Taiwan Semiconductor Manufacturing Co Ltd Stock (TSM) Moved Up by 4.83% on Jul 6: What Signal Does It Send?

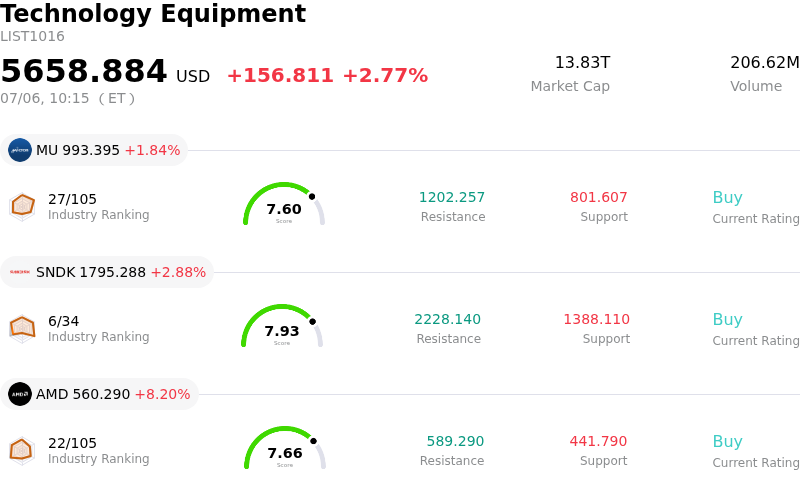

Taiwan Semiconductor Manufacturing Co Ltd (TSM) moved up by 4.83%. The Technology Equipment sector is up by 2.77%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 1.84%; SanDisk Corporation (SNDK) up 2.88%; Advanced Micro Devices Inc (AMD) up 8.20%.

What is driving Taiwan Semiconductor Manufacturing Co Ltd (TSM)’s stock price up today?

Taiwan Semiconductor Manufacturing Company (TSMC) experienced a notable upward movement, characterized by significant intraday volatility, as institutional momentum and strategic market updates injected fresh optimism into the semiconductor sector.

A primary driver of this upward momentum is a highly positive pre-earnings catalyst watch initiated by Citigroup. Analysts at the firm predicted that TSMC is poised to raise its full-year 2026 revenue growth projections during its upcoming quarterly earnings call scheduled for mid-July. This optimism is underpinned by the company's unrivaled global scale, which holds approximately 70 percent of the dedicated foundry market share. This dominant market positioning is anticipated to shield the company from pricing pressures, secure deep customer loyalty, and support highly stable gross margins despite growing competition in the semiconductor foundry space.

Secular demand for advanced artificial intelligence (AI) chips and high-performance computing infrastructure continues to serve as a powerful tailwind. Market leaders like Nvidia, Apple, and AMD remain heavily reliant on TSMC's sub-3-nanometer advanced nodes and cutting-edge packaging technologies. Additionally, structural tailwinds, including expectations of margin expansion from potential price hikes on advanced manufacturing nodes and increased manufacturing tax credits for U.S. capacity expansion, have reinforced the long-term bullish thesis among institutional investors.

However, the significant intraday volatility reflects a tug-of-war between long-term fundamental strength and near-term market technicals. Leading up to this movement, the stock had experienced a period of fading short-term momentum, trading below key short-term moving averages and facing profit-taking pressures. Concerns over high capital expenditures and a recent exclusion from Goldman Sachs' conviction list had briefly dampened near-term sentiment. Nevertheless, the combination of strong analyst upgrades, anticipated guidance hikes, and resilient AI-driven demand ultimately allowed buyers to reclaim control, driving the sharp upward recovery during the session.

Technical Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Technically, Taiwan Semiconductor Manufacturing Co Ltd (TSM) shows a MACD (12,26,9) value of -1.794, indicating a neutral signal. The RSI at 50.113 suggests neutral condition and the Williams %R at 72.568 suggests sell condition. Please monitor closely.

Fundamental Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Taiwan Semiconductor Manufacturing Co Ltd (TSM) is in the Technology Equipment industry. Its latest annual revenue is $122.22B, ranking 2 in the industry. The net profit is $55.12B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $478.87, a high of $625.00, and a low of $351.00.

More details about Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Company Specific Risks:

- Aggressive Capex and Margin Compression Risks: TSMC's massive projected 2026 capital expenditures of $52 billion to $56 billion to scale advanced sub-3nm nodes expose the company to significant fixed-cost underutilization and potential gross margin erosion if global AI-related hardware demand experiences a cyclical cooling period.

- Q2 Revenue Growth Underperformance: Although TSMC reported double-digit sales expansion, its combined April and May sales growth of 24% year-over-year fell short of Wall Street's elevated quarterly expectations of 35%, raising the risk of a near-term revenue miss and fueling investor caution ahead of the company's July 16, 2026, earnings conference.

- Downstream Pricing Pressures and Demand Pullbacks: Rising silicon and packaging costs have forced TSMC to enact broad price hikes across its manufacturing nodes. Institutional analysts are concerned that these hikes will force downstream hardware partners, such as Apple, to raise retail prices, potentially dampening consumer electronics demand and leading to a pullback in wafer order volumes.

- Valuation Premium and Valuation Stretch: The stock's trailing twelve months (TTM) P/E ratio stands at over 32.8x, which is significantly higher than its 5-year median P/E of 22.78x, rendering the company overvalued based on historical performance and removing any margin of safety for investors.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.