune social feeds/ads, sticking users and maxing revenue.

3.3.3 Industry-Specific Applications: Custom AI fixes for sectors like health, finance, manufacturing, retail, logistics—tackling unique issues.

Why It Matters: High barriers yield fat margins; solves pains, drives digitization in growth areas. IDC forecasts over $80 billion by 2027, vital for differentiated AI plays.

Key Players:

· Palantir (PLTR): Platforms tailor for retail/finance/gov, analyzing data for personal outcomes; defense deals amp security/trust.

· CrowdStrike (CRWD): AI spots network threats in real-time, safeguarding data with rapid expansion.

· Intuitive Surgical (ISRG): Da Vinci robots use AI for precise patient analysis, leading med tech.

Through tight integration of infrastructure (energy, grids, centers, cooling), core tech (hardware/compute, data/models), and applications (enterprise, consumer, industry-specifics), the AI ecosystem builds a full value chain. From power to chips, data processing to model rollout, it propels AI from basics to impact. Projections show the market topping $100 billion in 2025, charging ahead at 20%-30% CAGR to 2030, reshaping tech and economies worldwide.

4. Companies Building AI Applications

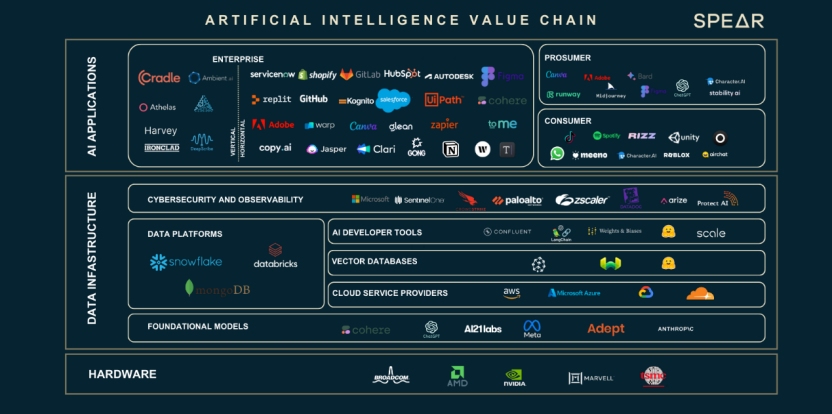

The surge in AI adoption is driving a multi-layered ecosystem, with value creation anchored by advances in both infrastructure and software. Behind every breakthrough in applications and models, there is massive investment in technology infrastructure, the essential backbone that enables scale. Leading semiconductor companies such as Nvidia, Intel, AMD, and TSMC produce specialized chips powering model training and inference, while cloud hyperscalers like Microsoft Azure, AWS, Google Cloud, and Oracle, and dedicated data center operators, provide the high-performance computing resources and networks needed to host and serve global AI workloads. These partners are expanding processing and storage capacity, innovating in energy management, and building resilient, next-generation data centers to keep up with AI’s relentless growth.

With these foundations in place, the ecosystem advances through three intertwined software-driven layers: foundation model providers, application leaders, and service integrators. Together, these groups shape the pace, breadth, and monetization of the generative AI wave.

-42d851631dd5427c9072aa6ed575d3fc.jpg)

Source: Spear Invest

4.1 Foundation Model Providers: The Base Layer

Foundation models are large, general-purpose AI systems powering today’s most advanced generative AI applications. These models act as the platform for the new AI era, enabling everything from chatbots and virtual assistants to coding copilots and creative design tools.

Globally, the most influential providers are OpenAI (ChatGPT), Google (Gemini), Anthropic (Claude), xAI (Grok), and major Chinese firms including DeepSeek and Alibaba (Qwen). As user preferences and use cases become more differentiated, organizations and individuals increasingly match each platform’s unique strengths to their specific needs in coding, productivity, creative work, or industry-focused applications—details highlighted in the comparison table below.

