NeoClouds Earnings: CoreWeave and Nebius Deliver Strong Growth, But Investors Stay Cautious

TradingKey - This week, two of the most closely watched firms in AI infrastructure—CoreWeave and European-based Nebius—published quarterly results. Both companies reported strong top-line growth, backed by expanding demand and significant customer traction. But the market reaction was muted. Shares in both firms declined following their earnings announcements, signaling ongoing investor uncertainty about how sustainable this infrastructure cycle’s growth really is—and whether a soft landing is even possible amid current challenges.

CoreWeave Tops Expectations, But Leverage Comes Back Into Focus

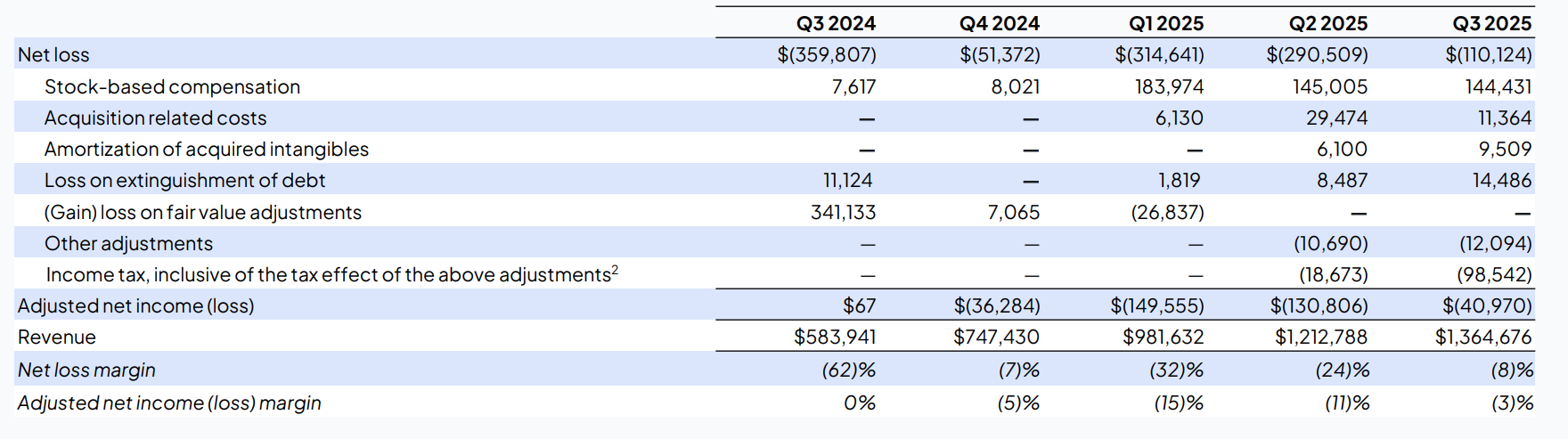

CoreWeave’s latest report sent a mostly positive message. Revenue for the quarter reached $1.4 billion, up 134% YoY. Net losses narrowed to $110 million, a substantial improvement from the prior year, and earnings came in ahead of consensus estimates.

In recent months, CoreWeave has also secured several high-profile agreements that helped reinforce its lead in the AI cloud landscape. These include a $14.2 billion multi-year compute deal with Meta—a critical win for footprint expansion—and a separate partnership with Poolside to provision up to 40,000 NVIDIA GPUs across in-progress data centers.

Thanks to its deep integration with NVIDIA, CoreWeave retains priority allocation across GPU shipments—positioning it as a key resource provider in an increasingly gated compute market. Most market models continue projecting strong revenue growth ahead, supported by big tech’s expanding appetite for dedicated AI capacity.

But the capital structure underpinning that growth is beginning to raise questions. CoreWeave’s business model remains highly debt-leveraged. Many of its infrastructure expansions are financed against existing long-term GPU supply contracts, allowing the company to raise additional funds through structured refinancing.

As a result, scheduled debt repayments remain heavy. CoreWeave faces $9.7 billion in maturities due within the next twelve months. Its total debt load now stands at $14 billion—up from $11 billion last quarter, and $7.6 billion the quarter before that. Interest expense rose to $311 million this quarter, a more than threefold increase from the $104 million reported a year ago. Servicing those payments has become a growing drag on profits.

Its cash flows remain stable for now, and the company did lower its CapEx forecast for 2025 by around 40%, to a new range of $12–14 billion. Still, the overall capital intensity of the infrastructure build remains extraordinarily high—and liquidity pressures have not fundamentally eased.

