Sea Ltd Stock (SE) Closed Down by 5.31% on May 14: A Full Analysis

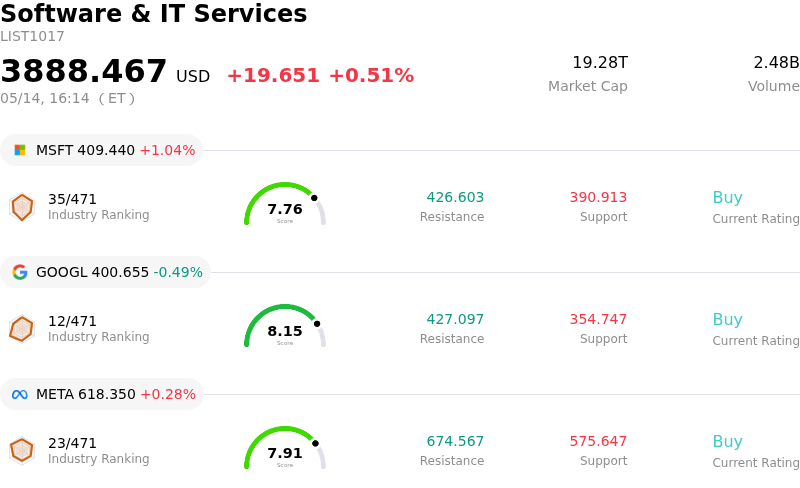

Sea Ltd (SE) closed down by 5.31%. The Software & IT Services sector is up by 0.51%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 1.04%; Alphabet Inc Class A (GOOGL) down 0.49%; Meta Platforms Inc (META) up 0.28%.

What is driving Sea Ltd (SE)’s stock price down today?

Sea Limited (SE) is experiencing downward movement and intraday volatility primarily due to a nuanced reaction to its recently reported first-quarter 2026 earnings. While the company demonstrated robust top-line growth, a key financial metric fell short of analyst expectations, leading to a mixed market response.

The company announced significant revenue growth, with its GAAP revenue for Q1 2026 increasing substantially year-over-year and comfortably surpassing consensus estimates. This strength was broad-based, with strong performances across its e-commerce segment, Shopee, which achieved record gross merchandise value and revenue. The digital financial services arm, Monee, also saw considerable revenue growth, and the gaming division, Garena, delivered its strongest quarter in several years. The company reaffirmed its full-year guidance for Shopee's gross merchandise value growth, along with an outlook for stable or improving adjusted EBITDA.

However, despite the impressive revenue beat, the company's earnings per share (EPS) missed analyst forecasts. This disparity between strong revenue and a less favorable EPS figure may have contributed to investor caution. Although net income and adjusted EBITDA showed year-over-year increases, their growth rates lagged behind the substantial revenue expansion, suggesting ongoing investments in logistics, ecosystem development, and other operational areas which can impact short-term profitability.

Furthermore, a series of insider share sales by several key executives, including the Chief Compliance Officer, Chief Product Officer, and Chief Operating Officer, were reported over the past few days. While these transactions were conducted under pre-arranged Rule 10b5-1 trading plans, which are designed to allow insiders to sell shares systematically, a pattern of such sales can sometimes be interpreted by the market as a potential signal, potentially adding to negative sentiment.

Analyst reactions to the earnings were varied; while some reiterated Buy ratings and even raised price targets based on the overall revenue strength and segment performance, the EPS miss and the company's valuation against its peers likely prompted some re-evaluation among investors. The market appears to be weighing the strong growth narrative against the immediate profitability metrics and insider activity, contributing to the current volatility.

Technical Analysis of Sea Ltd (SE)

Technically, Sea Ltd (SE) shows a MACD (12,26,9) value of [-0.04], indicating a neutral signal. The RSI at 58.95 suggests neutral condition and the Williams %R at -35.59 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Sea Ltd (SE)

Sea Ltd (SE) is in the Software & IT Services industry. Its latest annual revenue is $22.94B, ranking 19 in the industry. The net profit is $1.58B, ranking 34 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $140.15, a high of $195.00, and a low of $108.00.

More details about Sea Ltd (SE)

Company Specific Risks:

- Adjusted Earnings Per Share (EPS) of $0.67 for Q1 2026 missed analyst consensus estimates of $0.75-$0.77 per share, indicating profitability challenges despite strong revenue growth.

- The Shopee e-commerce segment's adjusted EBITDA declined by 15.5% year-over-year to $223.2 million in Q1 2026, due to continued investments in growth and subsidies, signaling potential margin compression in its primary growth driver.

- Provision for credit losses in the financial services segment surged by 65.1% to $465.5 million in Q1 2026, contributing to higher operating costs and impacting overall net income.

- Multiple insiders, including COO Ye Gang and CCO Wang Yanjun, engaged in open-market sales of Class A ordinary shares between May 12-13, 2026, potentially indicating a lack of confidence in the company's near-term outlook.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.