TradingKey - In today’s derivatives market, put options serve not only as essential tools for building defensive positions but also as strategic vehicles for achieving profit objectives. The Bull Put Spread has evolved as a yield-oriented structured strategy that creates a risk-capped, marginally profitable position by simultaneously "selling a higher-strike put" and "buying a lower-strike put."

This strategy is particularly suitable for investors with a moderately bullish market outlook who seek to limit maximum losses while generating income through time decay or directional positioning. While avoiding single-directional trading risks, this structure also provides a more flexible framework for navigating varying volatility environments.

This article systematically analyzes the strategy’s definition, operational mechanics, profit/loss dynamics, and sensitivity to market variables (price movements, volatility shifts, and time to expiration). Through practical case studies, we further explore its advantages and potential risks, guiding investors to identify optimal timing for implementation and achieve stable speculation or advanced portfolio management objectives.

What Is a Bull Put Spread?

A Bull Put Spread is a risk-controlled, neutral-return options strategy that achieves maximum profit when the underlying asset price remains above the strike price of the sold put option at expiration.

This strategy is constructed by simultaneously selling a higher-strike put option and buying a lower-strike put option with the same expiration date. These two legs form a vertical spread combination that expresses bullish or neutral market views with lower margin requirements while capping potential losses within a defined range.

The sold higher-strike put generates premium income, while the purchased lower-strike put primarily serves as a hedge against exercise risk. Due to the strike price differential between the two options, investors always receive net premium income when establishing this position—hence the alternative names "credit put spread" or "short put spread."

Learn more: "A Rational Choice in Moderately Rising Markets: Understanding the Bull Call Spread Strategy"

(Source: Freepik)

Operational Mechanics of the Bull Put Spread Strategy

The Bull Put Spread strategy operates based on fundamental put option characteristics. In this approach, traders construct a position with clearly defined risk boundaries by simultaneously selling a higher-strike put option and buying a lower-strike put option.

When the underlying stock price reaches or exceeds the strike price of the sold put option (the higher-strike put) at expiration, both options expire worthless. The trader retains the full net premium, achieving maximum profit. Consequently, this strategy is ideal for investors anticipating modest price increases or expecting the underlying asset to remain at least at the higher strike price level. It provides a method to benefit from rising prices without physically holding the stock, while strictly controlling potential losses through structured design.

A key advantage of this strategy is the ability to earn limited profits from moderately rising markets without direct stock ownership, using a synthetic structure. Simultaneously, since premium income is collected during position establishment and the long leg establishes a risk "floor," downside losses are confined to a predetermined range. Maximum loss is calculated as the difference between the two strike prices minus the net credit received at initiation.

Although overall risk is controlled, investors retain the option to close positions early if market movements reverse sharply or approach unfavorable thresholds, avoiding additional costs from volatility.

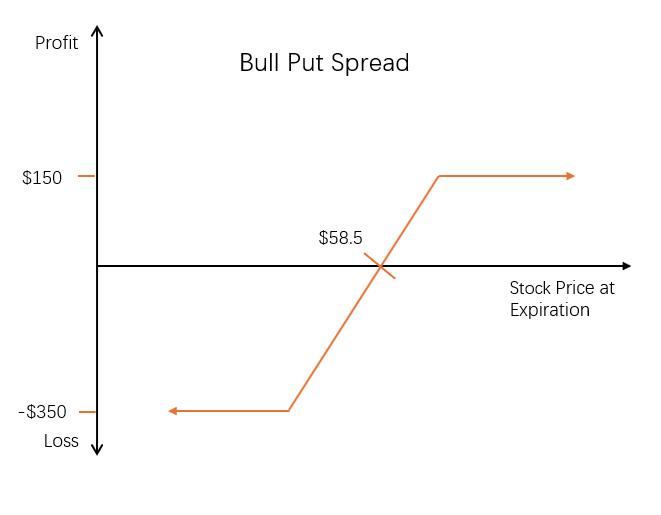

Case Study: Constructing a Bull Put Spread

Suppose an investor holds a moderately bullish view on a stock currently trading at $62. They believe the stock will maintain a range-bound or slightly upward trajectory over the coming weeks, with little likelihood of significant decline. To express this view while controlling potential drawdown risk, the investor elects to implement a Bull Put Spread strategy.

Specific position-building actions:

Sell one put option with a $60 strike price (receiving a $2.50 premium)

Simultaneously buy one put option with the same expiration date and a $55 strike price (paying a $1.00 premium)

Net credit = $2.50 − $1.00 = $1.50 per share

Each contract represents 100 shares, yielding a total net credit of $150.

Maximum Profit

Maximum profit = Net credit

= $1.50 per share × contract multiplier of 100 shares = $150 maximum profit

The strategy’s maximum profit equals the net credit received at initiation. When the underlying stock closes at or above $60 (the strike price of the sold leg) at expiration, both put options expire out-of-the-money and worthless. The investor retains the full $150 as final profit.

Notably, regardless of whether the stock price rises to $63, $70, or higher—as long as it remains above $60—both legs expire worthless, and no additional profits accrue beyond the $150 maximum.

Breakeven Point

Breakeven point = Sold put strike price − Net credit = $60 − $1.50 = $58.50

This means the position yields positive returns as long as the stock price at expiration is at or above $58.51. At exactly $58.50, the trade breaks even. Below this level, the position enters a minor loss zone.

