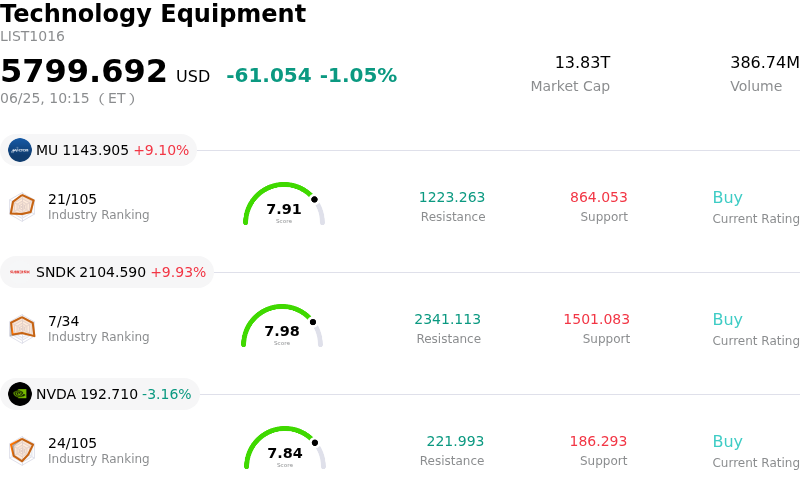

Micron Technology Inc Stock (MU) Moved Up by 9.10% on Jun 25: A Full Analysis

Micron Technology Inc (MU) moved up by 9.10%. The Technology Equipment sector is down by 1.05%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 9.10%; SanDisk Corporation (SNDK) up 9.93%; NVIDIA Corp (NVDA) down 3.05%.

What is driving Micron Technology Inc (MU)’s stock price up today?

Micron Technology has experienced a strong upward surge in intraday trading, reversing recent sector-wide volatility. The primary catalyst is the company's exceptional third-quarter fiscal 2026 earnings report and an extraordinarily robust outlook, which have rejuvenated investor confidence across the entire semiconductor sector. The blowout results demonstrate that the artificial intelligence hardware buildout remains in a rapid expansion phase, with high-bandwidth memory and advanced DRAM demand intensifying faster than Wall Street had modeled.

During the third quarter, Micron generated revenue of $41.46 billion, representing a near-fourfold increase compared to the same period last year and significantly beating consensus expectations. Adjusted earnings per share reached $25.11, comfortably ahead of the anticipated $20.49. The company's performance was bolstered by a soaring gross margin of 84.9%, reflecting immense pricing power in a structurally undersupplied memory market. This stellar profitability illustrates the massive operating leverage Micron possesses as fixed manufacturing costs remain steady while average selling prices climb.

Investor enthusiasm was further amplified by forward guidance that shattered previous estimates. For the fourth fiscal quarter, Micron expects revenue of approximately $50 billion, far exceeding the prior consensus of $42.9 billion, and adjusted earnings per share of $31.00. Crucially, the company's gross margin is guided to expand to roughly 86%. Beyond the immediate numbers, Micron announced that it has entered into transformational Strategic Customer Agreements. Under these agreements, Micron has secured 16 take-or-pay contracts, locking in $22 billion in upfront cash deposits and guaranteeing a minimum of $100 billion in revenue over the next five years. This structural change greatly enhances long-term financial predictability and mitigates cyclical memory risks.

Major Wall Street brokerages have responded to these disclosures by aggressively raising their price targets. Analysts have highlighted that the massive demand for AI-optimized memory is creating a prolonged upcycle that is likely to extend for several more quarters. By proving that hyperscaler demand is accelerating and backed by locked-in, long-term customer commitments, Micron’s earnings have successfully calmed fears of an imminent slowdown in artificial intelligence capital spending. This has triggered a broad wave of institutional buying, driving the stock higher despite the prevailing market volatility.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of -7.876, indicating a neutral signal. The RSI at 56.813 suggests neutral condition and the Williams %R at 45.948 suggests neutral condition. Please monitor closely.

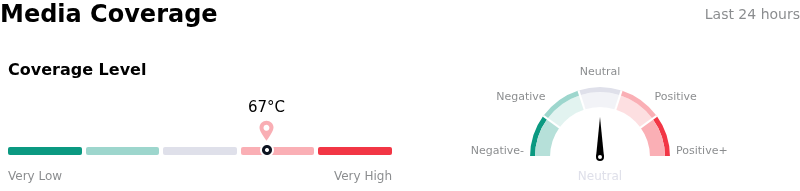

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 67, indicating a high level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1114.85, a high of $1750.00, and a low of $190.00.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Aggressive Capital Expenditure Demands: Micron raised its fiscal year 2026 net capital expenditure guidance to $27 billion (including a sequential Q4 capex hike to $10 billion) to expand advanced DRAM and HBM facilities. This record-level investment creates heavy operational leverage and severe downside risk to margins if AI infrastructure demand or data-center buildouts slow down sooner than expected.

- Intensifying AI Memory Competition: Despite a strong Q3 performance, Micron faces fierce competition from Samsung and SK Hynix, both of which are aggressively scaling up next-generation HBM production (e.g., Samsung delivering HBM4E samples and SK Hynix advancing its own capacity expansion and thermal management solutions). This threatens to erode Micron's pricing power and could shift the market back into oversupply by 2027.

- Extreme Valuation Volatility and "Priced for Perfection" Baseline: The sharp 13.2% stock selloff on June 23, 2026, ahead of earnings underscores Micron's high sensitivity to macroeconomic sentiment and rival stock corrections. With its newly established Q4 revenue baseline of $50 billion, analysts warn that the stock's massive run-up exposes it to technical exhaustion and "sell-the-news" downside if future quarterly results deliver anything less than exceptional beats.

- Ongoing Patent and Product Litigation: Noted alongside its June 24, 2026, earnings update, Micron continues to navigate extensive patent infringement and legal disputes covering a major portion of its high-volume DRAM and NAND products, posing a persistent threat of financial liabilities, cost escalation, or operational disruptions.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.