Today’s Market Recap: South Korea’s Semiconductor Strategy Boosts Chip Chain, Nvidia, Western Digital, Micron and Other Chip Stocks Collectively Strengthen

AI Podcast

On June 29, Eastern Time, U.S. equities rebounded, led by the Nasdaq’s 2.07% gain, as tech stocks recovered from recent corrections. The Dow reached a record 52,188.21, while the S&P 500 rose 1.18%. Semiconductor and AI-related shares drove growth amid renewed risk appetite. Geopolitical tensions in the Middle East stabilized, tempering oil volatility. Despite current momentum, investors remain cautious regarding upcoming U.S. jobs data and the sustainability of the AI capex cycle. Meanwhile, the yen hit 1986 lows due to persistent U.S.-Japan interest rate differentials, highlighting ongoing pressure from divergent central bank policies and potential carry trade shifts.

Tracking Market Trends

TradingKey - On June 29, Eastern Time, the US stock market rose across the board, supported by a rebound in tech stocks and a temporary cooling of tensions in the Middle East. AI and mega-cap tech stocks, which had previously been under continuous pressure, staged a corrective rally, driving the Nasdaq Composite to lead the three major indices. The Dow Jones Industrial Average closed above the 52,000-point mark for the first time, setting a new record closing high. Market risk appetite recovered somewhat, but investors remain focused on the implementation of the temporary US-Iran peace agreement, oil price volatility, and the US jobs data scheduled for release this week.

At the close, the Dow Jones Industrial Average rose 0.59% to 52,188.21 points; the Nasdaq Composite index climbed 2.07% to 25,820.14 points; and the S&P 500 index gained 1.18% to 7,440.44 points. Tech stocks became the main driver of the market's rebound, with AI and semiconductor-related shares that had previously undergone deep corrections attracting fresh buying. Tesla ( TSLA) surged over 8%, Alphabet ( GOOGL) rose nearly 5%, SpaceX ( SPCX) gained about 7%, indicating a recovery in market sentiment toward mega-cap tech and the AI infrastructure sector.

In terms of individual stocks and sectors, technology shares led the market's rebound, with chip stocks performing particularly well. The Philadelphia Semiconductor Index closed up 3.83%, while Marvell Technology ( MRVL ), AMD ( AMD ), Nvidia ( NVDA) and Micron Technology ( MU) all recorded gains. Inflows returned to AI chips, advanced nodes, memory, and semiconductor equipment chains, indicating that investors are still betting on medium-to-long-term demand driven by AI infrastructure expansion after the recent sharp correction.

In commodity markets, oil prices rebounded against the backdrop of ongoing uncertainty in the Middle East. WTI ( USOIL) spot crude closed up 0.23% at $70.41/barrel, while Brent crude slipped 0.04% to $73.58/barrel. With shipping in the Strait of Hormuz gradually resuming and expectations of returning supply rising, oil prices remain in a clear downward trend for the month. In precious metals, the US dollar and Treasury yields stayed high, putting pressure on gold ( XAUUSD) causing the price of gold to fall about 1.8% on the day as safe-haven demand cooled compared to the previous period.

Market Headlines

The South Korean government officially unveiled a new round of semiconductor and AI industry development strategies, planning to advance three major "mega projects" in semiconductors, AI data centers, and robotics. Among these, Samsung announced an investment of 2,655 trillion won, while SK Hynix will invest 1,100 trillion won, focusing on expanding production capacity for AI semiconductors, HBM, high-end memory, and advanced packaging. The South Korean government will also provide supporting initiatives covering power, water, transportation, talent, and regional infrastructure to consolidate its leading position in the global memory chip market.

The US and Iran held talks in Qatar on Tuesday. Although interim peace arrangements between the US and Iran still face uncertainty, expectations that both sides would resume technical-level contacts in Qatar today have eased market concerns over a full-scale conflict escalation. The short-term rebound in oil prices reflects more of a recovery of the risk premium following geopolitical conflicts over the weekend, rather than a fundamental reversal in the supply and demand dynamics. As shipping in the Strait of Hormuz gradually recovers, the market is reassessing the pace at which global crude supply will return.