Maximum Loss

Maximum loss = Difference between strike prices − Net credit received

= ($60 – $55) – $1.50 = $5 – $1.50 = $3.50 per share, totaling $350

In extreme scenarios where the underlying asset falls below $55—breaching the protective threshold set by the bought leg—the position triggers its maximum possible drawdown. However, losses remain strictly capped at $350 and cannot exceed this predetermined limit.

Impact of Stock Price Movements on the Strategy

The Bull Put Spread strategy generates profits when the underlying stock price rises and incurs losses when it falls, resulting in an overall positive Delta characteristic (i.e., positive net Delta). Delta reflects the rate at which an options portfolio's profit/loss changes in response to movements in the underlying asset price.

Since this strategy combines one sold put option and one bought put option, its overall net Delta value is small and remains relatively stable despite stock price fluctuations.

This insensitivity to Delta changes is commonly described as having a "Gamma value approaching zero." Gamma measures the rate of change in Delta per unit movement in the underlying price. Consequently, this position exhibits a mildly bullish yet stable directional bias.

Impact of Volatility Changes

Implied volatility is one of the most critical factors determining options pricing. When volatility rises while other conditions remain constant, most single-leg options positions benefit.

However, because the Bull Put Spread involves offsetting long and short positions, its sensitivity to volatility changes is low—its overall Vega value also approaches zero.

This means that in directionless volatile markets, even if short-term sentiment causes implied volatility estimates to spike, the structure itself experiences minimal valuation deviation, reducing interference from non-predicted factors for investors.

Impact of Time Value Decay

As expiration approaches, the time value component of option prices continuously deteriorates—a phenomenon known as "time decay" or the Theta effect.

The Bull Put Spread strategy includes both a sold and a bought put contract, so its sensitivity to time passage depends on the current position of the underlying stock price.

- When stock price is above the sold strike price

This scenario delivers optimal profitability. Both contracts trend toward expiration worthless while the seller retains the full premium, with the position gradually approaching its maximum profit ceiling.

Simultaneously, because the short leg is closer to at-the-money status, its value decays faster than the long leg, creating a favorable overall time effect.

- When stock price is between the two strike prices

Time decay impacts both legs relatively equally here. Neither contract expires worthless nor becomes deeply in-the-money, causing their Theta effects to largely offset each other. This results in relatively flat or consolidating P/L performance.

- When stock price approaches or falls below the lower strike price

This situation increases the probability of losses. The long leg becomes the dominant control factor and is more severely eroded by Theta, causing the entire position to move toward negative returns.

Nevertheless, the initial premium received from the short leg serves as a protective barrier, capping the maximum possible loss within predefined limits.

Early Exercise Risk

After establishing a Bull Put Spread position, investors must monitor the risk of early exercise on their short leg (the sold option), as this obligation represents an uncontrollable factor.

This situation typically occurs around ex-dividend dates. If a stock is about to issue cash dividends and a deep in-the-money put contract’s remaining time value falls below the dividend amount, the holder is more likely to exercise immediately to "beat" the official ex-dividend date. This forces the trader to unexpectedly hold a 100-share long position in the underlying asset (automatic stock purchase).

Although the lower strike portion (the bought leg) carries no similar risk, two common countermeasures prevent unintended inventory:

① Proactively close the entire position before the ex-dividend date (exiting the structure entirely);

② Close only the leg prone to early exercise risk (the short option) while retaining the protective long leg to maintain market exposure.

Notably, if the user’s account cannot provide overnight margin support for the required cash settlement, it may trigger margin calls. Inability to promptly liquidate the position could also raise regulatory capital alerts. Therefore, avoiding forced settlement arrangements should be a critical operational principle.

Additionally, corporate actions such as stock splits, secondary offerings, special dividends, or merger restructurings alter existing contract valuations—requiring adjustments like basis conversions or new standards. These events break traditional "early exercise probability" predictive models, necessitating close attention to announcement details and timely system alert tracking.

(Source: Freepik)

Advantages of the Bull Put Spread Strategy

- Controlled Risk

Since this strategy incorporates a protective long put option, maximum loss is clearly defined at initiation, calculated as the difference between the two strike prices minus the net premium received. This makes it a reliable choice for risk-averse traders.

- Locked-in Profits

When the underlying asset’s price at expiration is at or above the sold put option (the higher strike leg), both options expire worthless, retaining the full premium to achieve maximum profit = net credit—eliminating subsequent position uncertainty.

- Suitable for Gradual Bullish Markets

This structure particularly suits "moderately rising" or "range-bound with upside bias" market environments. It doesn’t require significant stock appreciation—only maintaining prices above a certain threshold to steadily capture predetermined returns.

Disadvantages of the Bull Put Spread Strategy

- Capped Profit Potential

Regardless of how sharply the underlying stock rises, this structure’s maximum profit equals only the net premium collected at initiation. If the stock surges powerfully, it cannot breach this pre-set profit ceiling, potentially missing larger gain opportunities.

- Downside Losses Still Possible

If markets abruptly turn bearish and prices fall below the long leg’s strike, the worst-case scenario triggers. Though losses remain limited, actual negative P/L occurs—demanding high operational discipline and making it unsuitable for frequent directional misjudgments.