Lam Research Corp Stock (LRCX) Moved Up by 3.09% on Mar 23: What Investors Need To Know

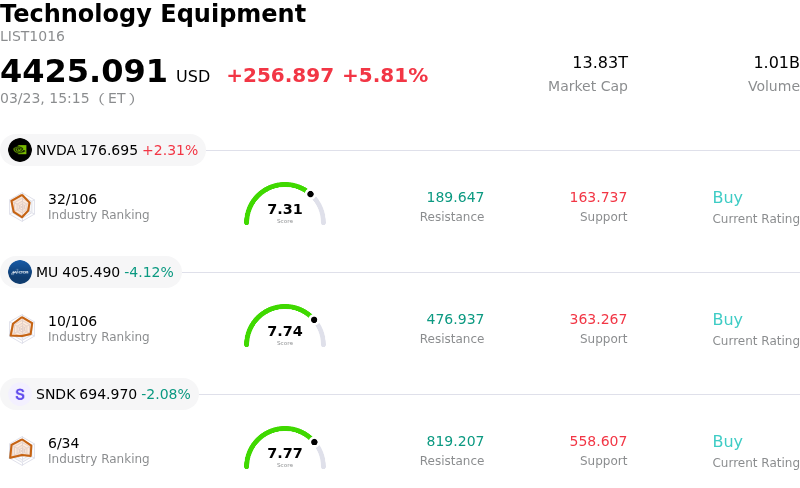

Lam Research Corp (LRCX) moved up by 3.09%. The Technology Equipment sector is up by 5.81%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.31%; Micron Technology Inc (MU) down 4.12%; SanDisk Corporation (SNDK) down 2.08%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research (LRCX) experienced an upward price movement with notable intraday volatility today. This performance appears to be largely driven by positive sentiment stemming from the company's recent strategic communications and robust financial indicators, supported by favorable industry dynamics.

A significant catalyst was the company's presentation at a recent investor conference in March. During this event, Lam Research highlighted an optimistic strategic outlook, particularly emphasizing the increasing demand for artificial intelligence computing which is expected to drive substantial growth in the Wafer Fabrication Equipment (WFE) market this year. The company also pointed to strong revenue growth achieved in the prior fiscal year, with gross margins consistently exceeding targets. Furthermore, the firm outlined significant opportunities in advanced packaging and Gate-All-Around technologies, along with its dry resist technology.

Investor confidence has also been bolstered by positive analyst sentiment. The stock currently holds a consensus "Outperform" recommendation from numerous brokerage firms, with a majority of analysts maintaining "Buy" ratings. Several analysts have recently increased their price targets for Lam Research, reflecting an optimistic view of its future prospects. This positive analyst outlook follows strong financial results reported in late January for the second fiscal quarter of 2026, where the company surpassed both revenue and earnings per share estimates and provided encouraging guidance for the upcoming quarter.

The broader semiconductor equipment industry continues to exhibit strong tailwinds, propelled by the accelerating demand for AI processors and ongoing investments in leading-edge logic and advanced memory solutions. Lam Research is well-positioned within this growth environment, given its critical role in providing equipment for advanced chip manufacturing. The company has also demonstrated technological leadership through recent collaborations to advance sub-1nm logic scaling. While some institutional investors have adjusted their holdings and insider selling has been noted, the prevailing market sentiment for LRCX remains constructive, buoyed by its strong market position and exposure to high-growth areas within the semiconductor industry.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [-1.11], indicating a neutral signal. The RSI at 52.87 suggests neutral condition and the Williams %R at -19.83 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $270.39, a high of $325.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Significant insider selling by the Chief Financial Officer and a director within the last 72 hours raises concerns about management's confidence in future performance.

- Ongoing vulnerability to US export controls and escalating geopolitical tensions negatively impacts sales practices and revenue contribution from the critical Chinese market, with reliance on China growing to 35% of revenues.

- The stock's stretched valuation, trading at peak cycle price-to-earnings ratios, makes it susceptible to profit-taking and sharper reactions to any negative news.

- Concerns persist regarding potential margin compression stemming from an unfavorable product mix and a projected decline in revenue from China.