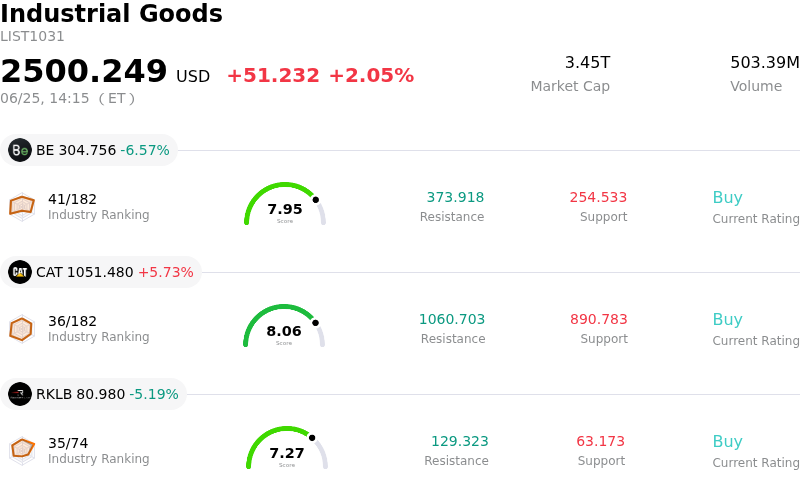

Deere & Co Stock (DE) Moved Up by 3.55% on Jun 25: Drivers Behind the Movement

Deere & Co (DE) moved up by 3.55%. The Industrial Goods sector is up by 2.05%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Bloom Energy Corp (BE) down 6.57%; Caterpillar Inc (CAT) up 5.73%; Rocket Lab USA Inc (RKLB) down 5.12%.

What is driving Deere & Co (DE)’s stock price up today?

The significant upward move and intraday volatility in Deere and Company shares on the current trading day are primarily driven by a powerful mix of industry-wide momentum, upgraded company guidance, and supportive policy developments.

A major near-term catalyst is a sector-wide rally across the heavy machinery and industrial equipment space. Positive investor sentiment was triggered by strong gains in key peer Caterpillar, which experienced a notable upward re-rating due to robust backlogs and exposure to high-growth segments like data-center power. This industry-wide lift helped pull Deere higher, as institutional investors increased exposure to high-quality industrial names that show resilient demand and strong pricing power.

Underpinning this momentum is Deere's successful pivot from a traditional, cyclical hardware manufacturer into a high-margin, software-integrated agricultural technology leader. The company recently surprised the market by raising its full-year net income guidance, driven by a faster-than-anticipated adoption of its advanced See and Spray autonomous technology suites. This technological pivot has expanded Deere's valuation multiples, allowing it to maintain strong profit margins despite cyclical pressures in the broader agricultural market.

Further supporting the stock is Deere's robust capital allocation strategy. The board's authorization of a massive new share repurchase program has bolstered investor confidence. This initiative reassures shareholders of management's long-term cash flow outlook and dedication to returning capital to investors.

Finally, macroeconomic policy changes have provided critical relief to Deere's supply chain and production margins. The recent lowering of metal import tariffs on farm and construction equipment under federal trade adjustments has significantly reduced input cost pressures. By mitigating the heavy tariff liabilities that previously threatened margins, these adjustments have allowed Deere to protect its profitability, further fueling the stock’s upward trajectory on the day.

Technical Analysis of Deere & Co (DE)

Technically, Deere & Co (DE) shows a MACD (12,26,9) value of 6.834, indicating a buy signal. The RSI at 61.527 suggests neutral condition and the Williams %R at 21.700 suggests buy condition. Please monitor closely.

Fundamental Analysis of Deere & Co (DE)

Deere & Co (DE) is in the Industrial Goods industry. Its latest annual revenue is $45.67B, ranking 2 in the industry. The net profit is $5.03B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $634.90, a high of $759.00, and a low of $471.00.

More details about Deere & Co (DE)

Company Specific Risks:

- Persistent Margin Compression from Direct Tariff Exposures: Despite recent policy adjustments, Deere faces a massive direct tariff exposure of approximately $1.2 billion for fiscal 2026. This translates to an immediate 3% equipment operations margin headwind. Even after accounting for one-time refunds, the company is absorbing roughly $900 million in annual net tariff costs rather than passing them on to customers, severely restricting structural gross margin expansion.

- Prolonged Cyclical Downturn in Large Agriculture Segment: Deere's highest-margin segment, Large Production & Precision Agriculture, continues to struggle with a severe cyclical downcycle, with regional equipment sales in the U.S. and Canada projected to slide 15% to 20% in fiscal 2026. This demand contraction is exacerbated by depressed global crop prices, rising farm debt levels, and a 15% decline in farmer net incomes, forcing customers to defer capital equipment upgrades.

- Erosion of Aftermarket Service Revenues from Right-to-Repair Mandates: Following the preliminary approval of a $99 million antitrust class action settlement, Deere is legally obligated to open its proprietary diagnostic software ecosystem to independent repair shops and equipment owners for at least a decade. This legally binding "right-to-repair" commitment shifts power away from Deere’s exclusive dealer network, directly threatening its highly lucrative, high-margin captive parts and service revenues.

- Stretched Valuation Premium Vulnerable to Macro Headwinds: Trading at a premium Forward P/E multiple of 27x to 32.5x (compared to an industry average of approximately 21x), the stock aggressively discounts a rapid "next-cycle" peak recovery. This elevated valuation leaves the stock highly vulnerable to sudden downside volatility if the broader macroeconomic recovery in the agricultural sector takes longer to materialize than institutional models currently project.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.