Why Is Bringing Manufacturing Jobs Back to the U.S. So Difficult? Do Trump’s Policies Backfire?

TradingKey - Since the 2008 financial crisis, bringing manufacturing back to the United States has been a top priority for multiple presidential administrations — yet this ambitious goal has faced persistent challenges and yielded limited success. The phenomenon of “manufacturing hollowing-out” remains a hotly debated topic in American society.

From Obama’s “reindustrialization,” Trump’s first-term "America First" policies and tariff wars, Biden’s CHIPS and Science Act, to Trump’s proposed record-high tariffs in his second term, successive governments have introduced a wide range of measures aimed at revitalizing U.S. manufacturing.

On May 27 , Trump threatened to impose a minimum 25% tariff on all iPhones manufactured overseas but sold in the U.S., sparking widespread controversy. Industry insiders responded that relocating smartphone production lines back to the U.S. would be extremely costly and time-consuming — making it economically unfeasible.

U.S. Trade Deficit and the Hollowing-Out of Manufacturing

In early April 2025, the White House released a document declaring a national emergency and announcing a baseline 10% tariff on all countries, with higher reciprocal tariffs imposed on those with large trade surpluses against the U.S. These measures were justified as ways to strengthen America's global economic position and protect domestic workers.

The administration insists that “Made in America” is more than just a slogan — it is a central pillar of Trump 2.0’s economic and national security strategy. The goal: reverse long-standing trade deficits and create high-paying jobs by producing more American-made cars, appliances, and other goods.

Since the 1970s, the U.S. economy has largely followed a pattern of current account deficit + capital account surplus, shaped by dollar dominance, financialized governance, consumer-driven growth, low savings rates, and global supply chain specialization.

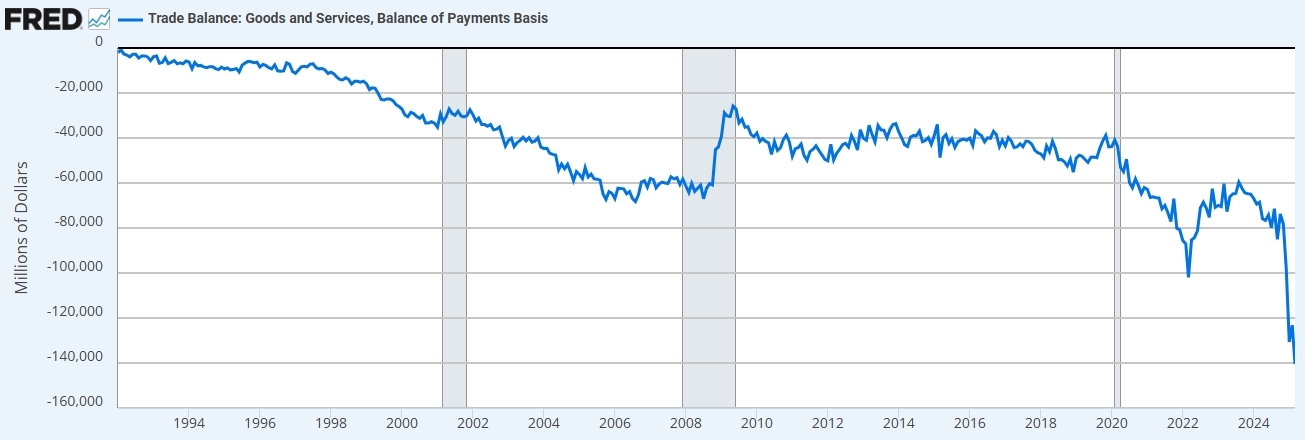

Trump aims to reverse this trend — targeting the trade deficit , which hit a record $140.5 billion in March 2025, with total imports reaching an all-time high of $419 billion.

U.S. Trade Deficit, Source: St. Louis Fed

According to the U.S. Department of Commerce, the record trade deficit dragged down Q1 GDP by 4.83 percentage points, marking the first negative growth since Q1 2022.

Much of the merchandise trade deficit stems from decades of offshoring. For example, during the pandemic, U.S. medical mask production dropped from 90% domestic to 95% foreign within a single year.

