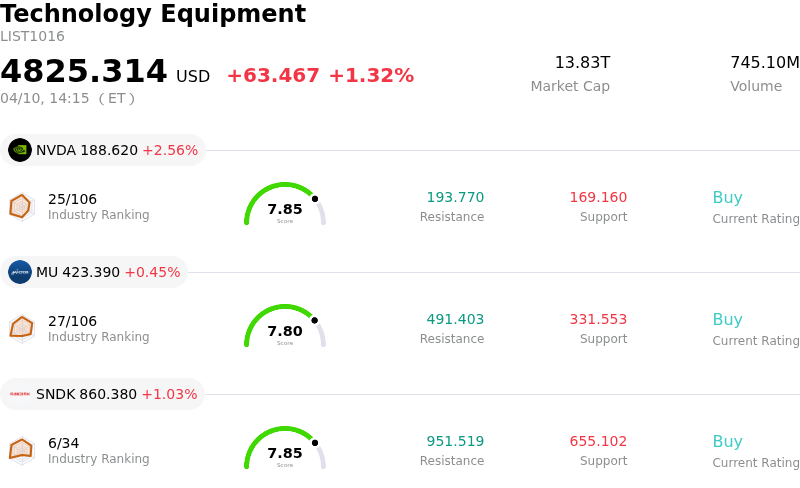

Lam Research Corp Stock (LRCX) Moved Up by 3.10% on Apr 10: A Full Analysis

Lam Research Corp (LRCX) moved up by 3.10%. The Technology Equipment sector is up by 1.32%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.56%; Micron Technology Inc (MU) up 0.45%; SanDisk Corporation (SNDK) up 1.03%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research (LRCX) experienced an upward price movement, largely fueled by a robust outlook for the semiconductor equipment industry and increasing demand tied to artificial intelligence (AI) advancements. The broader semiconductor manufacturing equipment market saw substantial growth in 2025, with projections indicating continued expansion in 2026, driven by investments in advanced logic, memory, and AI-related capacity. This industry upcycle, especially due to AI demand, is contributing to a positive environment for companies like Lam Research.

The company's recent financial performance has further bolstered investor confidence. Lam Research reported fiscal Q2 2026 earnings that surpassed analyst expectations for both revenue and earnings per share. Furthermore, management issued optimistic guidance for Q3 2026, forecasting continued strong revenue and EPS. This strong financial data, coupled with numerous analyst upgrades and positive reiterations of "Buy" or "Outperform" ratings and raised price targets, has contributed to the stock's positive momentum. The company also recently paid a quarterly dividend.

Despite the overall positive trend, significant intraday volatility suggests underlying market concerns. Proposed U.S. legislation aiming to tighten export controls on semiconductor manufacturing equipment to China presents a notable geopolitical risk for Lam Research, as China has been a significant market for the company. Valuation concerns have also emerged, with some analyses suggesting the stock may be overvalued relative to its intrinsic value. Additionally, projections for modest gross margin compression due to factors like tariff pressures and shifts in customer mix introduce a degree of uncertainty. Reports of insider selling also contribute to a mixed market sentiment.

The upcoming fiscal third-quarter 2026 earnings call, scheduled for April 22, is a key event that will test the sustainability of current AI-driven momentum and margins. Investors will be closely monitoring management commentary on these factors, particularly in light of ongoing macroeconomic and geopolitical headwinds, which are amplifying market swings for technology stocks.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [-0.05], indicating a neutral signal. The RSI at 65.40 suggests neutral condition and the Williams %R at -0.40 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $274.91, a high of $360.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Increased margin risks and supply chain vulnerability due to dependence on helium for tool production, as cited in a recent downgrade by Erste Group.

- Analyst downgrades, including from Zacks on April 10, 2026, reflect concerns about the stock's stretched valuation and limited near-term upside.

- Significant insider selling by multiple executives has been reported, potentially signaling negative sentiment to the market.

- High revenue exposure to the China market (35% of revenues) presents ongoing geopolitical and regulatory risks.

Recommended Articles