Tesla Q1 Profit Beats Wall Street Expectations, Musk’s $25 Billion Capital Expenditure Plan Cools Market

AI Podcast

Tesla's Q1 2026 earnings surpassed profit expectations but revenue slightly missed. Free cash flow was a highlight, doubling year-over-year. Automotive revenue rebounded, yet EV deliveries showed a notable slowdown. Energy generation and storage revenue declined, contrasting with strong growth in Services and Other, driven by a surge in FSD subscriptions. Management announced increased capital expenditures for the year, exceeding prior guidance, which triggered market concerns about payback periods and led to stock volatility. Preparations for Optimus robot mass production are accelerating.

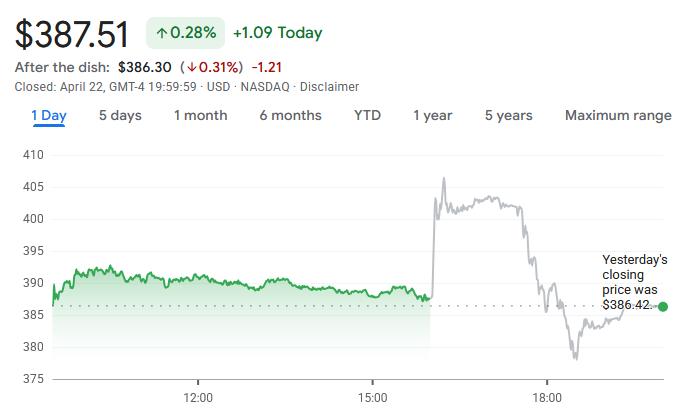

TradingKey - Tesla ( TSLA )'s first-quarter 2026 earnings report, released after the market close on April 22 Eastern Time, provided a brief lift to its recently sluggish stock price, but subsequently triggered market concerns regarding capital expenditure plans.

The report showed total revenue for the quarter reached $22.39 billion, up 16% year-over-year. While slightly missing the market expectation of $22.64 billion, profitability far exceeded expectations. GAAP net income was $477 million, a 17% year-over-year increase; non-GAAP adjusted net income soared 56% to $1.453 billion, with adjusted earnings per share of $0.41, roughly 11% above analyst forecasts.

Free cash flow was a particular highlight; while the market had expected it to turn negative, it actually recorded a positive $1.44 billion, doubling from a year earlier.

By business segment, the automotive business remained the primary revenue base, with quarterly revenue of $16.234 billion, up 16% year-over-year, reversing the 10% decline from the fourth quarter of last year. Energy generation and storage, however, became a drag, with revenue falling 12% to $2.408 billion—a sharp contrast to its 25% growth in Q4. Services and other segments were the standout performers, with revenue growing 42% to $3.745 billion, serving as the main engine of growth this quarter compared to 18% growth in the previous quarter.

Boosted by the double beat in earnings and cash flow, Tesla's stock rose more than 4% in after-hours trading. However, during the subsequent earnings call, management revealed that capital expenditures for the year would exceed $25 billion, a $5 billion increase from the previous $20 billion guidance. Following this news, the stock quickly surrendered its gains and fell more than 2%. Year-to-date, Tesla's stock has fallen by nearly 14%.

The market is focused on when these high-level investments will translate into actual profits. In the short term, the significant ramp-up in capital expenditure suggests a longer payback period, which is the primary reason for investors adjusting their expectations and the resulting stock price volatility.

Automotive business slowdown

Based on Tesla’s first-quarter automotive performance, the company delivered 358,000 electric vehicles globally, a 6.3% year-over-year increase. Despite achieving sequential growth, this marked the second-worst quarterly sales performance since 2022. Wedbush Securities analyst Daniel (Dan) Ives called it a "disappointing start," though from a cumulative delivery perspective, Tesla’s global total has surpassed 9.2 million units, up 21% year-over-year.

In terms of product mix, the Model 3 and Model Y remain the primary sales drivers. Combined production for the two models in the first quarter reached 394,600 units, while deliveries totaled 341,900 units, representing year-over-year growth of 14% and 6%, respectively.

In contrast, other models—including the Cybertruck, Model S, and Model X—showed divergent performance. Production fell 20% year-over-year to 13,800 units, while deliveries rose 25% to 16,100 units. This discrepancy arose because Tesla officially ceased production of the Model S and Model X in January; original production lines at the Fremont factory are being retooled into Optimus humanoid robot lines, meaning most vehicles currently in circulation are inventory units.

The Cybertruck’s market performance has been more nuanced. Although its annualized production capacity has surpassed 125,000 units, market acceptance has lagged expectations. To absorb capacity, Tesla has begun selling the Cybertruck to other Musk-affiliated companies. Simultaneously, Tesla is advancing mass production of new models; the first Cybercab rolled off the line at the Texas Gigafactory in February, and the company plans to achieve mass production of both the Cybercab and the all-electric Semi truck by 2026.