The so-called “hollowing out” of U.S. manufacturing refers to the declining share of U.S. manufacturing output in both global production and GDP, along with job losses and offshoring trends.

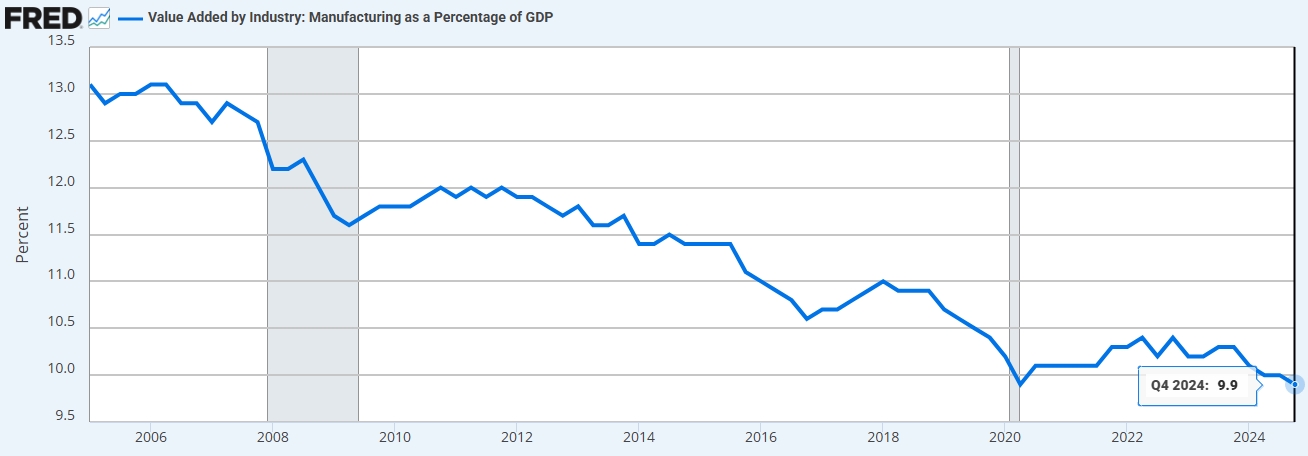

Data shows that the U.S. share of global manufacturing value-added fell from 25% in 2000 to 15.9% in 2024 . Meanwhile, the share of manufacturing in U.S. GDP declined from 13% at the turn of the century to just 9.9% in Q4 2024 .

U.S. Manufacturing Output as % of GDP, Source: St. Louis Fed

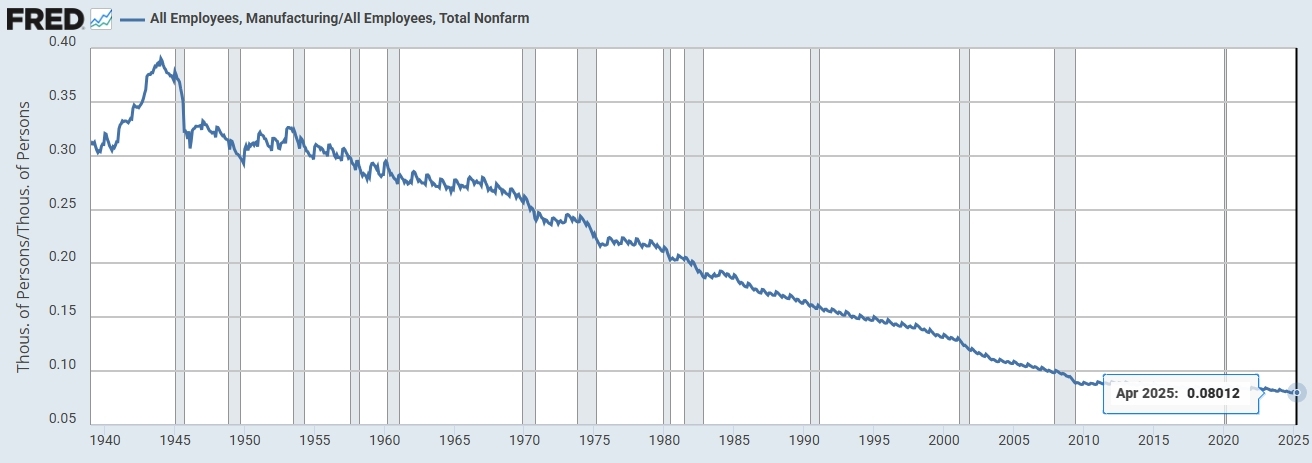

Post-WWII, the U.S. led globally in industries such as automobiles, steel, and aircraft manufacturing, employing over 30% of the labor force . As globalization progressed, U.S. comparative advantages evolved, and the economy shifted toward services and technology sectors. Today, only about 8% of the U.S. workforce is employed in manufacturing .

