Snowflake Inc Stock (SNOW) Moved Down by 9.05% on Apr 10: Facts Behind the Movement

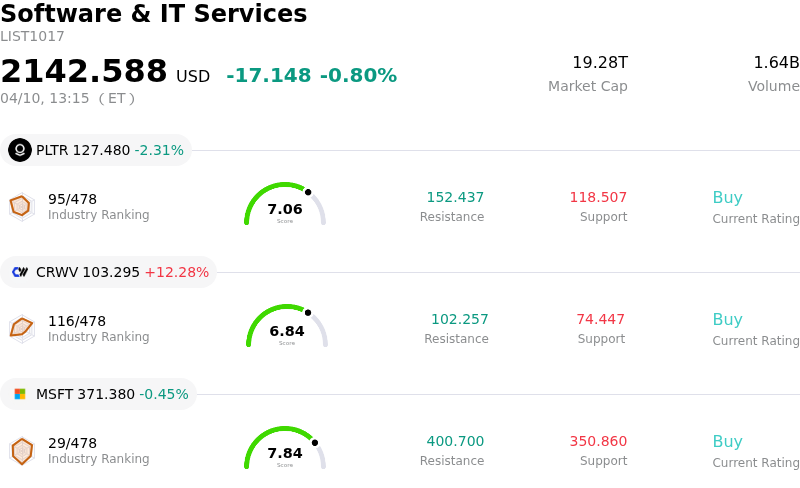

Snowflake Inc (SNOW) moved down by 9.05%. The Software & IT Services sector is down by 0.80%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Palantir Technologies Inc (PLTR) down 2.31%; CoreWeave Inc (CRWV) up 12.28%; Microsoft Corp (MSFT) down 0.45%.

What is driving Snowflake Inc (SNOW)’s stock price down today?

The notable downward movement in Snowflake (SNOW) stock on April 10, 2026, appears to be primarily driven by a combination of increasing legal scrutiny, ongoing concerns about competition, and a general negative sentiment towards the broader software sector.

Several class-action lawsuits have been publicized, alleging that Snowflake and its executives made misleading statements regarding customer usage patterns and revenue prospects. These lawsuits, with a lead plaintiff deadline of April 27, 2026, claim that the company failed to disclose that factors like Iceberg Tables, tiered storage pricing, and product efficiency improvements were expected to negatively impact sales and consumption. Such legal overhang can create significant uncertainty and pressure on the stock, increasing potential litigation costs.

Additionally, broader market sentiment and industry dynamics are contributing to the decline. The enterprise software sector, in general, has been facing a sell-off due to fears of AI disruption and concerns that autonomous agents could lead to margin compression for legacy software providers. While Snowflake is actively pursuing an AI strategy with tools like Cortex AI, it faces formidable competition from rivals such as Databricks and cloud giants like Microsoft, which are also aggressively targeting the enterprise AI market. Some analysts are divided on Snowflake's valuation, with one popular narrative suggesting the company is significantly overvalued at current prices.

Despite these headwinds, the company previously announced a change in its Chief Revenue Officer role on March 31, 2026, appointing Jonathan Beaulier. At that time, Snowflake reaffirmed its guidance for the first quarter and full year of fiscal 2027, signaling no change to its existing financial outlook, suggesting management maintained continuity in revenue expectations amidst the leadership transition. However, previous analyst reports noted a slight reduction in some price targets in late February 2026, alongside some reiterations of "Buy" ratings. Investor concerns regarding growth sustainability in a competitive landscape have also been highlighted by recent valuation adjustments, with a reduction in target multiples. While some analysts see potential for growth driven by AI adoption, the immediate market reaction seems to be weighing these competitive and legal pressures heavily.

Technical Analysis of Snowflake Inc (SNOW)

Technically, Snowflake Inc (SNOW) shows a MACD (12,26,9) value of [-7.02], indicating a sell signal. The RSI at 25.17 suggests sell condition and the Williams %R at -97.69 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Snowflake Inc (SNOW)

Snowflake Inc (SNOW) is in the Software & IT Services industry. Its latest annual revenue is $4.68B, ranking 69 in the industry. The net profit is $-1.33B, ranking 586 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $237.70, a high of $500.00, and a low of $170.00.

More details about Snowflake Inc (SNOW)

Company Specific Risks:

- Snowflake faces ongoing securities class action lawsuits with an impending lead-plaintiff deadline of April 27, 2026, alleging misleading statements regarding consumption patterns, revenues, and demand for its products due to efficiency gains, Iceberg Tables, and tiered storage pricing.

- The company is under increasing competitive pressure and faces potential disruption from advanced AI models, which threaten its data warehousing moat, premium pricing, and traditional SaaS business model.

- Concerns persist over slowing product revenue growth and management's cautious outlook, compounded by recurring quarterly net losses of approximately US$300 million and analyst downgrades.

- Recent significant insider share sales by executives, including an SVP of Engineering and other key personnel, are contributing to reduced investor confidence in the company.

Recommended Articles