Alarmingly, inventory pressure continues to climb. At the end of the first quarter, global days of supply reached 27 days, a significant increase from 22 days a year ago and 15 days in the previous quarter.

The gap between production and deliveries has exceeded 50,000 units, a discrepancy almost entirely concentrated in the Model 3/Y segment. This both reflects an accumulation of channel inventory and suggests that end-market demand is under pressure.

Short-term volatility in energy business

Tesla's energy business experienced rare volatility in the first quarter of 2026, with the energy generation and storage segment generating revenue of $2.408 billion, a 12% year-over-year decline; energy storage deployments reached 8.8 GWh, down 15% year-over-year and dropping sharply by 38% from the historical peak of the previous quarter.

In fact, the energy business is significantly influenced by project recognition cycles and delivery schedules, and quarterly performance fluctuations are standard in the industry. The market should focus more on mid-to-long-term signals from its production capacity layout and product iterations.

On the capacity side, construction continues on Tesla's new Gigafactory near Houston, which will specifically produce Megapack 3 storage units for Megablock energy storage systems, with production scheduled to begin in late 2026. Meanwhile, the Megapack factory in Shanghai, with an annual capacity of 20 GWh, is also under construction, which will further enhance global energy storage supply capabilities in the future.

Regarding products, Tesla has begun large-scale deliveries of its next-generation solar panels developed independently at the New York Gigafactory. This innovative product features 18 independent power generation zones—triple the number of traditional residential panels—ensuring stable and efficient power output even when partially shaded. Furthermore, the new product offers improved aesthetics and a more streamlined installation process, with its core advantages centered on the dual enhancement of shade resistance and installation efficiency.

Despite short-term performance pressures, Tesla's long-term strategy in the energy sector remains steadfast. Once energy storage demand rebounds, the potential for gross margin contribution from this business remains highly promising.

At the same time, the expansion of Tesla's Supercharger network has not slowed, with a net increase of over 2,200 stalls in the first quarter. The global number of Supercharger stations reached 8,463, while the total number of stalls surpassed 79,918, both representing a 19% year-over-year increase.

FSD Subscriptions Surge

The Services and Other segment performed particularly well, with revenue surging 42% year-over-year. A breakdown of the profit structure reveals a significant improvement in the gross margin of the services business; the growth rate of costs was far lower than that of revenue, making it a key driver of the company's overall gross margin increase.

At the core operational level, Tesla's autonomous driving and AI businesses are progressing rapidly. The number of FSD (Full Self-Driving) subscribers has reached 1.28 million, representing a 51% year-over-year increase and a nearly 16% quarter-over-quarter gain.

In April this year, FSD (Supervised) received official approval in the Netherlands, paving the way for its rollout in more EU countries. Meanwhile, Tesla is gradually transitioning FSD toward a "subscription-only" model to enhance recurring revenue and user penetration.

As of the end of the first quarter, cumulative FSD mileage has surpassed 17.7 billion kilometers, with V12 and subsequent versions contributing approximately 14.5 billion kilometers of driving data.

The Robotaxi business is also accelerating its expansion, with paid mileage nearly doubling quarter-over-quarter in Q1, reaching a cumulative total of over 2.74 million kilometers. In April, Tesla expanded its unsupervised Robotaxi service to Dallas and Houston while increasing the scope of unsupervised operations in the Austin area. Several other U.S. cities, including Phoenix and Miami, are preparing to launch the service, while a ride-hailing service equipped with safety drivers is simultaneously operating in the San Francisco Bay Area.

For capital markets, the large-scale commercialization of Robotaxi is of significant importance. Once it moves from small-scale pilots to a replicable business operation, Tesla's profit model will shift from traditional "hardware gross margin" to a compounded growth model of "fleet operations + software services." The impact of this shift on the company's valuation far outweighs short-term delivery data.

Optimus Preparations Accelerate

Tesla is accelerating the mass production rollout of its Optimus humanoid robot, with its manufacturing footprint and strategic transformation moves drawing significant market attention.

In January this year, Tesla announced it would discontinue its Model S and Model X luxury models to repurpose the existing production lines at its Fremont, California plant into a manufacturing base for Optimus. According to the latest disclosures, preparations for the first large-scale Optimus factory will officially begin in the second quarter; this first-generation line is designed for an annual output of 1 million robots, with trial production expected to start in late July or August 2026.

Meanwhile, Tesla is planning a more extensive capacity layout near its Texas Gigafactory, preparing for a second-generation Optimus production line with a long-term designed annual capacity of up to 10 million units, expected to enter production in 2027. In its first-quarter investor presentation, Tesla showcased vast tracts of land adjacent to the Texas plant, outlining its strategy for the deployment of the second-generation Optimus lines.

Elon Musk has consistently sought to shift the perception of Tesla away from being a traditional automaker by betting on autonomous driving and humanoid robot technology. While Tesla still largely depends on electric vehicle sales for its revenue and the Robotaxi is currently undergoing only limited testing in Texas, the move to phase out flagship models in favor of robot production lines signals a clear strategic pivot.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.