Mega-cap US tech stocks staged a rebound after a series of corrections. Leading tech giants, previously weighed down by AI capex return cycles, valuation pressures, and interest rate expectations, regained buying support, driving the Nasdaq to snap a five-day losing streak. However, market divisions over the AI trade have not disappeared; investors are still distinguishing between the "capex beneficiaries" and the "capex spenders" in the AI supply chain, suggesting that tech stocks could remain highly volatile in the near term.

In the foreign exchange market, the yen weakened further, briefly touching its lowest level since 1986. The market believes that the Federal Reserve is maintaining a relatively hawkish stance, while Japan's monetary policy normalization process remains constrained by economic and financial market conditions, leaving the US-Japan interest rate differential to continue pressuring the yen. The yen's weakness has also heightened focus in Asian markets on carry trades and shifts in capital flows.

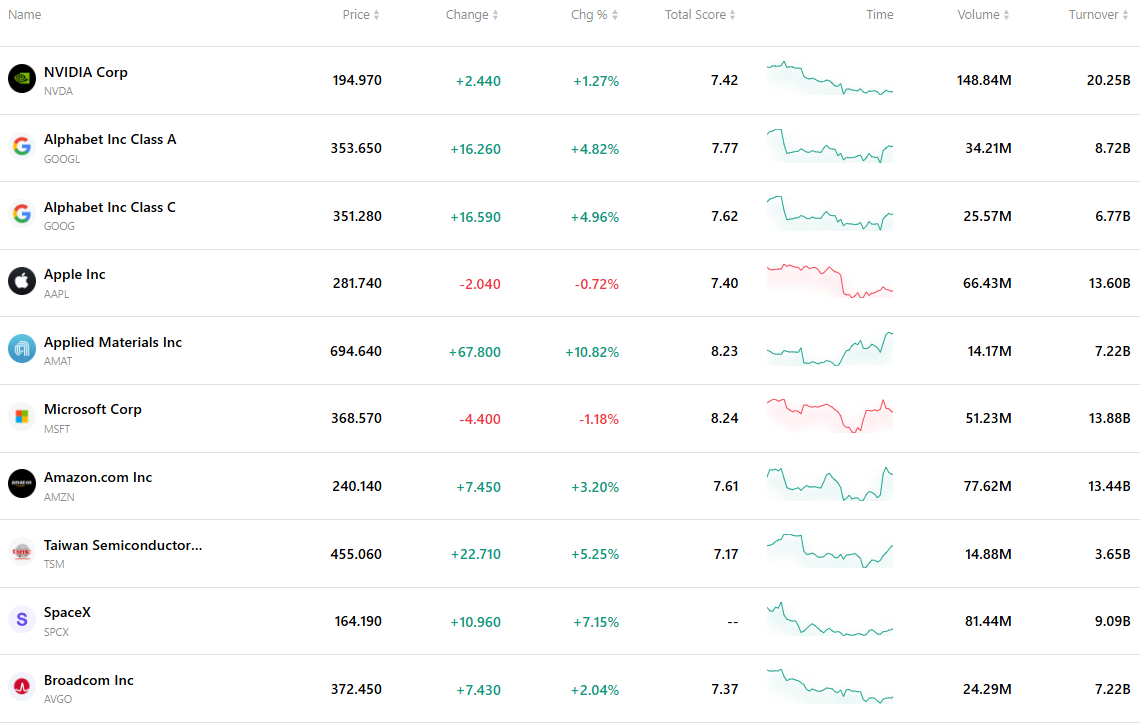

Top 10 most active stocks

The table below lists the ten most actively traded stocks in the current market. Supported by massive trading volumes and exceptional liquidity, these assets have become key benchmarks for tracking global market dynamics.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.