Provider / Model | Core Strengths | Best At | Typical Users / Scale |

OpenAI ChatGPT | All-purpose, coding, writing, creativity, integrations | Reliable assistant, coding, business docs | Global leader; 800M+ weekly users; businesses, developers, students |

Anthropic Claude | Safer outputs, coding, long docs | Coding, legal, regulated uses | 30M+ monthly users; enterprises, compliance-driven sectors |

Google Gemini | Multimodal (text, images, audio, video), Google suite integration | Productivity, summarization, workspace | 400M+ monthly users; Google suite users, knowledge workers |

xAI Grok | Real-time/web/social, humor, creativity | Social media, trending news | 35M+ monthly users; Gen Z, social/news consumers |

Alibaba Qwen | Multilingual, enterprise, commerce | Enterprise, finance, e-commerce | Asia-Pacific businesses; 2.2M corporate accounts |

Each provider generates revenue through a unique mix of subscriptions, enterprise API licensing, and strategic partnerships, with specific breakdowns shown in the table below.

Provider | API Usage | Enterprise Subscription | Consumer Subscription | Partnerships / Other | Notes |

OpenAI GPT | ~15–20% | ~25–30% | ~55–60% | <5% | Majority from subscriptions |

Anthropic Claude | ~60% | ~15% | ~15% | <10% | API-led, enterprise rising |

Google Gemini | ~20% | ~25–30% | ~20% | ~30% | Workspace + ads/hardware |

xAI Grok | ~10% | ~10% | ~70–75% | <10% | Bulk via X Premium+ |

Alibaba Qwen | ~20% | ~40% | ~10–15% | ~25% | Cloud/partner dominant |

4.2 Application Layer Leaders: Bringing AI to End Users

The application layer is where AI’s value manifests directly in daily activities for both consumers and businesses Leading players include enterprise software giants like Microsoft (Copilot), Google (Google Gemini Workspace), Salesforce (Einstein), Workday (AI), and ServiceNow (Now Assist), alongside a wide spectrum of consumer and vertical platforms such as Duolingo (Max), Intuit, Spotify, Adobe (Firefly), Canva, and Tempus AI.These companies leverage advanced AI, from generative models to recommendation engines, to deliver smarter automation, personalization, and content creation at scale.

AI-native startups continue to break new ground with entirely AI-powered apps, intelligent assistants, workflow generators, and industry-specific tools, targeting anything from knowledge work to education and design. In this environment, embedded AI has become a key differentiator, unlocking user engagement, loyalty, and new business models.

Source: Spear Invest

However, the entry barrier is not fixed. Next-generation challengers, often startups or spinouts from foundational labs, can use public APIs (from OpenAI, Anthropic, or open-source models) to rapidly prototype new tools.

AI monetization at the application layer remains closely tied to bundled and premium subscriptions, usage-based fees (including API/platform access), data partnerships, advertising, and in some cases, marketplace or in-app purchase models. As generative AI becomes core to mainstream apps, these revenue channels will diversify, but for now, AI revenue is blended into overall product earnings and is growing as adoption accelerates.

4.3 Service Integration: Enablers of Enterprise Transformation

While application layer solutions deliver ready-to-use tools, most enterprises require expert partners to adapt, integrate, and scale AI models within their complex systems, data environments, and compliance frameworks. Service integrators bridge this gap, bringing specialized consulting, technology deployment, and industry know-how to large-scale digital transformation projects.

Category | Leading Companies | Core Role | Example Services |

Consulting/Integrator | Accenture, IBM, Capgemini, EY | Custom AI strategy, integration at scale | End-to-end deployment, compliance, change management |

Cloud Provider | Microsoft Azure, AWS, Google Cloud, Oracle | Host, serve, and scale GenAI & LLM workloads | Cloud hosting, model fine-tuning, data lake ops |

Data & Analytics Platform | Databricks, Snowflake | Data unification, model development, analytics AI | Custom model tuning, integration, infrastructure |

Vertical Specialist | Palantir , Optum (UNH), Guidewire | Industry-specific AI systems for regulated domains | Custom AI workflows, security, compliance |

While application providers deliver standardized AI solutions, service integrators are essential for translating AI innovation into real enterprise value. They help clients overcome technical, compliance, and organizational hurdles, ensuring that GenAI tools are effectively adapted and scaled within each unique environment. As enterprises move from small-scale pilots to full operational transformation, this integration layer becomes indispensable.

