TradingKey - Most investors aspire to "participate in upside gains while controlling drawdowns," yet often lack the proper tools and strategies to achieve this balance. In this context, derivatives—particularly options—are opening new avenues of thought for an increasing number of investors.

Among various combination strategies, the Bull Call Spread stands out as a classic structure that allows participation in upward price movements while capping both maximum risk and potential returns.

Simply put, by simultaneously buying a lower-strike call option and selling a higher-strike call option with the same expiration date, traders construct this strategic combination.

Compared to directly purchasing call options, this strategy requires lower capital outlay and inherently incorporates built-in "take-profit and stop-loss" characteristics. Consequently, many professional traders employ it to express moderately bullish views on underlying assets.

This article will guide you from foundational definitions to practical applications—from volatility impacts to time value management—providing a comprehensive analysis of this operationally valuable options tool.

(Source: Freepik)

What Is a Bull Call Spread?

A bull call spread is a common options trading strategy constructed by simultaneously buying and selling two call options with the same expiration date but different strike prices. This structure generates limited profits when the underlying stock price rises moderately.

Specifically, the strategy involves buying a lower-strike call option while simultaneously selling a higher-strike call option on the same underlying asset and with identical expiration dates. This combination qualifies as a vertical spread strategy, as both contracts share the same expiration date but feature staggered strike prices.

Since the lower-strike call option typically carries a higher premium than the higher-strike call, establishing this position requires paying a net premium. It is therefore also known as a "long call spread" or "debit call spread."

Investors typically deploy this strategy when anticipating moderate market upside. Compared to holding a standalone call option, it reduces initial costs while clearly defining maximum risk and profit potential.

This structure’s popularity stems from its ability to lower the barrier to participating in bullish markets while avoiding unlimited risk exposure. However, it imposes a profit ceiling: once the underlying asset’s price exceeds the strike price sold, further upside gains cease to accrue.

Learn more: "Limited Risk, Predictable Profit: Mastering Bull Put Spread Strategies – Concepts & Practical Applications"

Operational Mechanics of the Bull Call Spread Strategy

The bull call spread is executed by simultaneously buying and selling two call options with different strike prices but the same expiration date. This strategy suits market environments where the underlying asset is expected to appreciate moderately.

The specific implementation involves:

Buying a lower-strike call option (typically at-the-money or slightly in-the-money, near or marginally below the current market price)

Simultaneously selling a higher-strike call option with the same expiration date (typically out-of-the-money)

As the lower-strike call carries a higher premium than the higher-strike call, establishing this position requires paying a net premium, creating a "debit spread" structure.

The key advantage lies in the premium offset mechanism: the premium received from selling the higher-strike call directly reduces the net cost of buying the lower-strike call, thereby decreasing the investor’s initial capital commitment.

Profits materialize when the underlying asset’s price aligns with expectations. If the price rises above the lower strike, the bought call gains intrinsic value. Maximum profit is achieved when the price reaches or exceeds the higher strike price at expiration.

However, this structure automatically caps profit potential—regardless of how high the price climbs, maximum profit is strictly limited to the difference between the two strike prices minus the net premium paid.

Correspondingly, maximum risk is clearly defined: if the price fails to exceed the lower strike price at expiration, both options expire worthless, and the investor’s loss is limited to the initial net premium paid.

Case Study: Building a Bull Call Spread Strategy

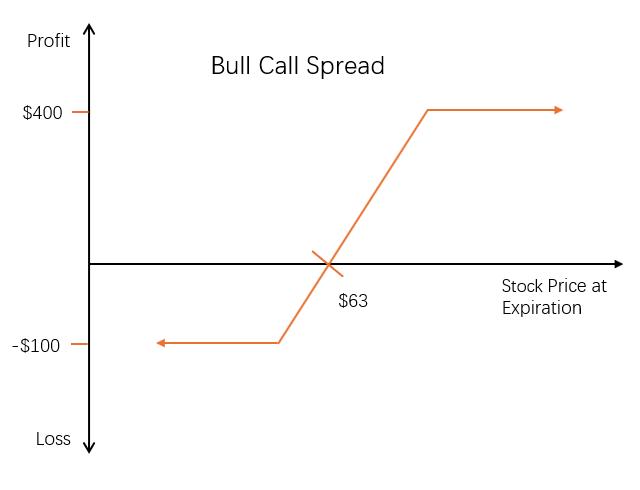

Suppose an investor believes a stock currently trading at $62 will experience moderate growth over the next month. They wish to profit from this potential modest upward movement through a risk-limited, cost-efficient approach. To achieve this objective, the investor decides to establish a bull call spread position.