Revenue guidance for the full year was also revised down modestly, to $5.05–5.15 billion (from a prior estimate of $5.15–5.35 billion). The update came primarily due to delays from third-party data center vendors, which pushed portions of contracted deployments into 2025. While the value of contracted deals remains unchanged, recognition of that revenue is slipping, which has now created timing mismatches between inflows and CoreWeave’s ongoing interest costs and internal investments. In a highly leveraged model, even short-term shifts in delivery schedules can create working capital strain.

Meanwhile, broader constraints are emerging on the infrastructure execution side. In the earnings call, CEO Michael Intrator noted a widespread bottleneck in “powered shells”—pre-energized, high-density physical enclosures that house GPU clusters. While this is not directly related to grid-level energy supply, slow construction and handoff timelines are limiting CoreWeave’s ability to bring compute capacity online.

To reduce dependency on single vendors, the company is now expanding its supply base and increasing self-built capacity. Executives expect the shortfall to ease over time.

Investor anxiety, however, is being fueled not just by delivery challenges—but by ongoing debate over the durability of AI demand itself. Is the market truly ready to absorb this much GPU supply? Are regional energy grids capable of supporting this wave of compute-heavy hosting? These questions are already being reflected in CoreWeave’s stock price, which has fallen more than 20% over the past two weeks, including a 10% decline on earnings day alone.

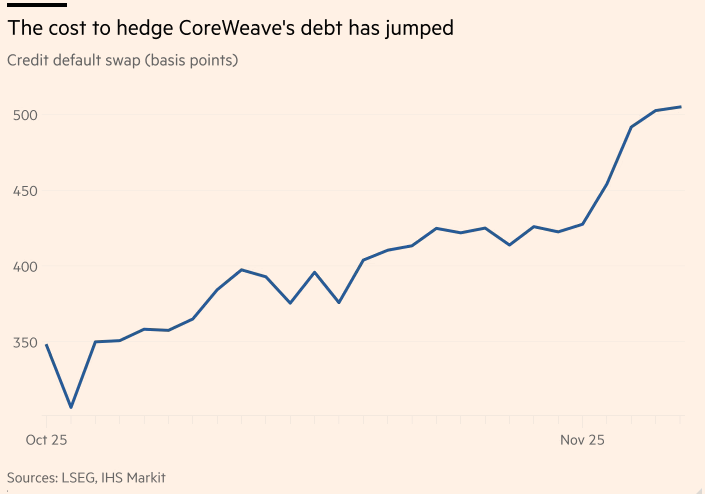

Credit markets are signaling similar concerns. The company’s five-year CDS (credit default swap) spread has widened sharply—from below 350 basis points in early October to 505 bps as of this week, highlighting growing skepticism around repayment timelines and debt service coverage.

Nebius Reports 355% Growth, High-Profile Deals—but Losses Continue to Grow

Nebius—the European-based NeoCloud startup often seen as CoreWeave’s closest peer—also posted strong numbers this week.

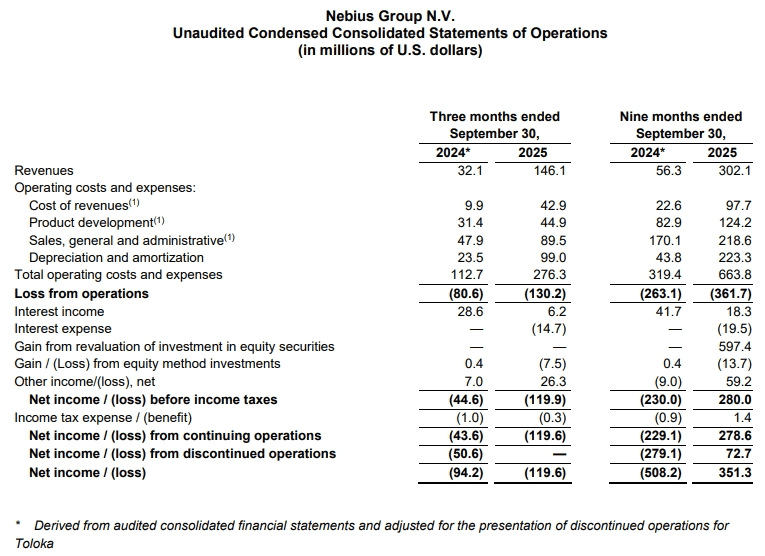

Revenue in Q3 came in at $146.1 million, a 355% increase YoY. The company also secured yet another major customer win, announcing a new five-year, $3 billion AI infrastructure agreement with Meta. This follows a $17.4 billion contract signed with Microsoft back in September. CEO Arkady Volozh noted on the call that Nebius expects its cloud division to scale nearly 7x by the end of 2026.

That expansion is already taking shape on the ground.

In Q3, Nebius launched a new data center in Kansas, where it deployed NVIDIA’s latest B200 chips for the first time. In London, the company brought its newest campus online last week—marking the first site in the UK to host 4,000 of NVIDIA’s B300 GPUs, according to public disclosures.

