Micron Technology (MU): What to Expect From the June 24 Earnings Report

AI Podcast

Micron Technology is set to report fiscal Q3 2026 earnings on June 24, with consensus estimates projecting $34.66 billion in revenue and $19.95 EPS. Transitioning from a commodity provider to a pivotal AI infrastructure player, Micron benefits from its HBM oligopoly and strong demand from hyperscalers. Despite a recent pullback, analysts maintain a "Strong Buy" rating, citing record margins and HBM4 growth. Key monitorables include forward-looking HBM4 allocations, fiscal 2026 guidance, and sustainability of gross margins amid rising CAPEX and intensifying competition from SK Hynix and Samsung. Potential risks include evolving AI efficiency and hardware demand volatility.

TradingKey - Micron Technology (Nasdaq: MU) is scheduled to report fiscal Q3 2026 results on June 24 after market close, and the Street is expecting figures that would have been unimaginable 18 months ago. The memory-chip behemoth has evolved from a commodity play into a pivotal player in the AI infrastructure build-out, contributing to the stock's nearly 700% rise over the past year. It's one of the most meaningful prints in the company's history, with consensus EPS of $19.95 and revenue of $34.66 billion.

See what Analysts are looking for!

Wall Street consensus is $20.25, representing a +942% year-over-year jump from $1.91 earned in the same quarter last year, according to TipRanks. Revenue consensus is around $34.66 billion, a 272% increase from the previous year. That is in line with Micron's own estimates of $33.5 billion ± $750 million in revenue and non-GAAP EPS of $19.15 ± $0.40, with a gross margins forecast of around 81%, the highest of the company's history and among the best in the semiconductor industry.

A difference between the company's estimate and Street consensus is not a red flag, the company has a history of issuing conservative targets and beating them. In Q2, it delivered $23.86 billion against an $18.7 billion estimate, and has beaten EPS estimates by 30-40% over the past several quarters. If this trend repeats, then the real print may move significantly higher than $20. The report is already being factored into the options trades for a 17.6% move in the stock, either up or down.

The reason why MU Surged — and why it just pulled back!

MU stock rose roughly 700% over the past year to trade near $947, before a sharp 20% pullback knocked it off its all-time high. That selloff was triggered in mid-June when Broadcom's AI revenue forecast came in below expectations, reigniting fears that peak AI hardware demand may be closer than assumed. Micron, deeply tied to AI infrastructure spending, got caught in that sector-wide de-rating.

But the force behind the rally hasn't changed: AI data centers need a ton of high-bandwidth memory (HBM), the specialized chips placed next to GPUs to process data at AI-model speed. Micron is one of just three companies in the world, along with SK Hynix and Samsung, that can produce HBM on a large scale. This oligopoly structure and multi-year supply agreements have granted Micron pricing power it has never had before in their decades-long history as a commodity memory maker.

What Is HBM4, and Why Does It Matter for Micron's Revenue?

The next generation of high-bandwidth memory, HBM4 is already shipping in high volume, and Micron is a qualified supplier for Nvidia's new Vera Rubin AI platform, which is the successor to Blackwell. Vera Rubin offers 288 to 384 GB of HBM4 memory on each GPU package, providing approximately 22 terabytes per second of memory bandwidth, nearly three times that of Blackwell.

In supply side, SK Hynix has the first-mover advantage because of its manufacturing process and partnership with TSMC, with around 60-70% of Vera Rubin's HBM4 volume, while Samsung controls around 25-30% and Micron owns the remaining volume.

That's a significant business even at 10-15% volume, as Micron says HBM will be a $100 billion business by 2028 at today's price point of ~$500 per stack. The most critical forward-looking indicator on the call will be management's commentary on June 24 regarding the trajectory for HBM4 allocations, such as platforms for Vera Rubin Ultra in 2027.

