Japan June Inflation Commentary: Impact on the Yen Exchange Rate

TradingKey - On 18 July 2025, Japan published its June inflation data, showing the headline Consumer Price Index (CPI) rising 3.3% year-on-year, a 0.2 percentage point drop from May’s figure. The core CPI, excluding fresh food, aligned with market forecasts, with its annual growth slowing from 3.7% in May to 3.3% in June. A significant decrease in Tokyo’s June CPI, alongside declining energy and utility costs and the government’s continued release of emergency rice stocks, helped curb inflation for the month. Moving forward, although Japan’s elevated inflation may have passed its peak, it is likely to stay above the Bank of Japan’s 2% target in the short term. This could lead the Bank of Japan to restart rate increases in Q3 or Q4 of 2025. Meanwhile, the Federal Reserve is expected to begin cutting rates in September 2025. With the interest rate gap between the two countries shrinking, we see potential for the yen to strengthen against the dollar.

Source: TradingKey

Main Body

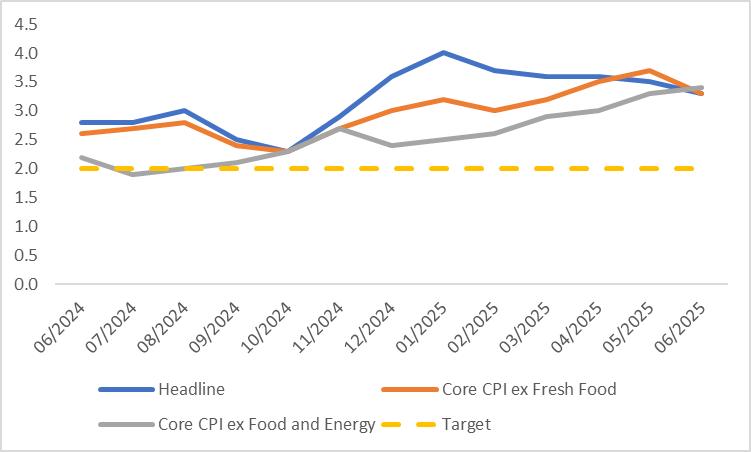

On 18 July 2025, Japan announced its June inflation figures. The headline Consumer Price Index (CPI) rose by 3.3% year-on-year, a decrease of 0.2 percentage points from May’s figure. Market expectations were confirmed, with the national CPI, excluding fresh food, showing a year-on-year increase that eased from 3.7% in May to 3.3% in June (Figures 1 and 2).

Figure 1: Market Consensus Forecasts vs. Actual Data

Source: Refinitiv, TradingKey

Figure 2: Japan CPI (%, y-o-y)

Source: Refinitiv, TradingKey

This development was primarily driven by three key factors:

First, Tokyo’s Consumer Price Index (CPI) for June saw a significant decline, with the headline CPI dropping by 0.3 percentage points and the core CPI falling by 0.5 percentage points. Given the leading nature of Tokyo’s inflation data, this slowdown had a notable impact on Japan’s nationwide inflation figures (Figure 3).

Second, gasoline prices, which had risen in May, experienced a month-on-month decline in June. Additionally, temporary reductions in water fees in regions such as Tokyo directly contributed to a decrease in the energy and utilities component.

Third, the Japanese government’s continued release of emergency rice reserves increased supply, which mitigated the upward pressure on food prices, further restraining inflation.

Figure 3: Tokyo CPI (%, y-o-y)