Manufacturing Employment Share in U.S. Workforce, Source: St. Louis Fed

The Trump administration claims that the U.S. lost around 5 million manufacturing jobs between 1997 and 2024 — one of the largest manufacturing employment declines in modern history.

What Makes Manufacturing Reshoring So Hard?

Whether under Obama, Trump, or Biden, bringing manufacturing back home has always been a key policy objective.

The U.S. manufacturing value-added in 2024 was $2.91 trillion, a figure larger than the total GDP of all but seven countries worldwide. This means the U.S. manufacturing sector alone would rank as the world's eighth-largest economy, ahead of countries such as Italy and Canada.

However, several structural and global challenges make reshoring increasingly difficult:

1. Economic Structure

The widening trade deficit and loss of manufacturing jobs are symptoms of a deeper imbalance in the U.S. economic model. The dollar’s global dominance , combined with high consumption and low savings behavior, fuels strong demand for imported goods.

As the U.S. economy has transitioned toward knowledge-intensive and service-oriented industries, labor has shifted away from manufacturing — accelerating deindustrialization.

2. Global Supply Chain Specialization

In today’s interconnected world, multinational corporations and SMEs alike leverage comparative advantages across borders to optimize cost efficiency and maximize profits. Labor-intensive manufacturing processes have moved to lower-cost regions like China, Vietnam, and Mexico.

Take Apple’s iPhone as an example: the U.S. leads in system design and innovation, China handles assembly using its demographic dividend, and Japan and South Korea supply competitive memory chips and display panels.

Fragmented global supply chains make full localization of production extremely difficult. In a globally open environment, most countries benefit from this model. Reversing existing supply chain structures comes at a high cost — including rebuilding entire ecosystems and significantly increasing production costs.

3. Talent and Technology Gaps

As the U.S. labor market shifts toward services and high-tech industries, traditional manufacturing faces a shortage of skilled workers and inadequate vocational training — leading to a mismatch between available skills and industry needs. Automation is also replacing many manual roles.

CIBC Capital Markets notes that the current U.S. unemployment rate (4.2% in March 2025) reflects a tight labor market, making domestic manufacturing recovery unlikely. Additionally, factory work holds little appeal for younger generations.

A Soter Analytics report found that only 14% of Gen Z — roughly one-third of the global population — would consider working in manufacturing. According to a survey by the National Association of Manufacturers (NAM), over 48% of respondents indicated that attracting and retaining manufacturing talent is their primary business challenge.

The NAM estimates that by 2033, the U.S. will need 3.8 million new manufacturing jobs , half of which could remain unfilled due to aging demographics and tighter immigration policies.

Moreover, filling these roles often requires accepting lower wages — a major hurdle for attracting talent in a highly competitive labor market.

4. Cost Disadvantages

U.S. manufacturing wages are far above those in countries benefiting from U.S. outsourcing. On average, U.S. workers earn 7 times more than Chinese workers , 11 times more than Mexican workers , and 16 times more than Vietnamese workers.

Reshoring also means abandoning existing global supply chain efficiencies and investing heavily in local infrastructure. Beyond construction costs, logistics and operational expenses in the U.S. are significantly higher.

According to a CNBC supply chain survey in April, 57% of respondents cited cost as the biggest obstacle to reshoring. 21% pointed to lack of skilled labor, while 18% noted that setting up domestic supply chains could double or even triple current costs.

Using Trump’s targeted example — Apple’s iPhone manufacturing — Wedbush analysts estimate that assembling an iPhone in the U.S. would cost $3,500, compared to the $1,000 price tag of a high-end iPhone 16 Pro. Analyst Ming-Chi Kuo argues that paying a 25% tariff is still more cost-effective than moving production back to the U.S.