For service integration leaders, AI-related monetization is still blended with broader digital transformation revenues. However, for their AI-specific business, revenue is typically structured with about 50–70% coming from large-scale professional and consulting projects, such as custom AI implementations, enterprise-specific advisory, and regulatory support—while 30–50% is generated by managed services including cloud hosting, AI system monitoring, and ongoing operational support. Proprietary integration software sales contribute less than 10%. Overall, AI accounts for only a small but rapidly growing portion of these companies’ total revenue, and specific financial disclosure around GenAI remains limited at this stage.

Monetization for service integration leaders remains intertwined with broader digital transformation revenues; AI-specific income is typically structured as 50–70% from large professional and consulting engagements, including custom solutions, advisory services, and regulatory support, and 30–50% from managed services (cloud hosting, system monitoring, ongoing support). Proprietary integration software contributes less than 10%. While AI still accounts for a modest share of total revenue today, this segment is growing rapidly.

In summary, looking ahead, the next major opportunity in AI applications is most likely to emerge on the consumer side, with foundation model providers positioned to lead thanks to viral expansion, platform scale, and diverse monetization channels including subscriptions, APIs, app stores, advertising, cloud partnerships, and hardware integration. As foundational models power ubiquitous digital assistants, creative tools, and everyday personal apps, some leading application companies may still play important roles in this evolving ecosystem. At the same time, the enterprise market will remain significant, as business-focused application and service integration layers continue to provide essential value through workflow automation, compliance, and industry transformation, though they face growing exposure to competitions.

5. AI Investment Strategies

As you can see from the previous sections, understanding the AI value chain is not a simple task due to the complexity of the value chain itself with various different players and functions, and the technical nature of these businesses (for example, understanding the differences between what NVIDIA, Broadcom or ASML requires a certain level ot familiarity with highly technical concepts).

Investing in AI adds another level of complexity in the whole picture, where investors should not only understand the business operations but also understand the investment opportunities coming with it. Similar to other industries and investment themes, people should be able to have a solid investment framework to evaluate not only the potential returns but also the risk associated with investing in AI stocks.

Here we have four investment strategies that can provide solid exposure to the AI boom, and at the same time manage the potential risks.

Strategy 1: Big AI scalers over pure-play AI companies

We can roughly divide the AI players into two groups, the incumbents and the contenders. The incumbents are the large established players, part of the “Magnificent Seven” like Nvidia, Microsoft, Amazon, Alphabet, and Meta.

On the other hand, we have the emerging players - companies like OpenAI and Anthropic (both operating LLMs), CoreWeave and Nebius Group (both infrastructure providers that rent out GPU-powered data centers for AI workloads), Snowflake and Databricks (data platforms) and Palantir and AppLovin (AI tools).

We believe investing in large incumbent players provides a more compelling risk-reward case. Companies like Google and Microsoft have already established businesses with dominant market shares in their respective areas (Google in search and advertising, Meta in social media and advertising; Microsoft in enterprise software). Financially, these companies have great profit margins and positive cash flows due to their legacy businesses.

AI competition is very fierce for all players, but the dominant market share of the big AI scalers provides a very solid competitive moat, while their solid cash reserves and cash flows can help them further invest into AI and stay ahead, and this means hiring the best engineers and acquiring the most promising AI startups. The limited downside here is that even if there is slowdown in AI development, there won’t be a significant existential threat for these companies as their original businesses will bail them out.

The downside of this is the fact that, unlike the big AI scalers, emerging pure-play AI companies may bring way more explosive investment returns over the short term. For instance, in the last twelve months, PLTR stock has risen by over 300%, while CRWV is up nearly 250% for the same period.

Strategy 2: Different sections of the AI value chain through ETFs

As we already got familiar with it, the AI value chain has many nodes - energy providers, data center scalers, chip designers, cloud providers, app developers - you name it. Investors can have exposure with ETFs that span different segments of the AI value chain, offering broad diversification and reduced single-stock risk. Examples of such ETFs include the iShares Semiconductor ETF (SOXX), which tracks the NYSE Semiconductor Index.

With top holdings being the major semiconductor players like Nvidia, AMD, and Intel. Also, there is Global X Artificial Intelligence & Technology ETF (AIQ), with a broader focus on tech enablers like cloud computing and includes names like Microsoft (Azure), Amazon (AWS), and Alphabet (Google Cloud), which dominate AI cloud services, alongside software firms like ServiceNow (NOW).

