Seagate Technology Holdings PLC Stock (STX) Moved Up by 3.69% on Mar 13: What Signal Does It Send?

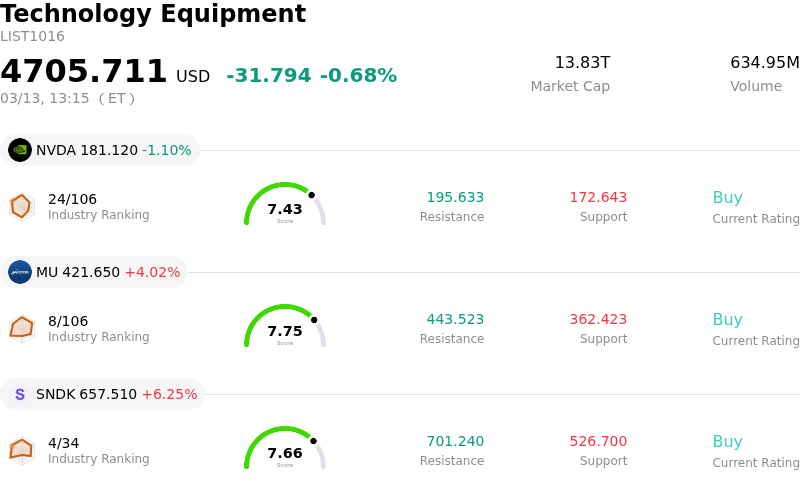

Seagate Technology Holdings PLC (STX) moved up by 3.69%. The Technology Equipment sector is down by 0.68%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 1.10%; Micron Technology Inc (MU) up 4.02%; SanDisk Corporation (SNDK) up 6.25%.

What is driving Seagate Technology Holdings PLC (STX)’s stock price up today?

Seagate Technology (STX) experienced an upward movement, largely driven by a combination of positive technological developments, robust financial performance, and favorable market sentiment. A significant catalyst has been the company's recent announcement and deployment of its next-generation Mozaic 4+ platform, featuring Heat-Assisted Magnetic Recording (HAMR) technology. This advanced storage solution, capable of capacities up to 44TB, is now in production and shipping in volume to leading hyperscale cloud providers, marking a critical milestone for AI-driven data storage needs. The industry views HAMR as a key enabler for higher capacity per drive and improved economics for AI infrastructure. Furthermore, Seagate's roadmap indicates a progression toward 100TB drives by 2030, with 40TB+ drives scaling volume production in early 2026.

The company's strong financial data also contributed to the positive momentum. Seagate reported robust second-quarter fiscal 2026 profitability, achieving a non-GAAP gross margin of 42.2% and a non-GAAP operating margin of 31.9%. These results included record exabyte shipments, gross margin, operating margin, and non-GAAP earnings per share. The fiscal second-quarter earnings per share of $3.11 surpassed consensus estimates, as did the revenue of $2.83 billion. Management has provided an optimistic fiscal 2026 outlook, anticipating revenue around $2.9 billion for the third quarter and continued margin expansion, with nearline production largely booked through the current year due to strong AI-related cloud demand. Analysts have also increased earnings estimates for fiscal 2026.

Market sentiment remains highly positive, with numerous research firms issuing "Moderate Buy" ratings and upgrading price targets for Seagate shares. The consensus analyst rating is currently "Buy," reflecting a belief that the stock is poised to outperform the market. This optimism is largely fueled by the perception of an ongoing "storage supercycle" and the expanding requirements of AI-driven data centers, positioning Seagate as a key beneficiary of these trends. Institutional investors have also shown increased confidence, with firms like Arrowstreet Capital Limited Partnership and Mackenzie Financial Corp significantly increasing their holdings in the company. Additionally, the recent announcement of a quarterly dividend likely further supported investor confidence.

Technical Analysis of Seagate Technology Holdings PLC (STX)

Technically, Seagate Technology Holdings PLC (STX) shows a MACD (12,26,9) value of [1.46], indicating a neutral signal. The RSI at 46.91 suggests neutral condition and the Williams %R at -62.15 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Seagate Technology Holdings PLC (STX)

Seagate Technology Holdings PLC (STX) is in the Technology Equipment industry. Its latest annual revenue is $9.10B, ranking 9 in the industry. The net profit is $1.47B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $473.02, a high of $700.00, and a low of $381.42.

More details about Seagate Technology Holdings PLC (STX)

Company Specific Risks:

- Significant insider selling activity, including a pattern of 133 insider sales with no purchases over the past six months and a substantial sale by the CEO earlier in March, signals potential lack of confidence from company leadership.

- Recent privately negotiated exchanges of $600 million in exchangeable notes for cash and a variable number of ordinary shares create near-term uncertainty regarding potential share issuance and dilution, which has contributed to recent stock declines.

- Analysts express concern over the company's stock being significantly overvalued, highlighting peak-cycle risks and a potential demand slowdown post-2027 for its Hard Disk Drive (HDD) segment, as its growth prospects and Average Selling Prices (ASPs) lag behind Solid-State Drives (SSDs).

- The company maintains an extremely high debt-to-equity ratio of 1046.6%, indicating heavy leverage that could amplify financial risks, especially in a rising interest rate environment.