Zoom Communications Inc Stock (ZM) Moved Down by 7.79% on Apr 10: Facts Behind the Movement

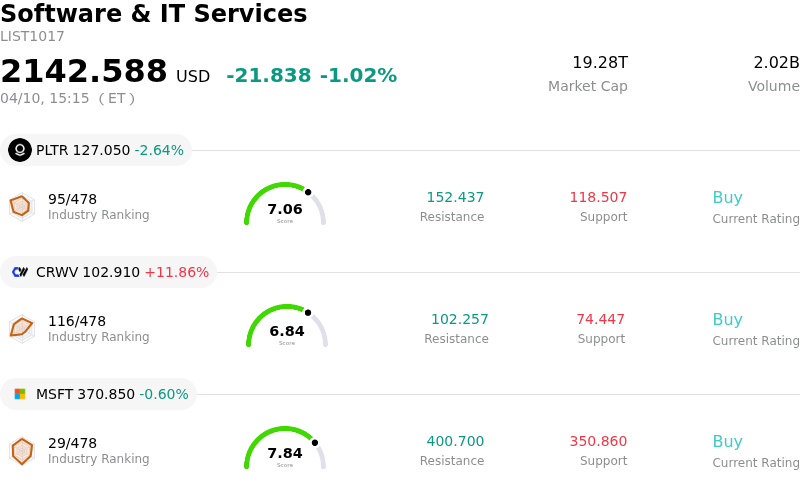

Zoom Communications Inc (ZM) moved down by 7.79%. The Software & IT Services sector is down by 1.02%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Palantir Technologies Inc (PLTR) down 2.64%; CoreWeave Inc (CRWV) up 11.86%; Microsoft Corp (MSFT) down 0.60%.

What is driving Zoom Communications Inc (ZM)’s stock price down today?

The recent negative intraday movement in Zoom Video Communications (ZM) share price appears to be primarily driven by a confluence of factors including analyst adjustments, lingering concerns from recent financial results, and ongoing questions regarding the company's growth trajectory within a highly competitive market.

Analyst sentiment has shown signs of caution, with some firms adjusting their price targets downward for Zoom. For instance, on April 10, 2026, BTIG lowered its price target, signaling a potentially revised outlook on the stock's future valuation. This follows earlier negative forecasts for April 2026, which anticipated a negative return on investment for the stock. Such adjustments can influence investor perception and contribute to selling pressure.

The market is also continuing to digest the company's fourth-quarter fiscal year 2026 earnings, reported in late February. While revenue surpassed expectations, the company's adjusted earnings per share missed consensus estimates, marking an end to a consistent streak of beating forecasts. More critically, the outlook for future free cash flow margins for fiscal year 2027 fell short of analyst projections, largely due to anticipated increases in capital expenditures and other financial headwinds. This guidance has fueled investor apprehension about future profitability and growth sustainability.

Furthermore, competitive pressures and the evolving market landscape continue to pose challenges for Zoom. Despite strategic initiatives to expand its offerings into unified communications, contact center solutions, and integrate advanced AI features, the company faces significant competition. Data indicates a net dollar expansion rate below 100% for enterprise customers in Q4 FY2026 and an elevated online monthly churn, suggesting that existing customers are either reducing their spending or not expanding their usage sufficiently, and the company is working hard to retain its customer base. This raises questions about the effectiveness of new product revenues in fully offsetting potential softness in its core video conferencing services. Additionally, reports of insider selling over the past three months may have also contributed to a cautious sentiment among investors.

Technical Analysis of Zoom Communications Inc (ZM)

Technically, Zoom Communications Inc (ZM) shows a MACD (12,26,9) value of [-0.33], indicating a neutral signal. The RSI at 60.98 suggests neutral condition and the Williams %R at -20.11 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Zoom Communications Inc (ZM)

Zoom Communications Inc (ZM) is in the Software & IT Services industry. Its latest annual revenue is $4.87B, ranking 66 in the industry. The net profit is $1.90B, ranking 28 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $97.53, a high of $115.00, and a low of $66.00.

More details about Zoom Communications Inc (ZM)

Company Specific Risks:

- Zoom Communications faces financial headwinds, including a sequential decline in gross margins to 79.8% and a significant miss in FY27 free cash flow margin guidance of 34% due to increased capital expenditures for asset refreshes.

- Analysts forecast a decline in the company's earnings by 9.5% annually over the next three years, with revenue growth projected to be slower than the broader U.S. market at 3.5% per year.

- The company is exposed to execution risks related to its internal sales culture and ongoing operational strategy changes, which analysts indicate could negatively impact future growth.

- A patent infringement lawsuit, "The California Institute of Technology v. Zoom Communications, Inc.," was filed against the company on March 1, 2026, introducing new legal uncertainty.

Recommended Articles