Arm Holdings PLC Stock (ARM) Moved Up by 3.79% on Mar 23: What Investors Need To Know

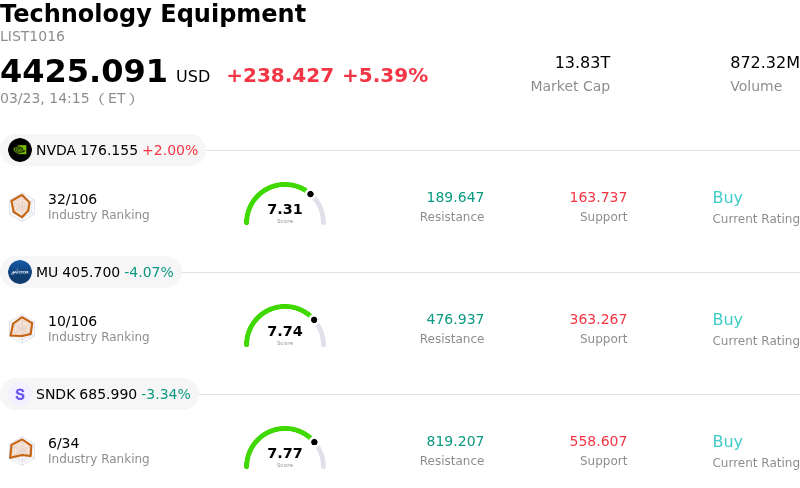

Arm Holdings PLC (ARM) moved up by 3.79%. The Technology Equipment sector is up by 5.39%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.00%; Micron Technology Inc (MU) down 4.07%; SanDisk Corporation (SNDK) down 3.34%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

ARM Holdings (ARM) experienced upward price movement today, largely driven by a combination of positive analyst sentiment, robust financial performance, and continued momentum in the artificial intelligence and data center sectors. Investors are particularly optimistic about the company's strategic pivot towards AI-driven server processors.

A significant catalyst for the stock's performance was a recent upgrade from HSBC, which raised its rating on ARM from "reduce" to "buy" and substantially increased its price target. This re-rating was based on the belief that the market was undervaluing ARM's transition into a major beneficiary of the AI server CPU market, highlighting a "game-changing" artificial intelligence-related narrative. Other analysts have also maintained bullish ratings, reflecting a consensus that ARM has a "Buy" rating based on recent research and market trends.

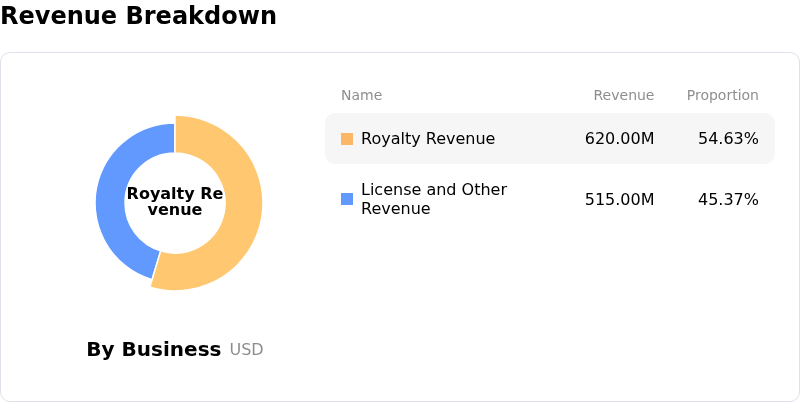

The company's strong fiscal third-quarter 2026 results (for the period ending December 31, 2025) further reinforced investor confidence. ARM reported significant year-over-year revenue growth, marking its fourth consecutive quarter of billion-dollar revenue. Both royalty revenue and license and other revenue demonstrated robust increases, primarily fueled by demand in AI, data centers, and advanced technologies. The company's data center royalty revenue has shown substantial growth, and ARM anticipates that its data center business will become its largest revenue driver in the coming years.

Furthermore, the anticipation of ARM's upcoming "Arm Everywhere" event on March 24, 2026, featuring CEO Rene Haas, is acting as a near-term sentiment catalyst. Traders are positioning for potential product and ecosystem updates related to AI and intelligent compute. This event is expected to highlight how ARM's engineering leadership and collaborations are enabling more efficient, scalable, and intelligent computing platforms. Industry dynamics, including the increasing demand for high-core-count CPUs for AI data centers and the adoption of ARM's v9 architecture and Neoverse Compute Subsystems, are also contributing to the positive outlook, as these advancements are expected to drive higher royalty rates per chip.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [0.88], indicating a buy signal. The RSI at 62.87 suggests neutral condition and the Williams %R at -26.49 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.01B, ranking 26 in the industry. The net profit is $792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $149.70, a high of $205.00, and a low of $81.78.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- The accelerating adoption of the open-source RISC-V architecture by major industry players like Qualcomm and Meta presents a significant long-term competitive threat to Arm's proprietary licensing and royalty business model.

- Arm's substantial revenue exposure (20-25%) to Arm China is subject to significant geopolitical risks and limited management control, creating potential disruptions to a critical revenue stream.

- Analyst concerns persist regarding slowing royalty growth, with Q4 guidance forecasting a deceleration to low-teens percentages and potential margin contraction, contributing to pressure on the stock's high valuation.

- The company's strategic shift toward compute subsystems introduces execution risks related to potential resistance from premium licensees valuing architectural independence and possible regulatory scrutiny over switching-cost tactics.