Is the Weak Dollar Trend Reversing? De-Dollarization Continues — IMF Data Shows Decline in Dollar Reserves

TradingKey - Similar to the U.S. Dollar Index (DXY) posting its worst first-half performance in over half a century, data from the IMF’s latest COFER survey shows that the share of U.S. dollars in global official reserves has declined, while the euro and Swiss franc have gained ground.

According to the International Monetary Fund (IMF) report released on July 9, total official foreign exchange reserves rose from $12.36 trillion in Q4 2024 to $12.54 trillion in Q1 2025, largely reflecting gains by major currencies against the weakening U.S. dollar.

Within this:

- The dollar’s share fell from 57.79% to 57.74%

- The euro increased from 19.84% to 20.06%, marking its highest level since Q4 2022

- The Swiss franc tripled to 0.8%, reaching the highest level since the launch of the euro in 1999

It's worth noting that if the effect of dollar depreciation were excluded, the dollar’s share would have risen by 0.68 percentage points.

The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) data does not yet reflect the sharp drop in the dollar during Q2 2025, when trade tensions and the controversial Section 899 asset tax intensified capital outflows from the greenback.

In early April — before the April 2 “Liberation Day” tariff announcement and the April 9 implementation of reciprocal tariffs — investor confidence in the dollar had only begun to wane, with the DXY falling about 4% in Q1.

Since then, growing concerns over Trump’s tariff policies, potential Fed independence risks, and rising fiscal deficits have fueled a broader shift away from the dollar — reinforcing the “weak dollar narrative.”

Dollar Bounces Back — But Is It Just a Rally?

In early July, as President Trump’s 90-day tariff suspension ended , investors began rotating back into the dollar — betting that other currencies would weaken under the new tariff regime.

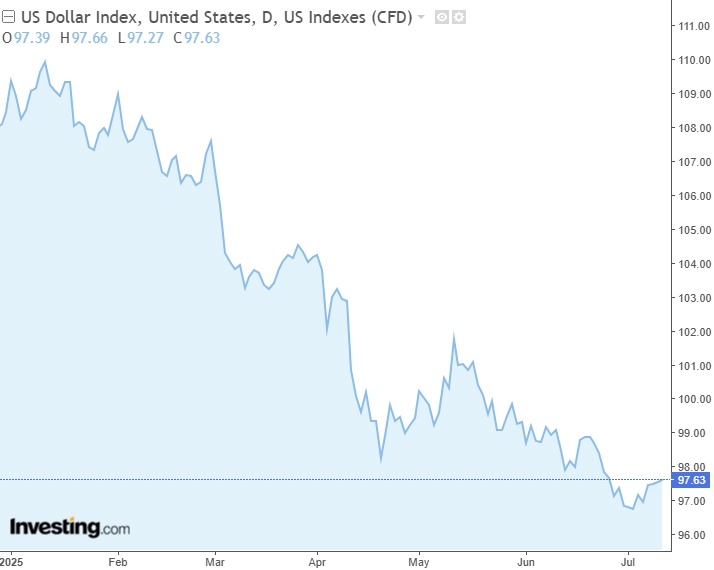

By July 10 , the DXY had rallied for four consecutive days, currently trading at 97.63 .

DXY in 2025, Source: Investing.com

However, analysts argue that this recent rebound may be temporary rather than structural.

Tianfeng Securities believes the dollar bear market is far from over, and that the greenback will likely remain on a downward path over the next 12 months. Any short-term rallies — such as in Q3 — could provide further opportunities for renewed short positions.

Analysts pointed out that several key factors still point toward long-term dollar weakness:

- No Fed rate hike in sight

- Stronger economic momentum in the eurozone compared to the U.S.

- A divergence in Fed and ECB rate cut timing expected in 2026

- Trump’s push for manufacturing repatriation requires a weaker dollar

Structural Challenges for the Greenback

This week, Goldman Sachs warned that the dollar may struggle to regain its traditional safe-haven appeal — citing three major headwinds:

- High policy uncertainty (including tariffs and Fed independence)

- Accelerating capital diversification away from the U.S.

- Rising fiscal concerns linked to government debt levels

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.