Taiwan Semiconductor Manufacturing Co Ltd Stock (TSM) Opened Up by 6.86% on Jun 21: A Full Analysis

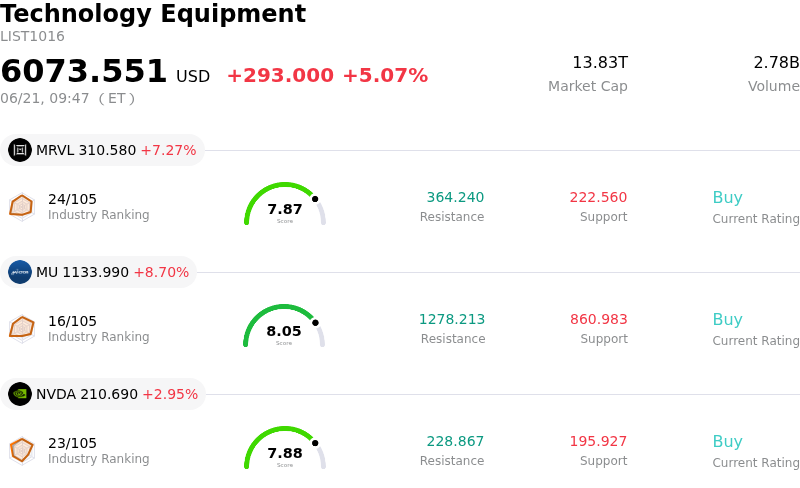

Taiwan Semiconductor Manufacturing Co Ltd (TSM) opened up by 6.86%. The Technology Equipment sector is up by 5.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Taiwan Semiconductor Manufacturing Co Ltd (TSM)’s stock price up today?

The robust upward surge and notable intraday volatility of Taiwan Semiconductor Manufacturing Company (TSMC) can be attributed to a confluence of stellar financial indicators, sector-wide momentum, and strategic operational milestones. At the core of this positive performance is the insatiable global demand for advanced semiconductor nodes, propelled by the relentless expansion of generative artificial intelligence and high-performance computing. TSMC's recent monthly sales data highlighted this growth trajectory, with its May revenue registering a record-breaking double-digit year-over-year increase, reinforcing its critical role in the global tech hardware supply chain.

Investor enthusiasm has been further amplified by the company's formidable pricing power. Facing rising upstream costs and tight advanced-node capacity, TSMC's plans to implement price hikes for its advanced foundry services have reassured the market of its ability to sustain elite profit margins. Backing this confidence, management raised its full-year revenue projections, forecasting growth of over thirty percent in U.S. dollar terms and driving its capital expenditures toward the high end of its guidance range to aggressively expand next-generation capacity.

On the operational front, TSMC’s newly established ten-year partnership with Amkor Technology has significantly bolstered confidence in its onshore expansion. This collaboration focuses on building out advanced packaging capabilities in Arizona, directly addressing supply chain bottlenecks for high-performance computing and AI customers who demand domestic manufacturing security. This strategic move strengthens the company's ecosystem and helps safeguard its long-term market dominance against geopolitical and logistics challenges.

Complementing these fundamental drivers, positive internal sentiment has sent strong buy signals to the market. Recent insider trading disclosures revealing open-market stock purchases by senior executives have signaled profound internal confidence in the company's long-term valuation. Consequently, Wall Street analysts have aggressively upgraded their target prices, emphasizing TSMC's near-monopolistic position in advanced nodes as a key growth catalyst.

While the broader semiconductor sector enjoyed a powerful rally, minor headwinds such as emerging dual-supplier strategies by major tech clients and regulatory discussions regarding tighter export controls did little to dampen the overall bullish momentum. The stock's significant appreciation reflects a market that remains overwhelmingly confident in TSMC's position as the primary engine powering the global artificial intelligence revolution.

Technical Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Technically, Taiwan Semiconductor Manufacturing Co Ltd (TSM) shows a MACD (12,26,9) value of 1.931, indicating a buy signal. The RSI at 63.428 suggests neutral condition and the Williams %R at 5.192 suggests overbought condition. Please monitor closely.

Fundamental Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Taiwan Semiconductor Manufacturing Co Ltd (TSM) is in the Technology Equipment industry. Its latest annual revenue is $122.22B, ranking 2 in the industry. The net profit is $55.12B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $458.87, a high of $600.00, and a low of $351.00.

More details about Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Company Specific Risks:

- U.S. Patent Litigation and Potential Import Ban: TSMC is under active investigation by the U.S. International Trade Commission (ITC) following patent infringement complaints from licensing firms Longitude Licensing and Marlin Semiconductor regarding its advanced process nodes. With a preliminary ruling expected in June 2026, the company faces the direct threat of a potential U.S. import ban on chips manufactured with key AI-accelerator technologies.

- Loss of Client Dominance to Dual-Supplier Strategies: Persistent capacity bottlenecks at TSMC have prompted key tech and automotive clients to diversify their foundry partners. Reports on June 18, 2026, revealed that Apple has agreed to partner with Intel to manufacture chips domestically to reduce reliance on TSMC, while Google, AMD, and Tesla are actively pursuing Samsung's advanced process services, including plans for Tesla to exclusively manufacture its next-generation AI6 chip at Samsung's Texas facility.

- Consensus Growth Mismatch and Capex-Induced Margin Compression: TSMC's combined April and May sales growth of 24% year-over-year has underperformed Wall Street's quarterly expectations of 35%, raising the near-term risk of a Q2 revenue miss. Concurrently, TSMC's massive projected 2026 capital expenditures of $52 billion to $56 billion to expand advanced sub-3nm nodes and packaging infrastructure expose the company to severe fixed-cost underutilization and margin erosion if AI hardware demand softens.

- Advanced Packaging Transition and Competitive Execution Risks: As TSMC races to commercialize its next-generation advanced packaging platform, Chip-on-Panel-on-Substrate (CoPoS) and Panel-Level Packaging (PLP), it faces steep technological hurdles. Samsung Electronics currently maintains a multi-year lead in PLP technology, putting intense pressure on TSMC as it attempts to finalize material and equipment qualification by late June 2026 to secure its pilot lines.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.