Applied Materials (AMAT) Earnings Preview: AI Chip Demand, Capital Expenditure Trends, & Trade Setups - In Progress

AI Podcast

Applied Materials (AMAT) stock has surged 179.83% in the past year, heavily outpacing the S&P 500 and XLK ETF, driven by AI chip demand. The company's upcoming Q2 2026 earnings report, with EPS expected at $2.66, hinges on continued momentum in DRAM and high-bandwidth memory equipment. Analysts maintain a positive "Strong Buy" consensus, with Morgan Stanley raising its price target to $454. Key drivers include customer capex cycles from TSMC and Micron, and expanded packaging solutions. Confirmation of over 20% semiconductor equipment business growth for 2026 and a strong second-half outlook are crucial. Downside risks include a conservative forecast and potential headwinds from Chinese exports.

TradingKey - The May 14 report comes when AMAT has risen by 179.83% over the past year and the whole semiconductor equipment cycle rests on AI demand for cutting-edge chips.

As AMAT announces its Q2 2026 earnings report after the market close on May 14, the story will not be just about whether the company beats expectations. Shares of Applied Materials have re-rated massively – AMAT rose by 179.83% over the past 52 weeks vs the S&P 500, which gained 30.73% over the same period and the XLK technology ETF, up 61.32%.

Being at those lofty heights, the company needs to deliver on all fronts and provide guidance consistent with the market's expectations.

Setup: What the Street Anticipates

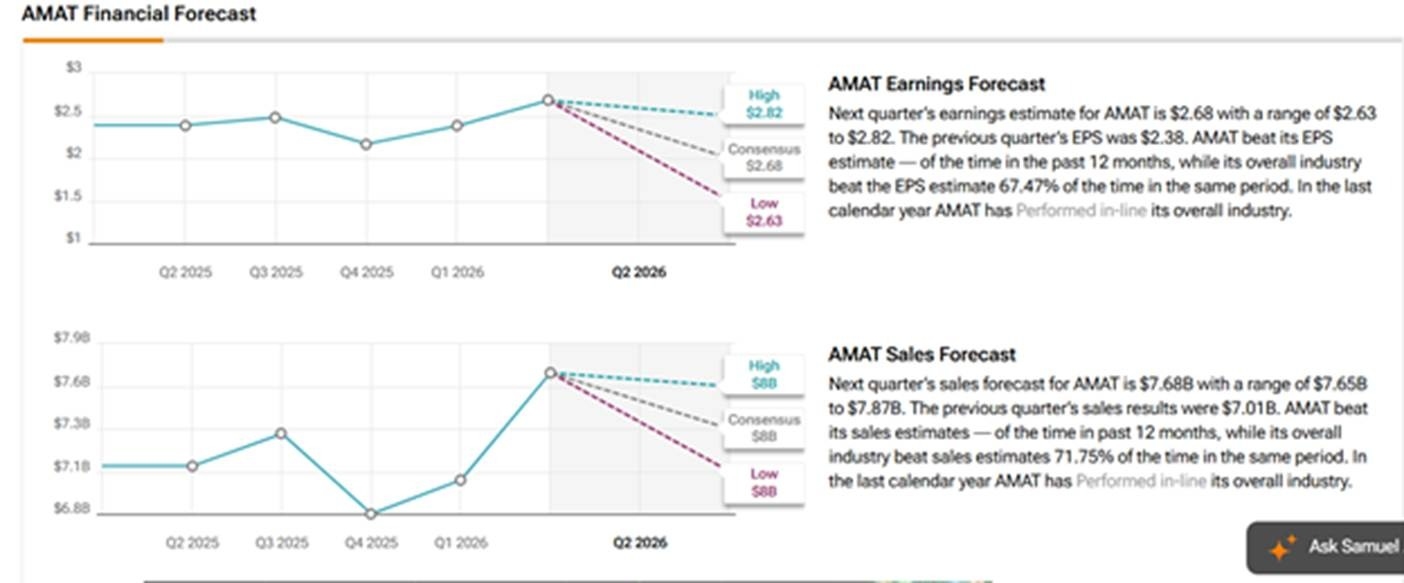

The EPS consensus is estimated at $2.66, representing a 11.3% increase compared to $2.39 in the previous-year quarter. For the last four quarters, Applied Materials reported EPS above analyst estimates. In its Q2 2026 guidance issued in February, management projected revenue to come in within the wide range between $7.15 billion and $8.15 billion. That midpoint implies a meaningful step-up from the $7.01 billion reported in Q1 2026, and the wide band signals management is being cautious about near-term visibility.

