Applied Materials Inc Stock (AMAT) Moved Up by 3.15% on Mar 24: A Full Analysis

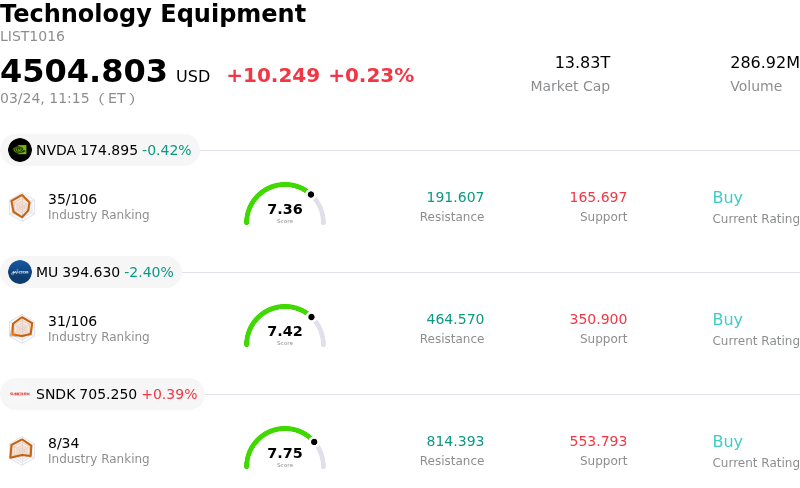

Applied Materials Inc (AMAT) moved up by 3.15%. The Technology Equipment sector is up by 0.23%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.42%; Micron Technology Inc (MU) down 2.40%; SanDisk Corporation (SNDK) up 0.39%.

What is driving Applied Materials Inc (AMAT)’s stock price up today?

Applied Materials' stock experienced significant positive movement and intraday volatility on March 24, 2026, primarily driven by a combination of favorable financial indicators, strong analyst sentiment, and strategic corporate developments within a robust industry landscape.

The company's financial health remains a key driver, with recent reports indicating better-than-expected revenue and earnings per share. Applied Materials has consistently surpassed consensus EPS estimates over the past four quarters, and its gross margin for Q1 FY26 showed an improvement year-over-year. Management has provided an optimistic outlook, projecting the semiconductor equipment business to achieve substantial growth in calendar year 2026, fueled by accelerating demand for artificial intelligence processors.

Analyst forecasts reflect this positive sentiment, with Wall Street maintaining a "Strong Buy" consensus rating and several firms reiterating or upgrading their ratings and increasing price targets. This reflects confidence in the company's exposure to rising spending in foundries and DRAM, as well as the anticipated multi-year earnings tailwind from AI-related capital expenditures.

Several major events further bolstered investor confidence. Applied Materials was added to the S&P 100 index on March 23, 2026, an event that typically generates incremental buying from passive index funds. The company's board also approved a notable increase in its quarterly cash dividend, marking nine consecutive years of dividend growth and signaling strong financial stability and a commitment to returning capital to shareholders. Furthermore, recent strategic partnerships with Micron Technology and SK Hynix, announced earlier in March, to develop next-generation memory solutions for AI systems, highlight the company's innovation and leadership in critical semiconductor technologies.

These company-specific strengths are amplified by a positive industry outlook. The semiconductor equipment market is experiencing a significant growth phase, driven by increasing global demand for advanced AI chips, 5G applications, and cutting-edge electronics. Industry forecasts project record sales for manufacturing equipment, with investments in leading-edge logic, high-bandwidth memory (HBM), and advanced packaging technologies providing strong tailwinds for Applied Materials.

Technical Analysis of Applied Materials Inc (AMAT)

Technically, Applied Materials Inc (AMAT) shows a MACD (12,26,9) value of [4.08], indicating a neutral signal. The RSI at 56.55 suggests neutral condition and the Williams %R at -21.64 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Applied Materials Inc (AMAT)

Applied Materials Inc (AMAT) is in the Technology Equipment industry. Its latest annual revenue is $28.37B, ranking 10 in the industry. The net profit is $7.00B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $407.73, a high of $470.00, and a low of $275.00.

More details about Applied Materials Inc (AMAT)

Company Specific Risks:

- Applied Materials faces intensifying competition in China, particularly in its Physical Vapor Deposition (PVD) and Sputtering/PCVD segments, leading to market share erosion by domestic suppliers like Naura and AMEC.

- The company incurred a significant $252.5 million settlement with the U.S. Department of Commerce in February 2026 for past non-compliance with export regulations concerning shipments to China, indicating ongoing regulatory compliance risks and potential for large financial penalties.

- Several analyst downgrades reflect concerns over an anticipated near-term deceleration in wafer fabrication equipment spending and the company's valuation, with growth in fiscal year 2026 expected to be heavily weighted towards the second half and current P/E ratios exceeding target valuations.