Position Setup:

Buy one call option with a $62 strike price expiring in one month (paying $3.00 per share)—an at-the-money or near-the-money option

Simultaneously sell one call option with a $67 strike price and the same expiration date (receiving $2.00 per share)—an out-of-the-money call contract

Net debit = $3.00 − $2.00 = $1.00 per share

Since each standard contract represents 100 shares, total initial outlay = $1.00 × 100 = $100

Maximum Profit

Maximum profit = Higher strike price − Lower strike price − Net debit

= ($67 − $62) − $1 = $4.00 per share

Total maximum profit = $4.00 × 100 shares = $400

When the underlying stock closes at or above $67 on the expiration date, both contracts become in-the-money. However, any price movement beyond $67 generates no additional gains, capping the position's profit potential at $400.

Breakeven Point

Breakeven point = Long leg strike price + Net debit

= $62 + $1 = $63.00 per share

In other words, as long as the stock rises to at least $63 by expiration, the trade becomes profitable. If it closes exactly at $63, the position breaks even; prices below this level result in net losses.

Maximum Loss

The strategy's maximum loss equals the initial net debit—the fixed drawdown incurred when both legs expire worthless:

Maximum loss = Net debit

= $1.00 per share × 100-share contract size

= $100 total

This scenario occurs when the underlying asset's final price is at or below the bought call strike ($62), causing both call options to expire worthless. The total amount paid initially constitutes the entire risk exposure.

Impact of Stock Price Movements

In a bull call spread strategy, the position’s overall value increases as the underlying stock price rises and decreases as it falls. This indicates the strategy has a "net positive Delta"—exhibiting favorable responsiveness to upward price movements.

Delta is a critical metric measuring an option’s price sensitivity to changes in the underlying asset’s price. This ratio is typically less than 1:1 (e.g., a Delta of 0.6 implies a $1 stock price rise increases the option’s price by approximately $0.60).

Because the bull call spread combines a long lower-strike call and a short higher-strike call, their Deltas offset each other. With constant time to expiration, the strategy’s net Delta usually remains modestly positive without significant volatility.

In professional options terminology, this characteristic is described as having a "near-zero Gamma value." Gamma measures the rate at which Delta changes per unit movement in the underlying price. A low Gamma value means the strategy’s risk exposure won’t fluctuate dramatically with minor price movements.

This stable Delta profile offers traders significant advantages: in moderately bullish markets, the strategy continuously profits from rising prices while avoiding the extreme sensitivity shifts common in single-option positions.

When the stock price fluctuates between the two strike prices, the position maintains a relatively stable positive Delta, providing predictable profitability. As the price approaches or exceeds the higher strike, Delta gradually converges toward zero—naturally capping additional gains from further upside. This aligns perfectly with the strategy’s "limited profit" design principle.

Impact of Volatility Changes

Volatility measures the degree of price fluctuation in a stock over a specific period, typically expressed as a percentage. It is a key factor influencing option pricing. Holding other variables (e.g., underlying price, expiration time) constant, rising implied volatility generally increases option contract prices.

For the bull call spread strategy—which includes both a long call and a short call on the same underlying asset with identical expiration dates—the impact of implied volatility changes is largely offsetting. This results in minimal price reactions to volatility shifts for the overall position.

In professional options terminology, this is characterized as having a "near-zero Vega value." Vega, the Greek parameter measuring an option’s sensitivity to volatility changes, approaches zero in this strategy. This means dramatic volatility swings won’t significantly affect the position’s value.

