ASML Holding NV Stock (ASML) Moved Up by 4.60% on Mar 24: A Full Analysis

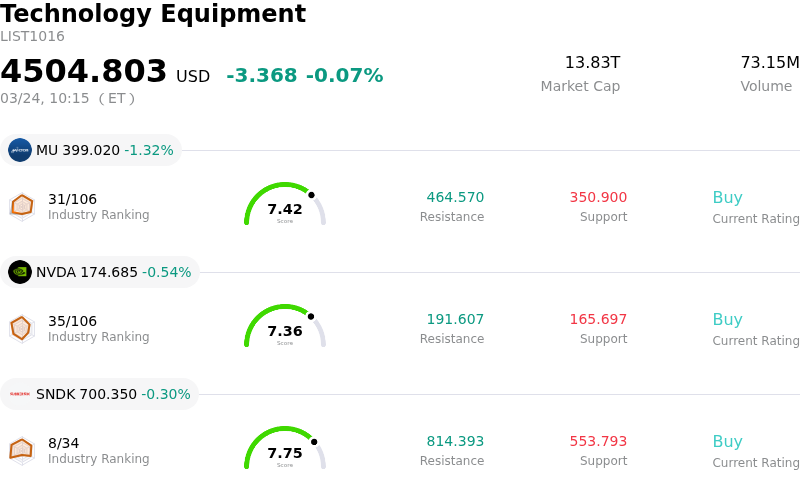

ASML Holding NV (ASML) moved up by 4.60%. The Technology Equipment sector is down by 0.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 1.32%; NVIDIA Corp (NVDA) down 0.54%; SanDisk Corporation (SNDK) down 0.30%.

What is driving ASML Holding NV (ASML)’s stock price up today?

ASML's stock experienced a significant upward movement on March 24, 2026, driven primarily by a substantial order from SK Hynix and a broadly positive sentiment from financial analysts regarding the company's pivotal role in the booming semiconductor industry.

A major catalyst for the positive performance was the announcement that SK Hynix Inc. plans to invest $7.9 billion in extreme ultraviolet (EUV) lithography tools from ASML, with orders extending through 2027. This record deal underscores the intense competition among chipmakers to secure advanced manufacturing equipment necessary for producing sophisticated semiconductors, particularly those powering artificial intelligence applications. The purchase validates ASML's projected path to 60 billion euro annual revenue by 2030 and highlights the shift in leading-edge memory demand from cyclical to structural. This development reinforces ASML's unique position as the sole provider of critical EUV technology essential for sub-10 nanometer processes, which are vital for AI chip acceleration.

In conjunction with this major event, analyst sentiment remained overwhelmingly positive. On March 24, 2026, BofA analysts raised ASML's price target, citing tight Foundry and DRAM supply and increasing EPS estimates for 2026-28. Similarly, Bernstein analysts also increased their price target and maintained an "Outperform" rating, suggesting that recent market dips presented a buying opportunity. The consensus from analysts around March 23-24, 2026, pointed to a "Buy" rating for ASML, with many highlighting its strong market performance and investor confidence.

The broader industry backdrop further supports ASML's robust performance. The semiconductor industry is in the midst of an AI-led recovery, with global chip sales projected to reach $975 billion in 2026 due to skyrocketing demand for AI. This AI boom is anticipated to sustain growth, potentially altering the historical cyclical trends of the semiconductor market. ASML's critical lithography technology is central to this growth, enabling the production of advanced chips for AI data centers and cloud computing. Additionally, ASML's ongoing share buyback program and increased dividend signal management's confidence in the company's financial health and commitment to shareholder returns. ASML had previously provided strong earnings guidance for 2026, with anticipated net sales between €34 billion and €39 billion, driven by increased EUV sales and growth in its installed base business.

Technical Analysis of ASML Holding NV (ASML)

Technically, ASML Holding NV (ASML) shows a MACD (12,26,9) value of [-4.74], indicating a sell signal. The RSI at 49.07 suggests neutral condition and the Williams %R at -28.85 suggests oversold condition. Please monitor closely.

Fundamental Analysis of ASML Holding NV (ASML)

ASML Holding NV (ASML) is in the Technology Equipment industry. Its latest annual revenue is $36.83B, ranking 7 in the industry. The net profit is $10.83B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1444.70, a high of $1911.00, and a low of $950.00.

More details about ASML Holding NV (ASML)

Company Specific Risks:

- Mizuho analysts downgraded ASML to 'Neutral' from 'Buy' with a reduced price target, citing a less favorable business outlook for 2026, including a forecasted 3% decline in sales and flat earnings per share.

- Morgan Stanley revised down ASML's 2026 revenue share estimate from China to 21% from 27%, anticipating an 18% year-on-year decline in line with management's guidance due to geopolitical tensions.

- Morgan Stanley warns of limited near-term upside for ASML in 2026, projecting that demand for its extreme ultraviolet (EUV) lithography machines will be heavily weighted towards the second half of the year.

- The company faces significant valuation risk and concentration risk, with a large portion of its revenue derived from a few top chipmakers, making it vulnerable to any reduction in their orders.