TradingKey - In highly uncertain market environments, relying solely on short selling or buying puts often fails to balance risk management with return efficiency. For investors with a moderately bearish market outlook, a key consideration in strategy selection is how to reduce capital exposure risk while maintaining clear directional expectations.

The Bear Spread strategy emerged precisely to meet this need. As a common "vertical spread" structure in options trading, it combines the purchase and sale of same-type options with consistent directional bias but different strike prices, precisely defining both profit potential and loss boundaries.

Whether constructed as a bear put spread (buying a put option while selling a lower-strike put) or a bear call spread (selling a near-the-money call while simultaneously buying a higher-strike call), this strategy provides stable returns during moderate market declines while avoiding significant losses from extreme market movements.

This article will systematically explain the core principles, profit/loss characteristics, applicable scenarios, and practical implementation examples of bear spread strategies, helping investors effectively understand and apply this classic yet practical derivatives tool to maintain initiative in future volatile or bearish markets.

(Source: Shutterstock)

What Is a Bear Spread?

A bear spread is a directional options strategy designed for investors with a moderately bearish market outlook. Its objective is to profit when the underlying asset price declines, while simultaneously controlling potential risk and capital commitment. This strategy constructs a "limited profit, limited loss" trading structure by simultaneously buying and selling options of the same type (either calls or puts).

Typically, these options share the same underlying asset and expiration date but have different strike prices, classifying them as a type of "vertical spread" strategy.

In simple terms, this strategy sacrifices potential excessive profits in extreme market movements to gain more defined risk boundaries and lower capital requirements—a relatively conservative, risk-controlled approach to shorting the market.

Bear spreads come in two types:

- Bear Put Spread

- Bear Call Spread

Both combinations are designed for scenarios where the market may experience moderate downward movement or weakening sideways trends, with each having distinct emphases under different market expectations.

Item | Bear Put Spread | Bear Call Spread |

Option Type Used | Put Options | Call Options |

Execution Method | Buy higher-strike Put + Sell lower-strike Put | Sell lower-strike Call + Buy higher-strike Call |

Net Cost at Entry | Net debit → Debit Spread | Net credit → Credit Spread |

Maximum Profit | Difference between strike prices - Net premium paid | Net premium received |

Maximum Loss | Net premium paid | Difference between strike prices - Net premium received |

Applicable Market Outlook | Clearly bearish / Expecting moderate decline | Bearish to neutral / Expecting sideways-to-weak trend |

Bear Put Spread

The bear put spread is a vertical spread strategy suitable for scenarios with moderately bearish market expectations. This strategy is constructed by purchasing a higher-strike put option (Long Put) while simultaneously selling a lower-strike put option (Short Put) with the same expiration date, making it a debit strategy. It is widely applied by investors seeking to profit from downward price movements in underlying assets while controlling risk capital expenditure.

The core positioning of this strategy is for situations where investors anticipate a decline in the underlying asset's price, but with limited magnitude. It captures downside profits at a controlled cost while sacrificing potential excess profits from extreme downward movements in exchange for clearly defined risk boundaries.

Constructing a bear put spread requires adherence to specific operational rules:

- Buy one higher-strike put option (typically near or slightly below the current market price) as the primary downside protection

- Sell one put option with the same expiration date but a lower strike price to offset part of the premium cost

- Net cash flow direction: Since the higher-strike put option carries a higher premium, a net premium payment is required at position initiation, hence the term "debit spread"

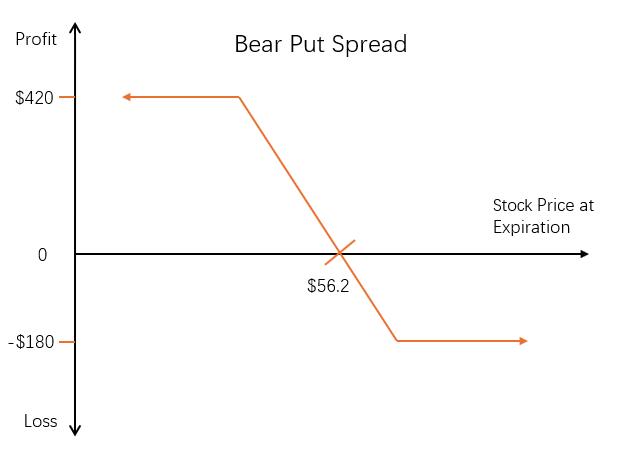

Case Study: Building a Bear Put Spread Strategy

Suppose an investor holds a moderately bearish view on a stock currently trading at $60. They believe the stock will gradually decline over the coming weeks but is unlikely to crash to significantly lower levels. To express this view while controlling risk and costs, the investor chooses to employ a bear put spread strategy.