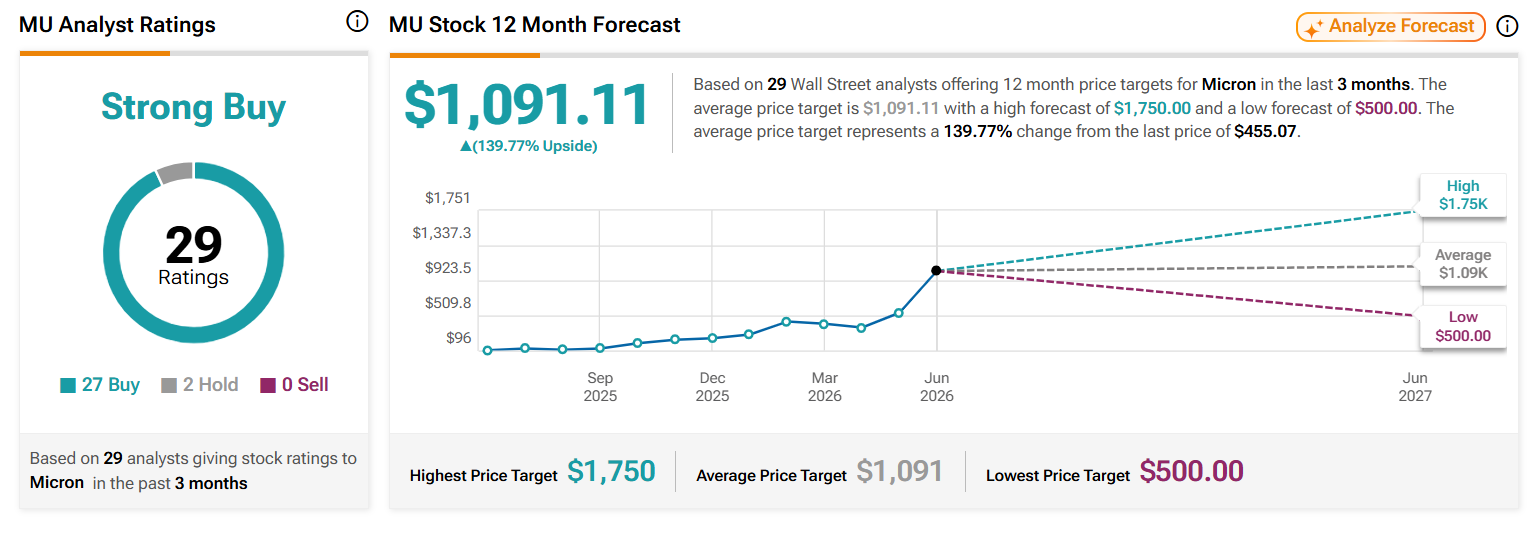

What Are Analysts Saying Ahead of the June 24 Print?

The sentiment for the week prior to print remains quite positive with a consensus rating of Strong Buy by 27 analysts covering MU, with no analysts assigning a sell rating. That's not been the case with the stock, though, as the average price target is around $1091, a strange situation in which the general sentiment is bullish, but the price targets are lagging the stock.

Source: Tipranks

Significant recent activity: RBC Capital has elevated its $525 target to $1,200 on June 15 based on AI demand, while C.J. Muse at Cantor Fitzgerald is the Street's most aggressive target at $1,500. Goldman Sachs identified tight DRAM supply and a better visibility of margins as the two important themes for Q3. For full fiscal 2026, analysts project EPS of $57.71, up 651% from $7.68 in fiscal 2025, with further growth to $97.77 expected in fiscal 2027.

What Are the Key Risks Investors Should Watch?

The bull case is good but has actual risk. The stock's $1 trillion valuation reflects expectations that the market has reached a new era in which demand for AI has ended the memorable up-and-down run of memory. However, if hyperscalers continue to purchase less or train AI models more efficiently than anticipated, HBM demand may weaken before Micron's new capacity is available.

Micron is also well on track to go big on CAPEX next year, currently projected at more than $25 billion in fiscal 2026, and increasing even more in fiscal 2027, with new fabs in Taiwan, Singapore, New York, and Idaho slated to reach significant wafer production levels, at the earliest, in 2027-2028.

That spending is seen to be reducing free cash flow while growing operating income to new heights. There is also a growing competition: SK Hynix has about 62% share in the HBM market and currently is ahead of Micron in terms of per-pin speed in HBM4, while Samsung also continues to ramp its capacity.

What Should Investors Look for in the June 24 Earnings Call?

Four additional data points will drive the market reaction: Q4 guidance and if the sequential revenue growth continues into the August quarter, HBM volume commentary, and any early signal on 2026 allocation, and DRAM/NAND pricing, with Micron's guidance indicating calendar 2026 DRAM bit shipments will increase in the low-twenties percent range; gross margin sustainability beyond the ~81% Q3 record into Q4.

As per Simply Wall St, full-year fiscal 2026 revenue growth has been raised to $108.7 billion, with the EPS projected at $58.05, which would have seemed ludicrous a year and a half ago. The June 24 edition of the AI memory cycle will be a big indicator of whether MU's unmatched streak can keep going.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.