A slightly overlooked segment of the AI value chain is the energy providers. With the growth of data centers and computing power, the electricity consumption will increase from 4% to 12% of the total US power consumption. The Defiance AI & Power Infrastructure ETF (AIPO) tracks this niche segment with energy names that can fuel the future AI rise like Constellation Energy Corp (CEG), GE Vernova (GEV), Eaton Corp (ETN), Vertiv Holdings (VRT) and Oklo (OKLO).

Certain limitations of using ETFs include potential overlaps in top holdings—many AI ETFs are weighted toward a few mega-caps—and sensitivity to broader tech sentiment. Also, we have management fees incurred when we put money in any type of pooled investments like ETFs.

Strategy 3: Invest in non-tech companies that are implementing AI solutions and applications

Technology is not just an isolated industry, but it affects every aspect of our daily lives, and as the driving force in technology nowadays, we can say the same about AI. Thus, while chasing exposure to AI, investors can look beyond tech and search for industries that can directly benefit.

One such industry is healthcare. In healthcare, for instance, Pfizer (PFE) employs AI for accelerated drug discovery, using machine learning to analyze vast datasets and predict molecular interactions, which has shortened development timelines and boosted R&D productivity. Similarly, Moderna (MRNA) leverages AI in mRNA vaccine design, demonstrating how biotechnology intersects with computational biology. Other non-tech examples include Walmart, which increasingly uses AI for supply chain optimization.

As we see from the above examples with Pfizer, Moderna and Walmart, AI adoption is more prevalent in mega caps due to their extensive financial resources and economies of scale, however, other players like Tempus – an emerging healthcare company leveraging AI for diagnosis and drug discovery

The main investment upside here is the enormous area for disruption that AI can have in traditional sectors and on the limited downside, we have the relatively low valuations of non-tech stocks compared with the tech ones. Thus, companies from various industries will be able to increase revenues and cut costs.

However, a downside of this strategy is that non-tech firms may be slower in adopting AI than tech firms.

Strategy 4: Invest in non-US AI players

In the last few years, the AI narrative has mostly been revolving around the US stock market, and this makes perfect sense considering the US tech firms are at the forefront of innovation. However, the current valuations of the AI-themed US stocks are not low anymore, and investors may want to explore overseas for further AI wins.

For example, Chinese tech giants like Alibaba and Baidu are following the same AI playbook as their US tech giants - investing massive amounts in AI, developing large language models, operating massive cloud businesses, and even trying to develop proprietary AI chips. The difference, however, is that Chinese AI plays are at much lower valuations. Also, if we zoom in to Europe, we can see players like ASML (lithography machines used for AI chips), Nebius (AI infrastructure provider) and SAP (enterprise software).

A potential limitation of this kind of strategy is the relatively small investment universe, as the non-US AI development is in a quite early stage. If we exclude the above-mentioned players from Europe and China, the majority of the non-US AI companies has a long way to catch up in this. Also, we should note that venture funding is way more abundant and sophisticated in the states than overseas.

Strategy | Key Examples | Pros | Cons |

Big AI Scalers | Nvidia, Microsoft | Strong moats, cash flows | Less explosive growth |

ETFs | SOXX, AIQ, GEV, OKLO, ETN, VRT, CEG | Diversification, low effort | Fees, mega-cap overlap |

Non-Tech Adopters | Pfizer, Moderna, Walmart, Tempus | Sector disruption, low valuations | Slower adoption |

Non-US Players | Alibaba, Baidu | Cheaper valuations | Geopolitical risks, early-stage |

6. Opportunities, Risks and Trends

6.1 Opportunities and Trends

The opportunities in AI will remain lucrative in the future. In the previous section we covered some of them-investing in large AI scalers, investing in non-tech adopters and even investing in energy providers for AI. In 2023, McKinsey estimated that AI will contribute $3.5-$4.4 trillion in economic value by 2030, across all sectors – a number bigger than almost every country’s GDP

But the impact goes way beyond investing. As we will see large established players, as well as emerging players integrating with each other, collectively boosting the computing power and the level of sophistication of the AI models, this will make AI a catalyst for other trends including quantum computing and internet-of-things, further blurring the boundary between our physical world and the alternative virtual reality.

However, in the world of investing, high returns always carry substantial investment risks. Some of these risks are already known:

6.2 Risks

6.2.1 High valuations

After the rally, a lot of AI stocks are traded at very high valuations.