Industry estimates suggest that shifting just 10% of Apple’s supply chain back to the U.S. would take three years and $30 billion — while a full relocation could take five to ten years.

How to Measure Manufacturing Reshoring Success?

Beyond rising U.S. manufacturing output, Brookings highlights key indicators:

- Employment: Since Trump’s return, manufacturing jobs have stagnated, with the sector’s share of non-farm employment remaining in single digits. Automation and AI are replacing workers, challenging job growth promises.

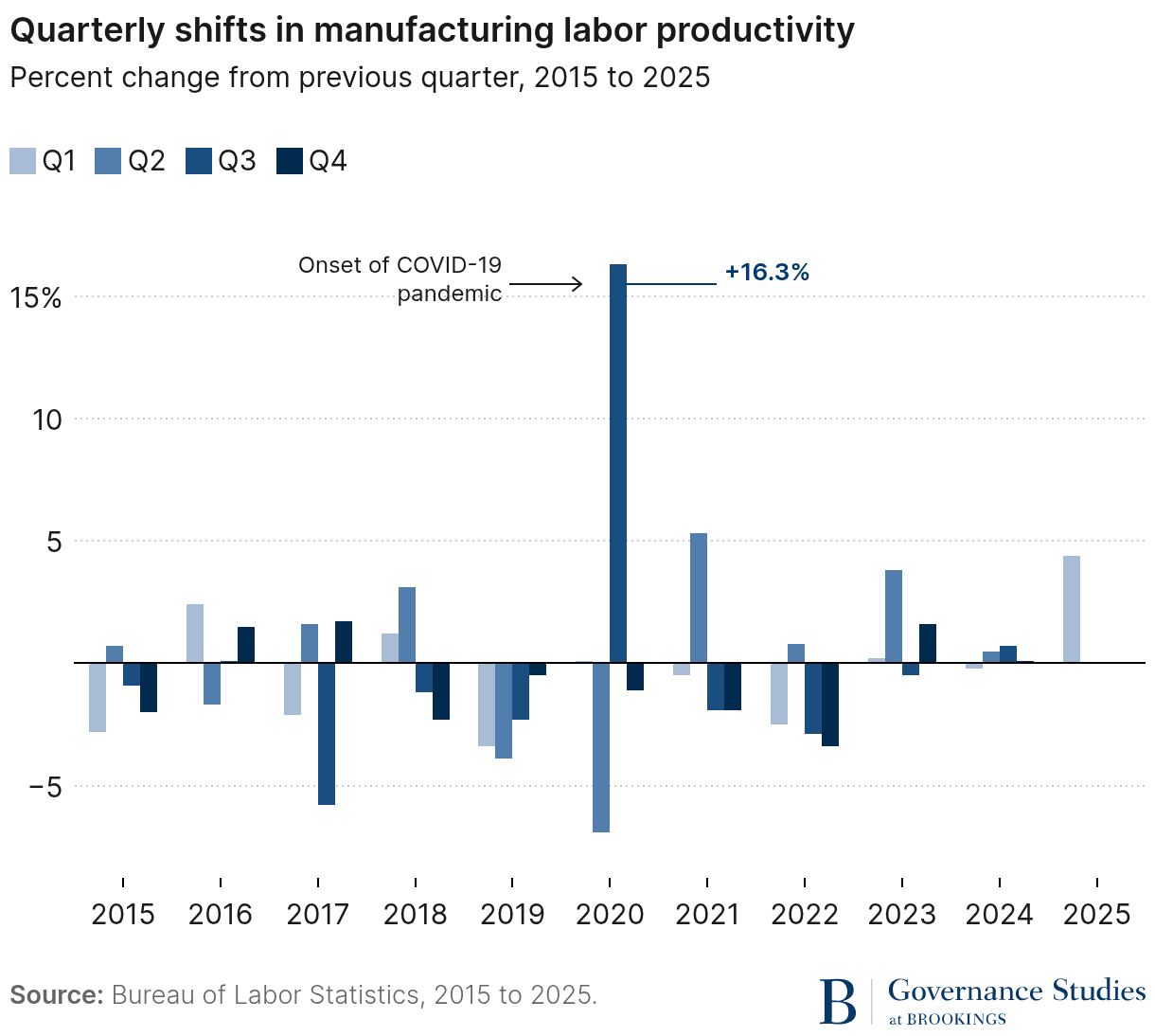

- Productivity: Manufacturing labor productivity has largely flatlined since 2015, despite technological advances.

