Google Earnings Preview: It’s a Buy on Strong Projected Cloud Business

AI Podcast

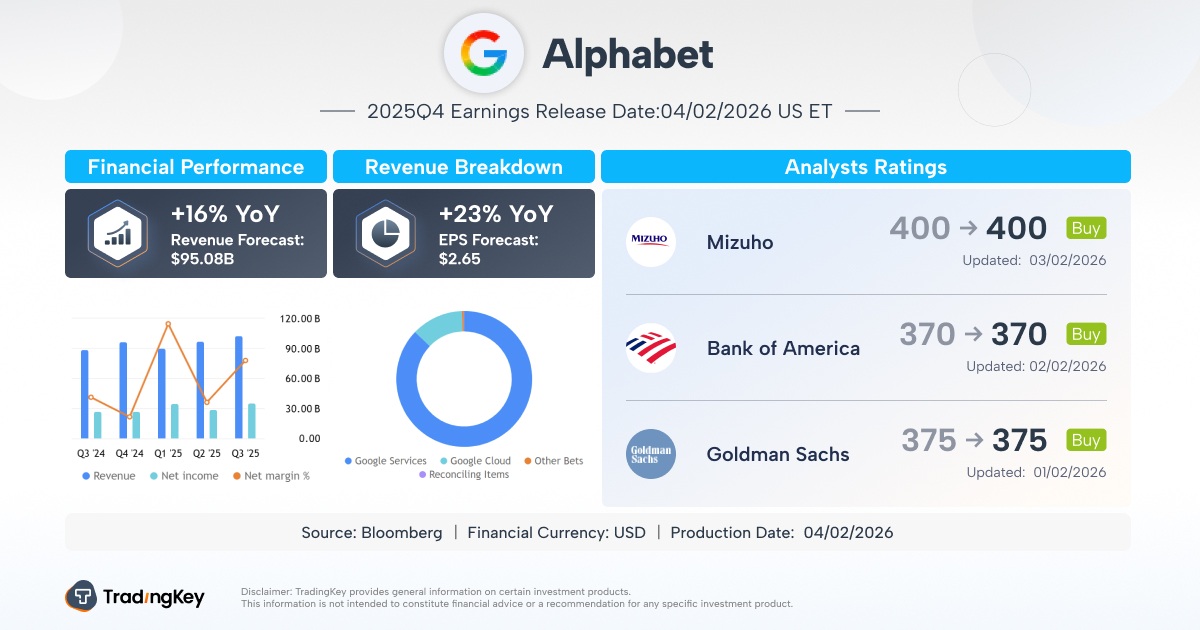

Google's Q4 2025 earnings are anticipated to be strong, with analysts projecting 16% revenue growth to $95.08 billion. Google Cloud is a key driver, expected to grow 35% year-over-year, supported by Gemini's adoption and strong backlog. The company's proprietary TPUs and "de-Nvidia-ization" strategy are also contributing positively to its IaaS business. While capital expenditures are rising, driven by AI infrastructure investment, continued cloud revenue growth and effective cost management are expected to offset these costs, maintaining Google's valuation. The advertising business, bolstered by AI search, is also showing robust growth prospects.

TradingKey - This week, market focus shifts to Google (GOOG) (GOOGL) the Q4 2025 earnings report. Based on the performance of the options market, most investors are confident in this quarter's results: as of January 29, Google Class A options trading was active, with a total daily volume of 4.07 million contracts. Call options accounted for nearly 70% of the total volume, and some traders even bet that Google would rise to $360 post-earnings.

For the full year of 2025, Google's stock price saw a cumulative increase of over 65%, becoming one of the best-performing companies among the MAG 7.

Google will release its Q4 earnings report after the market close on February 4, ET. Bloomberg analysts expect Q4 revenue to grow 16% year-over-year to $95.08 billion, adjusted net income to rise 19% to $38.55 billion, and GAAP earnings per share to increase 23% to $2.65.

Google’s Second Engine: Cloud Revenue Poised for 35% Jump

Google Cloud is Google's fastest-growing segment and is regarded as the company's second-largest growth engine. Cloud revenue in Q3 grew 34% year-over-year to $15.16 billion; as of the end of the third quarter, the backlog increased 82% year-over-year to $155 billion, a net increase of $47 billion compared to Q2. Due to the surge in backlog, the market expects Google's cloud business to maintain revenue growth of over 30% for some time.