Source: Refinitiv, TradingKey

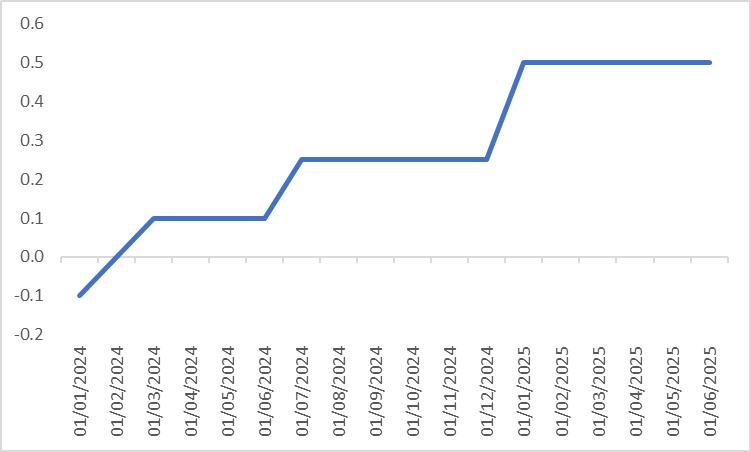

Looking ahead, while Japan’s high inflation may have peaked, it is likely to remain above the Bank of Japan’s (BOJ) 2% target in the near term. On the monetary policy front, since ending its negative interest rate policy in March 2024, the BOJ has raised rates by a cumulative 60 basis points (Figure 4). On 17 June 2025, the BOJ maintained its policy rate at 0.5% and announced that, starting in April 2026, it would reduce the pace of its balance sheet reduction from 400 billion yen per quarter to 200 billion yen. While this move may appear dovish on the surface, we believe it is unlikely to persist. Given that inflation is expected to significantly exceed the target in the short term, we anticipate the BOJ will adopt a hawkish stance and resume rate hikes in the third or fourth quarter of 2025. In contrast, the Federal Reserve is expected to restart rate cuts in September 2025. As the policy rate differential between the two countries narrows, we believe the yen has the potential to appreciate against the dollar.

Figure 4: BoJ Policy Rate (%)

Source: Refinitiv, TradingKey

Japan June Inflation Preview: Expected to Ease but Remain Above Target, Providing Short-Term Support for the Yen

TradingKey - Japan is set to release its June inflation data on 18 July 2025, with market consensus forecasting that the National CPI (excluding fresh food) will ease to 3.3% year-on-year from 3.7% in May. We concur with this outlook. The significant decline in Tokyo’s June CPI, falling energy and utility prices, and the Japanese government’s continued release of emergency rice reserves are expected to collectively suppress June’s inflation rate.

Looking ahead, while Japan’s high inflation may have peaked, it will remain above the Bank of Japan’s 2% target in the near term. This could prompt the Bank of Japan to resume its rate-hiking cycle in the third or fourth quarter of 2025. In contrast, the U.S. Federal Reserve is anticipated to restart rate cuts in September 2025. As the policy rate differential narrows, we believe the Japanese yen has room to appreciate against the U.S. dollar.

.jpg)

Source: TradingKey

Japan will release its June inflation data on 18 July 2025, with market consensus forecasting that the National CPI (excluding fresh food) will decline to 3.3% year-on-year from 3.7% in May (Figures 1 and 2). We agree with this outlook and believe that both headline and core CPI will fall below their previous month's readings.

.jpg)

Figure 1:Market Consensus Forecasts Source: Refinitiv, TradingKey

.jpg)

Figure 2: Japan CPI (%, y-o-y) Source: Refinitiv, TradingKey

This is primarily driven by three key factors:

First, Tokyo’s CPI for June experienced a significant decline, with headline and core CPI dropping by 0.3 and 0.5 percentage points, respectively. As a leading indicator, the slowdown in Tokyo’s inflation data substantially influences Japan’s national inflation figures (Figure 3).

Second, gasoline prices reversed their May increase, posting a month-on-month decline in June. Combined with temporary water bill reductions in Tokyo and other areas, this directly lowered the energy and utilities component.

Third, as the Japanese government continues to release emergency rice reserves, the increased supply is likely to ease the upward pressure on food prices. This will further contribute to suppressing inflation.

.jpg)

Figure 3: Tokyo CPI (%, y-o-y) Source: Refinitiv, TradingKey

Looking ahead, although Japan’s high inflation may have peaked, it is expected to remain above the Bank of Japan’s (BOJ) 2% target in the near term. On the monetary policy front, since ending its negative interest rate policy in March 2024, the BOJ has raised rates by a cumulative 60 basis points (Figure 4).

On 17 June 2025, the BOJ maintained its policy rate at 0.5% and announced that, starting April 2026, it would reduce the pace of its balance sheet reduction from 400 billion yen per quarter to 200 billion yen per quarter. While this move appears dovish, we believe it is unlikely to persist.

Given that inflation is expected to remain significantly above the target in the short term, we anticipate the BOJ will adopt a hawkish stance and resume its rate-hiking cycle in the third or fourth quarter of 2025. In contrast, the U.S. Federal Reserve is expected to restart rate cuts in September 2025. As the policy rate differential narrows, we believe the Japanese yen has the potential to appreciate against the U.S. dollar.

.jpg)

Figure 4: BoJ Policy Rate (%) Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.