- Trade Deficit: The largest deficits are with China, Mexico, Vietnam, Ireland, and Germany. Targeted negotiations with these nations could cut two-thirds of the gap.

- Foreign Investment: Companies like TSMC, Hyundai, Nissan, Siemens, and Apple have committed to major U.S. investments.

- Domestic Supply: Shortages in critical goods — like rare earths and pharmaceuticals — still hinder rapid scale-up.

What Has Trump Done to Bring Manufacturing Back?

To boost U.S. manufacturing competitiveness, the Trump 2.0 administration has implemented or proposed a comprehensive set of measures targeting businesses and workers:

- Tax cuts: Republicans are pushing for deep tax reductions for individuals and corporations.

- Tariff hikes: High tariffs on global trade partners aim to pressure companies into reshoring.

- Industrial policy: Launching the “Stargate” project; pressuring companies like Apple, TSMC, Johnson & Johnson, and Honda to increase U.S. investment; introducing tighter chip export controls to slow competitors and secure domestic tech leadership; streamlining regulatory procedures to encourage pharmaceutical firms to return production to the U.S.

- Vocational training: An executive order seeks to enhance technical education and workforce development.

U.S. Secretary of Commerce Howard Lutnick stated that community colleges will begin training students under a new model designed to provide lifelong careers in manufacturing. He added that this is a new model — you can work in these factories your whole life, and your children and grandchildren can too.

Lutnick emphasized that this new model will create good jobs — starting at $80,000 per year — accessible to those with only a high school diploma.

Why Tariffs May Not Bring Back Manufacturing

Despite the Trump administration’s insistence that tariffs are an effective tool for achieving economic goals, most Wall Street analysts disagree — arguing that tariffs fail to incentivize meaningful reshoring.

As of August 2025, the effective average tariff rate on all U.S. imported goods reached 18%, far exceeding 2.3% in 2024 and marking the highest level since 1930. Experts believe the "Reciprocal Tariffs 2.0" taking effect on August 7 will still fail to bring businesses back to the U.S.

A specialist from the Center for Strategic and International Studies (CSIS) said the policy might revive some textile production, but is insufficient to boost additional output in sectors like automobiles and steel.

A CNBC supply chain survey found that 61% of respondents believe tariffs will not bring manufacturing back, with over 60% considering moving operations to countries with lower tariffs instead.

Goldman Sachs cited academic research showing that a 10 percentage point increase in tariffs boosts protected sector employment by only 0.2–0.4%, while each 1% rise in production costs reduces employment by 0.3–0.6% — suggesting that tariffs may actually hurt employment in the long run.

JPMorgan CEO Jamie Dimon warned that tariffs do slow economic growth — and could even trigger a recession if mismanaged. While successful trade negotiations might bring short-term benefits, the long-term burden of tariffs will accumulate, becoming increasingly difficult to reverse.

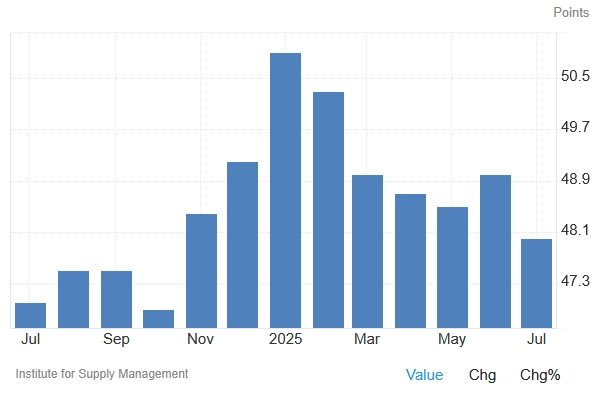

Data show that in the first seven months of 2025, the ISM Manufacturing Index remained above the 50 breakeven level in only two months, and has shown a downward trend.

United States ISM Manufacturing PMI, Source:Trading Economics

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.