Looking ahead, the street consensus estimate for the July quarter stands at $2.94, up by almost 19% YoY, while the annual fiscal 2026 EPS is expected at $11.14, marking a 18% increase relative to $9.42 for FY25.

Image Source: https://www.tipranks.com/stocks/amat/forecast

AI Chip Equipment Thesis: DRAM – The Key Driver

Applied Materials is not a pure-play AI chip company, but it is the one with the strongest connection to AI right now. Applied Materials has the highest exposure to DRAM among its semiconductor equipment peers, comprising 31% of calendar 2026 revenue, based on the Morgan Stanley research. The number is crucial since the ongoing AI build-out is driving a huge demand for high-bandwidth memory (HBM), exceeding what foundries can do. Morgan Stanley is explicitly bullish on both DRAM and Micron, and its quantitative analysis finds that being bullish on Applied Materials is equivalent to being bullish on DRAM specifically.

Supporting the narrative, management confirmed the thesis during the Q1 2026 conference call. It said that the demand remains robust, fueling wafer fabrication equipment (WFE) growth driven by AI, leading-edge foundry logic, improved DRAM and HBM, and slow NAND. Crucially, CFO Brice Hill mentioned the company's plan to achieve more than 20% semiconductor equipment business growth in calendar 2026. Confirmation of the statement on May 14 would be the most bullish data point for investors.

Customer Capex Cycle Drivers: The Customers Spend

A rare alignment of customer capex cycles creates a tailwind for Applied Materials. The capital expenditures for Taiwan Semiconductor are expected to reach $54 billion in 2026, while for Micron to reach $25 billion. Further, there are several new plants, set to open only in 2027 and 2028. Such delayed openings imply the extended demand for equipment well into the next fiscal year – a structural tailwind AMAT is best positioned to capitalize on.

The actions demonstrate Applied Materials' confidence. The company signed a definitive agreement with ASMPT Limited to acquire NEXX, a top supplier of large-area advanced packaging solutions. The transaction aims at expanding its panel-level packaging offerings, enabling chipmakers to build large AI accelerators using less power. Additionally, with the opening of the company's $5 billion EPIC Center R&D facility, together with SK Hynix and Micron in addition to Samsung, it solidifies the position of Applied as a co-development partner on the leading edge of the memory stack.

Analyst Posture: Overweight with Precision

In anticipation of the May 14 report, Morgan Stanley raised its price target to $454 from $432, keeping its overweight rating. The rationale is clear – the firm referred to January quarter as 'a leap in the right direction' and called the coming quarter 'a second leap,' noting that the market might underestimate Applied Materials' ability to capture incremental customer value through expedited, power and integrated solutions and gross margin expansion. In other words, clear guidance on May 14 will lead to further re-rating.

The sentiment of the broad analyst community is also quite positive. Among the 28 analysts covering Applied Materials, the consensus rating is "Strong Buy," the average price target stands at $444, with the Street-high of $517.

Image Source: https://www.tipranks.com/stocks/amat/forecast

Historical Performance and Options Expectations

It is in historical performance where the trade setup gains its flavor. According to options, the implied move for the company is close to 6%. Historically, AMAT exceeded options' expectations in six out of its past eight earning announcements. The magnitude has been quite significant, as shares moved by 19.3% despite the implied move of just 7.4% in February, falling by 9.2% with the implied 5.4% change in August 2025, and dropping by 9.9% with the implied 6.4% change in November 2024. Hence, the 6% implied move seems to be underestimated significantly.

Trade Setup

Directional players will see the asymmetry in guidance: if management reaffirms its 2026 semiconductor equipment growth above 20% and indicates a strong second half of the year, the bulls will get justified. However, a conservative forecast of Q3 sales will indicate the opposite: it implies that the current price is too optimistic, considering the peak of the cycle reached. Q3 guidance and any indications of headwinds from Chinese exports, one of the persistent overhangs, will be the key drivers.

For volatility traders, AMAT's track record of outsized moves relative to implied pricing suggests that long straddles or strangles have historically been rewarded, even after accounting for the IV crush that follows the announcement. The most recent example came in February when the share price jumped nearly 20% despite a modest 7.4% implied move.

Bottom Line

Applied Materials is now the key pure-play name in semiconductor equipment, with all hopes of the whole industry resting on its shoulder. Beating revenue expectations, confirming the 20+% WFE growth target for 2026, and expanding gross margin will put the stock in a good spot. However, failure to beat guidance and indications of Chinese export softness will make AMAT, up by 179% in a year, vulnerable to downside. The 6% implied move in options looks moderate compared to the past performance. Trade accordingly.

This article is for informational purposes only and does not constitute investment advice. Options trading involves significant risk of loss.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.