The Week on Wall Street: Geopolitical Tensions Drove Markets Lower; Fed Held Rates, Noting Inflation Risks

AI Podcast

Geopolitical tensions in the Middle East and their impact on oil prices dominated market sentiment. US inflation held steady at 2.4%, with core inflation at 2.5%. The FOMC maintained the federal funds rate at 3.50-3.75%, citing increased uncertainty about commodity prices and inflation. US equities declined, with the S&P 500 down 5.1% year-to-date. Bond funds saw significant inflows, reflecting a flight to safety. Investors are advised to maintain caution, favoring diversified portfolios with defensive sectors and quality bonds amid persistent volatility and inflationary concerns.

Previous Week’s Market Review & Analysis

TradingKey - Macroeconomic Landscape: Escalating geopolitical tensions in the Middle East, particularly involving Iran, Israel, and the United States, dominated the macroeconomic landscape, driving significant market uncertainty. Concerns persisted regarding the potential for a wider regional conflict and its implications for global oil supplies, especially through the Strait of Hormuz. Oil prices remained elevated, with Brent crude trading around $102.26 per barrel at the week's start, briefly reaching $105, though WTI crude saw some easing to $94.75 by March 16. This surge in energy costs contributed to persistent inflationary pressures, with the annual US inflation rate for February 2026 holding steady at 2.4% and core inflation at 2.5% (data released this week). The Federal Open Market Committee (FOMC) held its scheduled meeting on March 17-18, maintaining the federal funds rate at 3.50-3.75%, an outcome broadly anticipated by the market. Fed Chair Powell's post-meeting remarks underscored increased uncertainty, particularly concerning the conflict's impact on commodity prices and inflation, and noted that near-term inflation expectations had risen due to the oil price spike. The FOMC’s updated economic projections indicated more robust growth but also more persistent inflation than previously forecast.

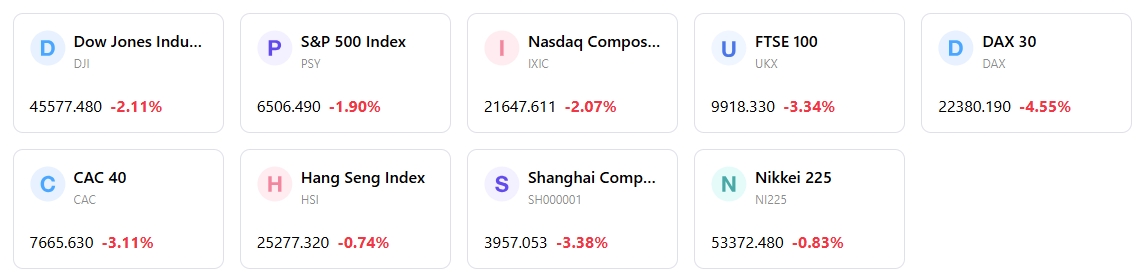

Market Performance Overview: US equity markets faced a challenging week, extending their recent retreat. The S&P 500 notably marked a fourth consecutive weekly loss, trading around 6,506.48 on March 20, down 5.1% year-to-date. Early in the week, some relief rallied the S&P 500 by 1.2% as crude oil prices temporarily eased, but overall sentiment remained pressured. Sector performance showed energy outperforming, while cyclical and growth-oriented sectors, including Industrials and Consumer Discretionary, generally underperformed. Defensive sectors like Utilities also saw modest gains. Value stocks continued to demonstrate relative strength against growth stocks.

Key Events Analysis: The FOMC meeting on March 17-18 was a central event, where the Federal Reserve maintained interest rates, conveying a cautious stance amidst a complex macro backdrop. The release of the Summary of Economic Projections provided insights into the Fed's view of sustained growth but elevated inflation risks. February 2026 US inflation data confirmed persistent price pressures. Geopolitical developments in the Middle East remained a critical market driver, directly influencing oil prices and investor sentiment.

Flows & Sentiment: US fund flows for February 2026, reported this week, highlighted a flight to safety, with bond funds and ETFs attracting substantial inflows. Taxable-bond funds gathered $85 billion, and international-equity funds saw their tenth consecutive monthly inflow of $33 billion, while US equity funds experienced outflows of $5.0 billion. This trend, coupled with near-record capital inflows into US-domiciled funds in Q1, underscored a market preference for perceived safety amid global turmoil. Market volatility remained elevated throughout the week, largely driven by geopolitical headlines.

Overall Assessment: The market logic for the week was dictated by the interplay of elevated geopolitical risks, their inflationary consequences via energy prices, and a cautious but resolute Federal Reserve. While the US economy showed signs of resilience, the specter of persistent inflation and ongoing global instability kept investors on edge, leading to broad equity market declines and a notable rotation into defensive assets and fixed income.

Next Week’s Key Market Drivers & Investment Outlook

Upcoming Events: The week ahead will include the release of the U.S. International Transactions and Investment Position for 4th Quarter and Year 2025 on March 25. A speech by Fed Chair Powell is also scheduled for March 22.

Market Logic Projection: Markets are expected to remain highly sensitive to any further developments in the Middle East conflict and their potential impact on global energy supplies and inflation. Central bank communications following the FOMC meeting will continue to be dissected for clues regarding the duration of current interest rate levels. Volatility is likely to persist as investors balance resilient economic data against geopolitical uncertainties and inflationary concerns.

Strategy & Allocation Recommendations: Given the heightened uncertainty and volatility, a cautious risk appetite remains prudent. Investors should favor diversified portfolios with an overweight stance on defensive sectors and those demonstrating resilience to higher energy costs. Fixed income, particularly quality bonds, may continue to attract inflows as a safe haven. Maintaining geographical diversification is also advisable.

Risk Alerts: Key risks include further escalation of geopolitical tensions, significant spikes in oil prices, and the potential for inflation to remain more persistent than anticipated, which could delay future monetary policy easing. Continued scrutiny of global trade policies and their economic implications is also warranted.

Markets Weekly

5-Day Index Performance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.