Lam Research Corp Stock (LRCX) Moved Up by 4.78% on Jun 25: A Full Analysis

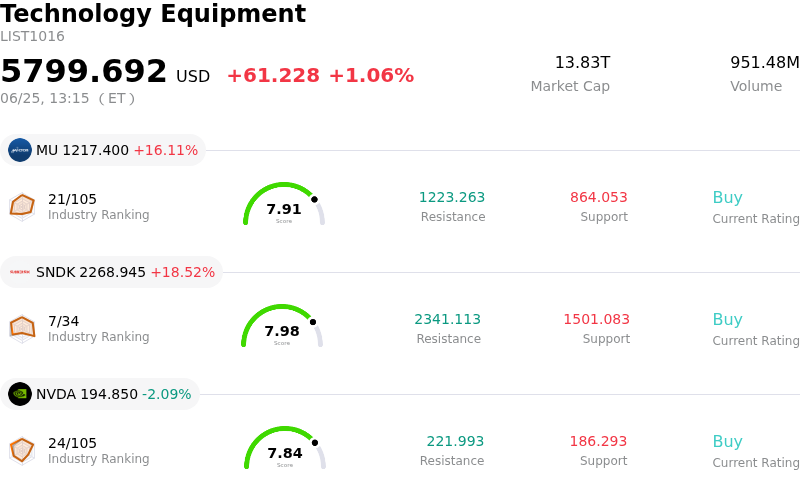

Lam Research Corp (LRCX) moved up by 4.78%. The Technology Equipment sector is up by 1.06%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 16.11%; SanDisk Corporation (SNDK) up 18.52%; NVIDIA Corp (NVDA) down 2.09%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research experienced a notable upward move accompanied by pronounced intraday volatility, driven primarily by a powerful sector-wide rally in semiconductor stocks and reinforced by bullish analyst upgrades.

The primary catalyst for the surge was the blockbuster earnings report and exceptionally strong forward guidance from memory chipmaker Micron Technology. Micron's blowout results reignited investor confidence in the durability of artificial intelligence spending and highlighted a persistent supply tightness in high-bandwidth memory and advanced storage. Because Lam Research is a premier provider of wafer fabrication, etching, and deposition equipment essential for advanced DRAM and 3D NAND manufacturing, the positive outlook for memory capital expenditures directly bolstered optimism for its order book. Additional positive forecasts from other industry giants, such as Qualcomm's projected AI-driven revenue expansion, further solidified the market's belief in sustained semiconductor demand, snapping a recent multi-day losing streak for technology equities.

Furthermore, recent highly favorable analyst adjustments have provided strong tailwinds for the company. Major financial institutions, including Bank of America and Citigroup, significantly raised their price targets for the stock. Analysts highlighted surging NAND equipment demand, accelerated by rising AI workloads and next-generation chip architectures like gate-all-around, as key drivers that could push the equipment manufacturer's valuation higher.

Despite the initial surge and positive opening gap, the stock faced significant intraday volatility and gave back a portion of its early gains. This pullback reflects an ongoing debate over the company's valuation, which has expanded substantially following a massive year-to-date rally. Investors remain sensitive to profit-taking pressure at these elevated multiples, especially when weighed against risks such as potential cyclical cooling in certain mature-logic nodes and persistent export control concerns regarding China. Additionally, recent insider trading disclosures, including pre-arranged stock sales by corporate executives, have introduced minor headwind anxieties, prompting short-term traders to lock in profits during the sharp morning spike. Nonetheless, the underlying demand for AI infrastructure continues to provide a robust fundamental backstop for the company.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 3.304, indicating a buy signal. The RSI at 59.421 suggests neutral condition and the Williams %R at 32.660 suggests buy condition. Please monitor closely.

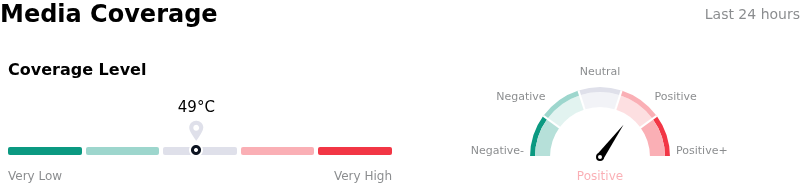

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $337.58, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- SK Hynix Production Pivot and Memory Capex Slowdown: SK Hynix's announcement on June 23, 2026, to slow advanced AI chip production (including high-bandwidth memory and advanced NAND) and redirect capacity toward commodity DRAM directly threatens demand. Because commodity production requires fewer process steps, this shift reduces equipment intensity per wafer and compresses the near-term order outlook for Lam's specialized etch and deposition tools.

- China Revenue Concentration and Tightening Export Controls: With China accounting for 34% to 35% of total revenue, Lam remains highly vulnerable to geopolitical friction. Ongoing US export restrictions limiting advanced semiconductor equipment sales to leading Chinese chipmakers, paired with guided sequential declines in China revenue, present a material threat to Lam's addressable market.

- Drastic Deceleration in System Shipment Growth: Analysts have raised structural concerns regarding a steep projected decline in system shipment growth, which is expected to drop to just 3% in 2026 from 82% in 2025. This deceleration is driven by cyclical cooling in 3D NAND and Chinese mature-logic nodes, and is further reflected in falling customer down payments signaling a pullback in memory capital commitments.

- Extreme Valuation Stretch and High-Level Insider Divestments: Following a year-to-date rally of over 115% that pushed the forward P/E ratio over 47x, the stock has exhibited severe vulnerability to profit-taking and multiple compression. This vulnerability is compounded by recent SEC Form 4 filings disclosing that Director Eric Brandt divested 54,500 shares in open-market transactions totaling over $19.1 million, triggering investor anxieties regarding a near-term valuation peak.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.