Bloomberg data shows that the market expects Google Cloud's Q4 revenue to grow 35.4% year-over-year. Citi (C) analysts believe the growth momentum primarily stems from the large language model Gemini, TPUs, and the cloud business backlog from Q3.

Citing internal Google data, The Information noted that the volume of Gemini API calls via Google Cloud has grown rapidly, from approximately 35 billion when Gemini 2.5 was released last March to about 85 billion by August. Currently, Gemini enterprise subscribers have grown to 8 million. Furthermore, compared to the early Gemini 1.0 and 1.5 versions which had negative margins, subsequent versions have achieved positive margins.

Regarding in-house chips, Google reached a chip sales and compute leasing contract with Anthropic last October valued at over $50 billion, providing 1 million self-developed TPUs to Anthropic. A portion of these will be supplied directly to Anthropic to meet the computing power demands of its large language models (Claude 4 or Claude 5). For Google, the development of in-house TPUs helps reduce the unit cost of computing power. The fact that these TPUs are now being offered externally also demonstrates that its "de-Nvidiaization" (NVDA) strategy has become relatively mature, and Google's IaaS (Infrastructure as a Service) business is expected to enter a golden age.

Additionally, some analysts believe that the improvement in cloud margins is also a significant growth driver. The margin reached 20.7% in Q2 2025 compared to just 11.3% in the same period last year, and exceeded 23.7% in Q3 2025 compared to only 17.1% last year. Although Google Cloud's margins remain lower than those of its peers—Amazon (AMZN) AWS cloud services saw a Q3 margin of 34.6%, while Microsoft (MSFT) Azure and other cloud services reached a margin of 43% in Q1 of fiscal year 2026, yet Google has been making steady improvements every quarter.

Hyperscalers Double Down: CapEx Forecasts Move Higher

Currently, Wall Street generally expects 2026 to be a year when tech giants significantly ramp up capital expenditures. Morgan Stanley predicts that the total CapEx of the four major U.S. cloud service providers (namely Amazon, Google, Meta (META) and Microsoft) will rise to $454 billion in 2026, a 26% year-on-year increase; cloud CapEx as a percentage of revenue will also reach a record high, exceeding 20% in 2026. Currently, TSMC (TSM) has taken the lead in announcing an upward revision to its 2026 capital expenditures, and other giants are expected to follow suit.

Google is no exception. Last October, Google raised its 2025 CapEx guidance to $91 billion-$93 billion. Management has indicated that capital expenditures will increase further in 2026 compared to 2025, with full-year spending expected at approximately $135 billion, though it could reach as high as $150 billion given the growth momentum of Google Cloud and its TPU business.

Analysts believe this is because Google, as a hyperscale cloud provider, derives its growth primarily from massive investment in computing power, and the current investment cycle has not yet concluded. The growth of Google Cloud has been accompanied by ever-increasing capital expenditures.

Currently, the market views the upward revision in Google's CapEx as a positive signal, implying that Google will continue to invest heavily in infrastructure. However, this does not mean the market will be entirely forgiving. If spending becomes excessive and Google Cloud's revenue growth fails to fill the void, or if the progress of the next-generation Gemini model falls short of market expectations and fails to justify its costs, Google's valuation could face a sharp correction.

Resilient Ad Business: Search AI in the Spotlight

Currently, Google has launched AI search in more than 200 countries and regions, supporting over 40 languages with 2 billion monthly active users. Google stated that AI search can increase search volume by 10% while enhancing user stickiness. This not only increases Google's ad inventory but also aids in user retention, playing a pivotal role in search advertising.

Wall Street expects search advertising revenue to grow by 13.7% year-over-year in Q4. Citi analysts believe that as new features like UCP (Unified Commerce Platform) and Direct Offers go live, supported by Google's over 50 billion product listings and core verticals such as Agentic Travel, the agentic commerce sector will also exhibit new growth momentum.

The market is anticipating that Google's AI search will bring greater advertising efficiency, allowing Google to maintain high-frequency services at a lower unit computing cost than its competitors, thus more efficiently converting revenue growth into profit growth.

In terms of YouTube advertising, YouTube now has more than 2.7 billion global users. With the steady growth of YouTube TV and subscription services, Wall Street projects that YouTube advertising revenue will grow by 13.5% year-over-year in Q4.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.