Philip Morris International (PM): Successfully Moving Away from Traditional Products

Share Price (USD) | 178.88 | 2024 Revenue (USD) | 37.88bn |

Market Cap (USD) | 278.43bn | 2024 EPS (USD) | 4.52 |

Listings | NYSE | Dividend Yield | 3.04% |

52-wk high/low (USD) | 186.69-100.80 | Target Price (USD) | 203.15-237.26 |

Source: TradingView

Investment Thesis

TradingKey - Philip Morris International (PM) is perhaps the best positioned consumer stock at this moment. No other tobacco firm comes closer to the efforts PM is making to move away from traditional combustible products and no other big consumer company has the earnings growth potential as PM is having.

Company Background

Philip Morris sells over 130 brands of combustible cigarettes along with its flagship brand Marlboro – the world’s best selling international cigarette brand. In 2008, Philip Morris was separated from Altria (MO). They sell the same brands but Altria is selling them only in America, while PM is selling them globally.

In the last decade, PM has begun to provide smoke free alternatives like IQOS - heated tobacco system and ZYN - nicotine pouches, trying to revamp the company’s business.

Revenue Breakdown

To understand how the company makes money, we can see the revenue from two perspectives

Firstly, by product, we can roughly divide the revenue in two categories - combustible products (the old school cigarettes that need to be lighted in order to be smoked) and smoke-free products (heated tobacco like IQOS and any other smoke-free alternatives) that represent 40%.

The biggest revenue contributor for combustible products is Marlboro, while on the smoke-free side, IQOS is the best selling heated product. IQOS is estimated to bring $11bn in sales, or nearly 30% of the total firm’s revenue.

.jpg)

Source: Company Reports

Geography-wise, Europe brings 40% of the total sales, followed by South and Southeast Asia, CIS (ex-USSR), Middle East and Africa (30%). East Asia and Australia contribute 25% while Americas - 5%.

Market Share and Competition

If we exclude China National Tobacco Company which dominates in China (the absolute biggest tobacco market in the world), the global tobacco market is largely controlled by four players - Philip Morris (Altria in US), British-American Tobacco (BAT), Japan Tobacco and Imperial Brands. In most national markets, the top spot is held by either Philip Morris or BAT.

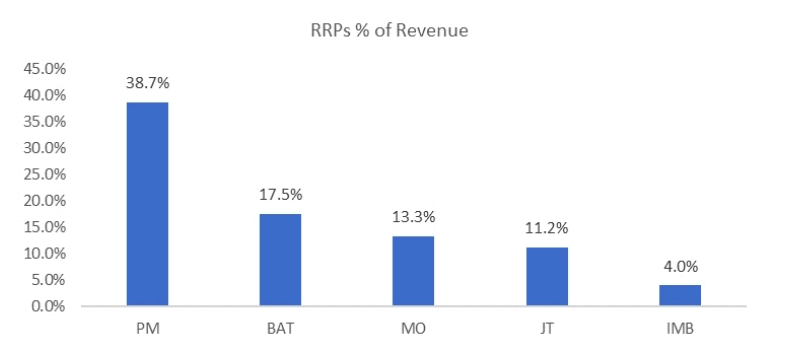

However, what differentiates PM from the rest is its smoke-free business. The company derives 40% of its revenue from the so-called reduced-risk products (RRPs). For comparison BAT has less than 20% of their revenue from such products. IQOS is already the best selling heating device globally, far outpacing the BAT equivalent “Glo”.

Source: Company Reports, Needham and Company

Growth Potential

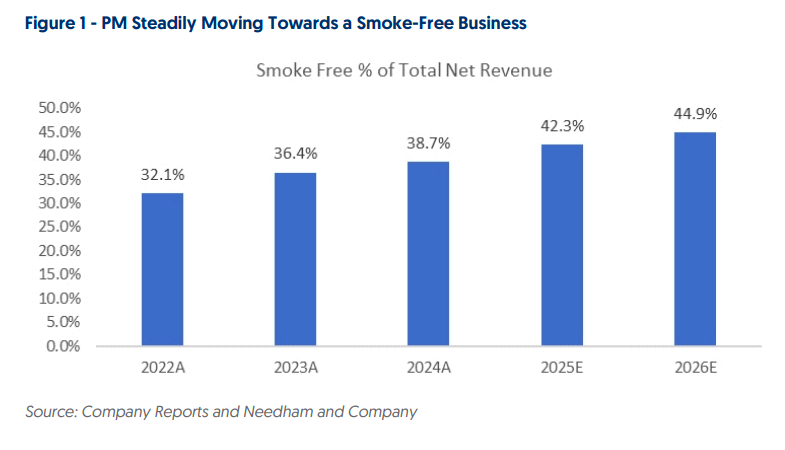

Despite Marlboro still being the best traditional cigarette brand, the PM growth is no longer relying on combustible products. Their new generation product’s growth has been outpacing and it is a matter of time to reach 50% of the total revenue.

Source: Company Reports, Needham and Company

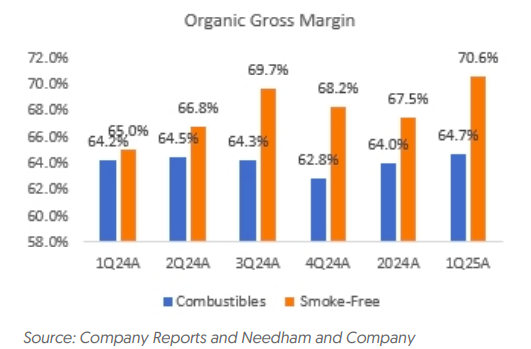

Not only that, the margins for smoke-free products is higher than combustibles, which will drive the margins up with the evolving revenue mix.

Source: Company Reports, Needham and Company

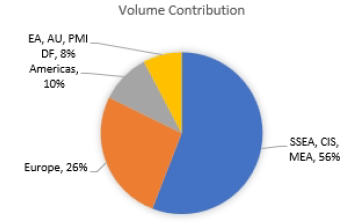

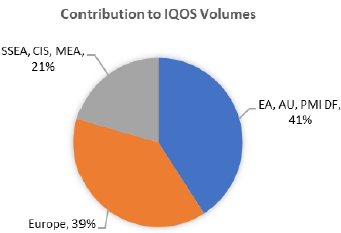

Apart from the developed markets, we see a huge growth opportunity for IQOS in SSEA, CIS and MEA, which represents 56% in terms of volume of combustible cigarettes sold but for IQOS the volume is just 21% - we believe that this huge gap will be narrowed over time.

Source: Company Reports

Finally, we have ZYN, the new generation nicotine pouches, currently at around $2bn revenue (5% of total) with an even higher gross margin of 86%, growing at above 20% year-over-year.

Both IQOS and Zyn are consumed mostly by people in the age range of 20-40 years old which is a plenty of time for Philip Morris to create a mind share among consumers.

Valuation

Despite the valuation of 36x PE being well above tobacco peers and large consumers players like Coca-Cola (KO), our discounted cash flow model suggests a target price above USD200. We believe the growth potential of the smoke-free products deserves a premium valuation, as this not only will drive double-digit top-line growth but will also help expand the margins even further, implying an EPS growth of high-teens. For comparison, the above-mentioned consumer giants will have an EPS growth of mid-single digits.

Risks

A potential risk for Philip Morris would include sudden hike in excise taxes will harm the net revenue in long term. Another risks may be related to competition among smoke-free products becoming more intense. Also, we should not forget that PM is an American company, but the business operations are almost entirely outside the country, exposing them to certain FX risks.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.