The investor's actions are as follows:

Buy one put option with a $58 strike price (paying a $3.00 premium)

Sell one put option with a $52 strike price but the same expiration date (receiving a $1.20 premium)

Strategy net cost = $3.00 – $1.20 = $1.80 per share

With each contract representing 100 shares of stock, the total position cost is $180.

Profit/Loss Analysis:

Breakeven point = Long strike price − Net cost = $58 − $1.80 = $56.20

If the underlying stock price equals $56.20 at expiration, the strategy breaks even.

Maximum profit = Difference between strike prices − Net cost

= ($58 − $52) − $1.80 = $6 − $1.80 = $4.20 per share → Total $420

Maximum profit is achieved when the underlying asset's price at expiration is ≤ $52, as both contracts will be in the money.

Maximum loss = Initial net investment, or $1.80 per share ($180 total)

If the stock price at expiration is ≥ $58, both contracts will expire worthless, resulting in a total loss of the initial outlay.

Time Value and Volatility Impact

The long option in a bear put spread suffers negative effects from "time decay" (theta) as time passes. If the market prediction is correct, the trader hopes for a quick price decline to lock in profits early, making the optimal outcome occur shortly after position entry with a significant price drop.

Simultaneously, since put options are highly sensitive to rising implied volatility, this strategy typically benefits from volatility increases. However, incorrect volatility forecasts or sustained market consolidation may cause the position to lose value.

Additionally, as the underlying asset price falls, the strategy's Delta (directional sensitivity) gradually moves from negative toward zero, losing further downside sensitivity after reaching maximum profit.

Bear Call Spread

The bear call spread strategy constructs a limited-risk, limited-reward short position by selling a near-the-money (lower strike) call option while simultaneously buying a higher-strike call option with the same expiration date, generating net premium income.

Since the lower-strike option carries a higher premium, this operation creates net cash inflow at position initiation, earning it the name "credit spread."

Implementation of Bear Call Spread:

- Sell one near-the-money or slightly out-of-the-money lower-strike call option (e.g., with current stock price at $50, select a $48 strike price)

- Buy one higher-strike call option (e.g., $53 strike price) as risk-control insurance

- Net cash flow: Receive net premium at entry, creating initial profit potential

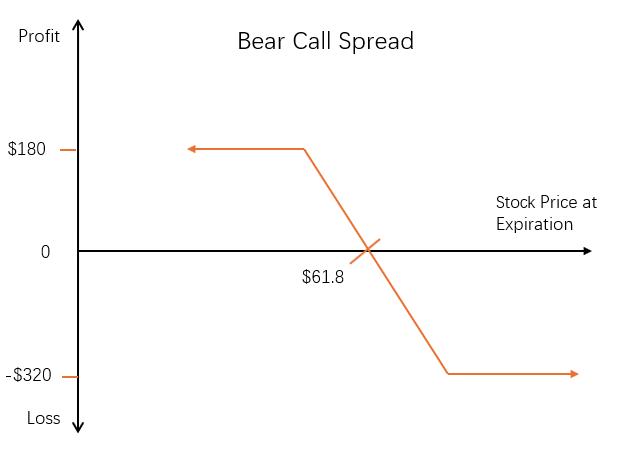

Case Study: Building a Bear Call Spread Strategy

Similarly, suppose an investor holds a moderately bearish view on a stock trading at $60. They believe the stock won't rise significantly in the coming weeks and may instead decline or remain range-bound. The investor therefore selects a bear call spread strategy to profit from the absence of upward price movement while maintaining controlled risk.

The investor takes the following actions:

Sells one call option with a $60 strike price (receiving a $3.00 premium)

Simultaneously buys one call option with a $65 strike price and the same expiration date (paying a $1.20 premium)

Strategy net credit = $3.00 – $1.20 = $1.80 per share

With each contract representing 100 shares, the total position credit is $180.

Profit/Loss Analysis:

Breakeven point = Sold strike price + Net credit = $60 + $1.80 = $61.80

If the underlying price equals $61.80 at expiration, the strategy breaks even.

Maximum profit = Net credit received, or $1.80 per share → Total $180

Maximum profit occurs when the underlying price at expiration is ≤ $60, causing both contracts to expire worthless.