Nevertheless, the strategy isn’t entirely immune to volatility shocks. Its ultimate performance may still be influenced by factors such as each leg’s moneyness (in-the-money/out-of-the-money status), remaining time to expiration, and actual trading slippage.

Impact of Time

In options pricing, time value continuously erodes as expiration approaches—a phenomenon known as "time decay" or "time erosion."

For the bull call spread—which consists of a long call and a short call—the position’s sensitivity to time passage depends on multiple factors. The most critical is the underlying stock price’s position relative to the two strike prices.

- When the stock price is near or below the lower strike price (long leg):

The position relies heavily on the long call’s expected profit potential. Here, the purchased call retains substantial time value and decays rapidly, while the short higher-strike call (deep out-of-the-money) depreciates slowly. Consequently, time decay negatively impacts the strategy.

- When the stock price is near or above the higher strike price (short leg):

Time decay becomes advantageous. The short call (closer to at-the-money) loses time value faster than the long call, causing the position’s value to rise as expiration nears.

- When the stock price sits between the two strikes:

Time value decay rates for both options balance each other, minimizing the impact of time erosion on the overall position.

(Source: Freepik)

Early Exercise Risk

In American-style options trading, short option holders face the risk of early exercise at any time. This characteristic imposes special considerations on strategies containing short positions (such as bull call spreads), as the short leg may be exercised by the counterparty before expiration.

For bull call spreads, the long call option carries no early exercise obligation, eliminating related concerns. However, the sold higher-strike call option faces potential early exercise risk.

If exercised, investors are forced to sell shares at the contract-specified price—even without owning the underlying asset—triggering additional trades and costs.

Early exercise most commonly occurs around ex-dividend dates. When an in-the-money call option’s (where current market price exceeds the strike) remaining time value falls below the expected dividend amount, counterparties often prioritize exercising the option. Thus, when the short leg of an investor’s position is in-the-money near an ex-dividend date, they must reassess the risk of early assignment.

Two approaches can address this situation:

- Close the entire spread: Simultaneously sell the long call and buy back the short call to fully exit the position, preventing any forced delivery events.

- Cover only the short leg: Retain the long call position while buying back the originally sold higher-strike call to unilaterally eliminate the exercise obligation.

If unaddressed and automatic exercise occurs without sufficient shares for delivery, a temporary short stock position is created in the account.

Expiration Risk

Holding a bull call spread to expiration introduces additional settlement risks—particularly when the underlying stock price hovers near the sold call option’s (short leg) strike price.

Since American options typically enter final settlement after Friday’s market close—with exercise instructions processed in batches over the weekend—institutional investors may not confirm assignment status until the following Monday. This uncertainty intensifies when the stock price sits slightly below, at, or marginally above the strike price.

Advantages of the Bull Call Spread Strategy

- Controlled Risk

Maximum potential loss is predefined as the net premium paid at initiation. Regardless of market volatility, the worst-case loss equals the initial net debit (the difference in premiums between the two strike prices), capping total capital exposure.

- Clear Profit Boundaries

With strike prices locked at entry, maximum profit can be precisely calculated before trading. This enables rational decision-making aligned with return objectives and risk-reward balance.

- Lower Capital Commitment

Compared to buying standalone calls, pairing a sold call offsets part of the purchase cost through premium collection. This significantly reduces net outlay, appealing to capital-constrained investors or those seeking efficient capital utilization.

Disadvantages of the Bull Call Spread Strategy

- Capped Profit Potential

When the underlying asset surges beyond the higher strike price, gains from additional upside are fully offset by the sold call. This limits returns during strong bull markets that might otherwise deliver higher profits.

- Reduced Returns vs. Single-Leg Trades

Due to offsetting positions, profit potential is inherently lower than holding an outright long call. Even with correct directional calls, investors must accept "trading total upside potential for reduced cost."

- Strong Path Dependency

Strategy performance heavily depends on the price path—not just the final outcome. If the stock first surges then retreats to between the strikes, time value erosion during interim volatility may reduce profits below theoretical expectations—even with a favorable expiration price.