Micron Q3 Data Center Revenue Grows Over Sevenfold YoY; Shares Jump Over 14% Post-Market, Memory Supply Shortage to Last Beyond 2027

AI Podcast

Micron’s fiscal Q3 2026 results exceeded expectations, with revenue surging 345.72% year-over-year to $41.46 billion and EPS reaching $24.67. Driven by explosive AI-related demand, the data center segment grew sevenfold. Gross margins expanded to 84.9%, reflecting strong pricing power. Micron projects Q4 revenue of $50 billion, signaling sustained momentum. Management anticipates memory supply shortages to persist beyond 2027 as capacity ramp-ups struggle to match demand. With 16 long-term customer agreements secured, Micron remains a primary beneficiary of the AI infrastructure cycle, with chip prices expected to remain elevated due to a structural supply-demand mismatch.

TradingKey - On June 24, Eastern Time, Micron (MU) released its fiscal third-quarter 2026 financial results during US after-hours trading, sending its stock price up over 13% at one point. As of press time, the stock remained up 13.96% at $1,194.19.

[Source: Google Finance]

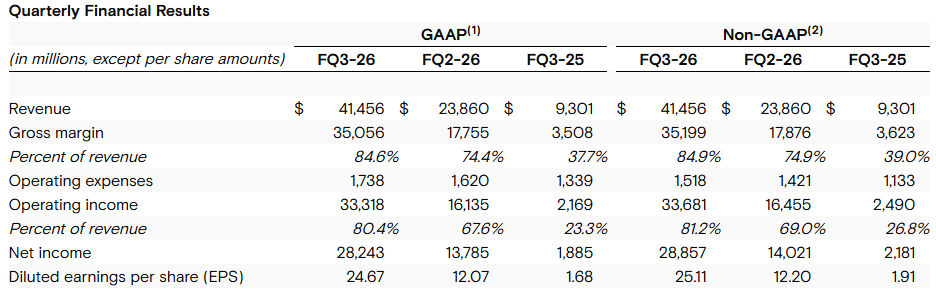

During the period, Micron Technology's revenue grew 345.72% year-over-year to $41.46 billion and 73.75% quarter-on-quarter, significantly beating market expectations of $35.84 billion. Although growth across all four business units surpassed expectations, the data center business recorded the most rapid growth, with its revenue increasing sevenfold year-over-year. Micron Technology stated in a report that besides its memory business, revenue from its data center SSD business also exceeded $5 billion.

Looking at the specific business segments, cloud storage revenue reached $13.769 billion, up 306.65% year-over-year, while its gross margin expanded significantly to 83% from 58% in the same period last year and 74% in the previous quarter.

Data center revenue stood at $11.524 billion, up 653.20% year-over-year, with the gross margin surging to 87% from 38% in the prior-year period.

Revenue from the mobile and client business was $11.524 billion, up 253.95% year-over-year, with the gross margin also surging to 87%.

In terms of profitability, under GAAP, Micron Technology's third-quarter net income was $28.24 billion, up 1,398.30% year-over-year. This translates to diluted earnings per share (EPS) of $24.67, a significant increase from $1.68 in the same period last year, and nearly doubling quarter-on-quarter.

Micron's gross margin was equally impressive (profit after deducting cost of goods sold), jumping to 84.9% from 74.9% in the previous quarter and 39% in the same period last year, beating analysts' expectations.

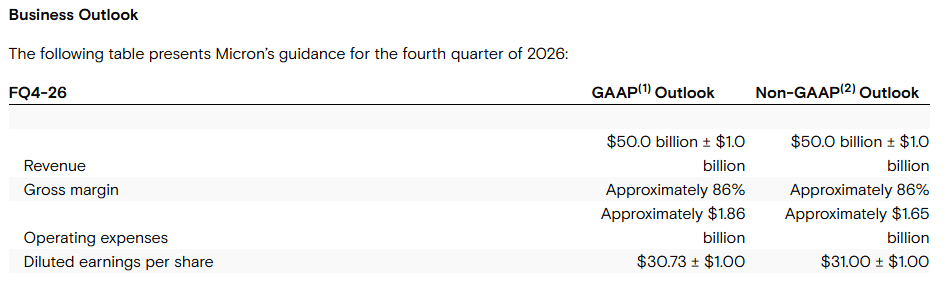

Regarding guidance, Micron expects fourth-quarter revenue to be $50 billion (plus or minus $1 billion), up from $11.3 billion in the same period last year and exceeding the $43.58 billion recently projected by LSEG. The gross margin is expected to be 86%, with adjusted EPS projected at $30.73 (plus or minus $1).

Micron Technology stated that, driven by AI-powered demand, tight memory supply is expected to persist beyond 2027. The company also noted that it has signed 16 long-term agreements with customers including data center operators and automakers, locking in sales for the next three to five years.

The wave of AI computing power buildout continues to propagate upstream along the industry chain, making the three global memory giants—Micron, Samsung, and SK Hynix—the most direct beneficiaries. Concentrated investments in data center computing power are driving demand across two major memory categories: the large-scale procurement of general-purpose memory, and the explosive growth of AI-dedicated High Bandwidth Memory (HBM).

Constrained by capacity ramp-up cycles, leading manufacturers cannot fully satisfy the surging demand in the short term, causing supply shortages to spread from data centers to downstream sectors such as PCs, smartphones, and automotive. Although major players are actively expanding capacity, the industry's supply-demand mismatch is unlikely to be resolved quickly, and memory chip prices are expected to remain elevated for some time.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.