Still, the stock sold off more than 7% on earnings day. The reason is losses widened, and the company’s latest capital-raising plan triggered concerns over dilution.

Adjusted net loss for the quarter reached $100.4 million—up dramatically from $39.7 million a year ago. With profitability not expected in the near term, Nebius is now actively preparing to raise additional capital to fund upcoming expansion phases.

At the end of Q3, the company still held $4.9 billion in cash. But Q4 CapEx is forecasted to reach $3 billion. To bridge the gap, Nebius has disclosed a multi-part refinancing plan: it will pursue new corporate debt issuance, collateralized loans backed by GPU assets, and the sale of up to 25 million Class A common shares in an offering later this year. That equity component was one of the main triggers for the post-earnings share price drop.

Nebius is also investing in product-level differentiation. Its newly launched inference-as-a-service platform—Token Factory (NTF)—is designed to compress post-training model deployment timelines by combining fine-tuning, optimization, and inference delivery in one system. According to the company, NTF allows models like LLaMA, Qwen, DeepSeek, and Nematron to run with up to 26x cost efficiency versus proprietary alternatives. It currently delivers 99.9% platform uptime and millisecond-scale latency in production inference environments. Executives believe the product could become a growth driver within developer-focused markets.

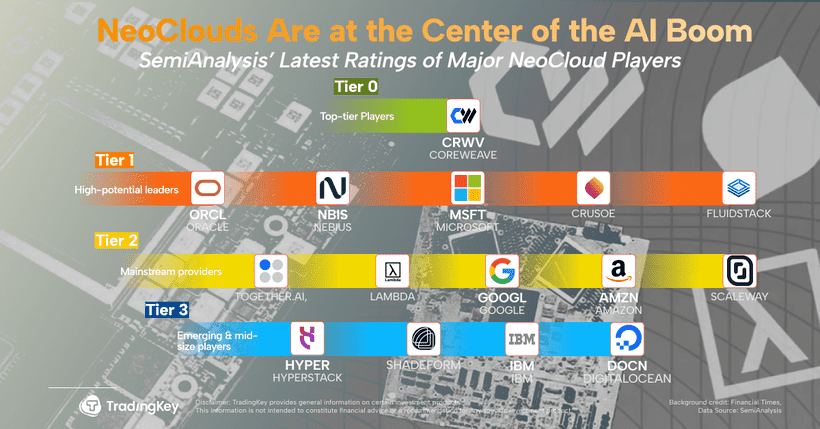

Industry Rankings Update: CoreWeave Still Leads, Nebius Closes the Gap

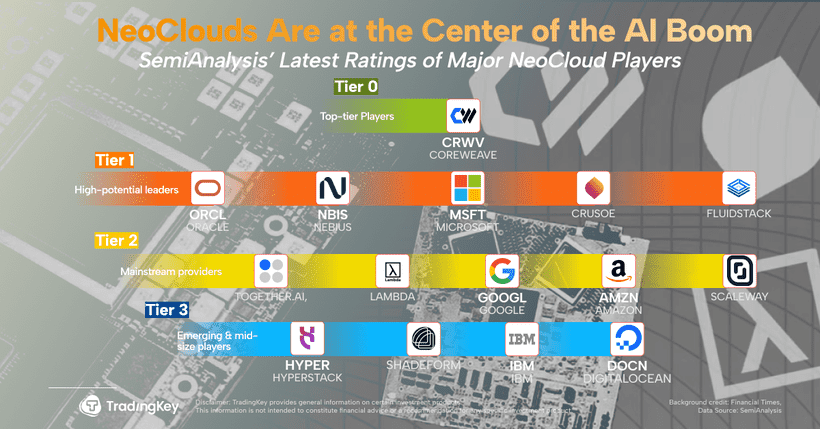

This week, SemiAnalysis published its latest sector rankings for infrastructure-focused AI cloud providers—a framework that has gained relevance as the NeoCloud category continues to professionalize.

As of November 2025, the latest tierings are as follows:

Tier 0 (Top-tier): CoreWeave

Tier 1 (High-potential leaders): Oracle, Nebius, Azure, Crusoe, FluidStack

Tier 2 (Mainstream providers): together.ai, Lambda, Google Cloud, AWS, Scaleway, Cirrascale, VULTR, Voltage Park, GCore, firmus, GMO Cloud, Tensorspace

Tier 3 (Emerging & mid-size players): Hyperstack, Shadeform, neysa, STN, GMI, RunPod, Atlas Cloud, PRIME, CUDO Compute, QUBRID, latitude.sh, Lightning AI, verda, DENV.R, IBM Cloud, DigitalOcean, HOT AISLE, BUZZ

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.