Maximum loss = Difference between strike prices − Net credit

= ($65 − $60) − $1.80 = $5 − $1.80 = $3.20 per share → Total loss $320

If the underlying price ≥ $65 at expiration, both calls will be exercised, resulting in maximum loss.

This strategy achieves maximum profit when the trader correctly predicts the underlying price will remain below the lower strike price (sold call) at expiration—the profit equals the net credit collected at initiation. Therefore, the optimal market forecast for this strategy is "moderately bearish" or "lacking upward momentum."

Simultaneously, if the stock price eventually rises above the higher strike price (bought call), maximum loss occurs. However, the upside risk is capped at the difference between the two strike prices minus the premium received. This clearly defined structural return range represents a key advantage of the strategy.

However, as a typical American-style stock option structure, this strategy faces the risk of early assignment on the short position. Short calls are more likely to be exercised early, particularly before ex-dividend dates when time value cannot offset dividend incentives.

Time Value Decay Effect

As expiration approaches, all options without exercise value or intrinsic value support experience time value erosion—the "Theta decay" process.

The bear call spread, as a credit structure, benefits positively from this natural deterioration caused by time passage, exhibiting an overall "positive Theta" profile.

Nevertheless, whether this time decay proves beneficial depends on the current stock price relative to the two strike prices:

If the market price remains below the sold call strike, the short call approaches at-the-money status and rapidly loses value, while the long higher-strike call remains out-of-the-money → strategy gains maximum positive benefit

If the underlying price approaches or exceeds the higher strike call position, the long call becomes near-the-money and depreciates faster than the short call → potentially causing net losses

If the price settles between the two strikes, both sides decay at similar rates, resulting in stable but directionally neutral P/L performance during this phase

Therefore, incorporating time as a factor in both position construction and exit decisions represents a critical risk management consideration for this strategy.

Stock Price Movement and Volatility Impact

The bear call spread strategy generates profits when the underlying stock price declines and may incur losses when the price rises. The strategy exhibits an overall negative Delta profile, meaning it maintains short sensitivity to price direction changes.

Delta measures an option's price responsiveness to underlying asset price movements, typically at less than a 1:1 ratio. In this combination, selling a near-the-money (ATM) call option while buying a higher-strike (OTM) call option creates offsetting directional exposures, resulting in a net negative Delta for the entire position.

Additionally, this strategy consists of options with the same expiration date and similar Delta characteristics. Under volatility changes, it demonstrates near-zero Vega exposure—meaning minor market volatility fluctuations have limited impact on the entire position since both sides adjust prices synchronously.

However, it's worth noting that establishing positions when implied volatility is relatively high helps lock in richer premiums for risk protection. Furthermore, if IV subsequently drops rapidly, it can enhance closing position profit potential.

Advantages and Disadvantages of Bear Spread Strategies

Compared to directly buying or selling single options, bear spreads create a structured approach to risk and cost control by combining two same-type options with different strike prices but identical expiration dates. Nevertheless, this strategy has inherent limitations.

Advantages

- Capped Maximum Loss

By constructing a buy/sell option combination, the strategy's maximum risk is locked at position initiation, enhancing capital management efficiency.

- Reduced Single-Leg Operation Costs

Whether offsetting put purchase costs by selling lower-strike puts (bear put spread) or hedging higher-strike call purchases with call premium income (bear call spread), initial capital requirements are effectively compressed.

- Suitable for Moderately Volatile or Slight Pullback Markets

When markets lack extreme trends and only show narrow fluctuations or technical corrections, this strategy can deliver better risk/reward ratios than directional single-leg positions.

- Appropriate for Intermediate Traders as an Advanced Risk Control Tool

With clear methodology and controllable structure, this represents an important educational stepping stone between naked single-leg positions and sophisticated multi-leg combinations.

Disadvantages

- Limited Profit Potential

Since one position leg serves to limit risk, it simultaneously caps profit potential. When markets experience unexpectedly sharp declines, the strategy cannot capture the full extent of potential gains.

- Requires Precise Assessment of Both "Magnitude" and "Direction"

Ideal returns occur only when the underlying price settles between the two strike prices or on the bearish side. Even with correct directional prediction, inaccurate magnitude assessment can lead to limited profits or losses.

- Early Exercise Risk with American-Style Options (Especially Bear Call Spreads)

Particularly with dividend-paying assets, short call positions may trigger early exercise around ex-dividend dates. Investors must monitor calendar events and evaluate technical details like liquidity and margin requirements.