Examples include (but not limited to):

· Nvidia at 30x Forward PE (not very high compared with other AI players, but still relatively high compared to the average PE of the S&P 500).

· PLTR at 217x forward PE ratio – perhaps the highest valuation among S&P constituents.

· Even OpenAI, which is not listed, is valued at $500 billion while its revenue is just $14 billion (35x P/S ratio).

These elevated valuations represent the optimism investors have about AI, but they also leave little margin for error; a slowdown in capex or disappointing earnings could trigger sharp corrections.

6.2.2 Intense competition

Historically, there has always been very intense competition in the tech sector, and we see this in AI. LLMs like OpenAI’s ChatGPT, Google’s Gemini, Anthropic’s Claude, Perplexity, and xAI’s Grok all compete for market share. Considering we are at a very early stage of this competition, the outcome is highly unpredictable, and it depends on which player will develop the most advanced technology and the most sustainable business model.

6.2.3 Circular transactions and financial sustainability

In recent months, we started to observe complex financial transactions among chip makers and AI scalers involving buying and selling GPUs, investing in each other's stocks, propping each other’s valuations. This started to resemble more of financial engineering and even reminiscing of the late stages of the dot-com bubble.

For instance, Oracle’s $300 billion cloud deal with OpenAI in September 2025 raised eyebrows, as it appeared to inflate valuations through cross-investments rather than deliver immediate economic benefits. Such transactions can distort market perceptions and potentially mask a weaker-than-expected demand, increasing the risk of correction.

This also raises the question of how and when companies like OpenAI, with less than $15 billion of revenue but capex needs of hundreds of billions of dollars, can become profitable.

6.2.4 Geopolitical tensions

AI is not simply an economic and technological topic anymore; it is also a political topic.

Geopolitical risks can disrupt the AI supply chain, particularly for chipmakers. Taiwan’s TSMC, which produces 80% of advanced AI chips, is central to US-China tensions, with export controls limiting China’s access to cutting-edge semiconductors. There is also trade restrictions imposed on Nvidia, selling its most advanced products to China.

Rare earth shortages, critical for chip production, can often become a hostage to potential trade disputes.

6.2.5 Government regulations

Government support can be crucial for AI; however, poorly designed policies can significantly hinder the development. Strict data regulations can prevent AI companies’ access to data, a crucial ingredient for developing sophisticated models – just what we see with the EU’s General Data Protection Regulation (GDPR).

In addition, energy restrictions, such as limits on nuclear or coal for data centers due to environmental reasons could hinder AI scalability, particularly for cloud providers like AWS, Azure, and Google Cloud.

6.2.6 Black swan events

The risks mentioned above are already known, however, there also might be risks that are currently unknown to us and extremely hard to predict. When such risks materialize, they will lead to so called “black swan events” which can have great severity. The most recent such event was the emergence of COVID-19, which led to massive corrections in the markets, disrupting the global economy. How and when the next such black-swan event will appear, we cannot predict, making it hard to prepare for it.

Risk | Example | Impact |

High Valuations | Nvidia (30x PE), Palantir (217x PE) | Sharp corrections if earnings disappoint |

Geopolitical Tensions | TSMC, Nvidia export controls | Supply chain disruptions |

Regulations | GDPR, energy limits | Slower AI development, higher costs |

Black Swan Events | COVID-19 market crash | Unpredictable market corrections |

7. Conclusions

AI is not only changing how technology works. It’s fundamentally rewiring the logic of global industry, investment, and competition. The ecosystem is deeper than any single trend, stretching from chip foundries and data centers to foundational models, enterprise workflows, and vertical apps used every day. Investments in infrastructure, energy, and talent are as critical as app-layer innovation. Platform leaders like OpenAI, Google, and Microsoft vie for dominance, but startups and service integrators retain power to disrupt and reshape value chains.

We face both exceptional upside and unique risks: market leaders enjoy deep moats and cash flows, but fierce competition, regulatory pressures, and complex financial structures create volatility and uncertainty. Success will depend on clear frameworks—mapping the AI stack, focusing on sustainable advantages, and watching for hidden risks such as valuation excess, cyclical hype, and geopolitical shocks. The next chapter in AI investing belongs to those who can navigate complexity, anticipate disruption, and separate signals from noise.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.