Unveiling U.S. Stock “Money Printing Machines” — Insights Into the Business Essence of Star Stocks From Net Profit Margins

AI Podcast

Net profit margin is identified as the core metric for evaluating U.S. stock quality, surpassing revenue scale and stock price gains. The S&P 500's Q4 2025 net profit margin of 13.2% serves as a benchmark. Companies like Tesla and Amazon exhibit low margins due to competition and capital intensity, relying on future growth. Conversely, Visa and NVIDIA demonstrate superior profitability through asset-light models and monopoly positions, respectively. Apple showcases steady margin expansion via its ecosystem. However, high profits can attract challengers, with Microsoft, Broadcom, and Adobe facing risks from capital expenditure and customer in-house development.

In the long-term valuation framework of the U.S. stock market, revenue scale and stock price gains are often "smoke screens" that attract retail investors. However, for institutional and value investors, there is only one core metric that can cut through market noise and measure the true quality of a business model: Net profit margin. It represents the proportion of every $100 in revenue that ultimately translates into shareholder wealth after deducting all costs, taxes, and expenses.

As the monetary environment of the U.S. stock market enters a new normal of neutral-to-tight policy and liquidity premiums return to rationality, simple "growth stories" can no longer sustain valuations. This article will use net profit margin as a "yardstick" to conduct a deep dive into representative companies such as NVIDIA, Tesla, Apple, and Visa to explore who the real money-printing machines of the capital markets are and who is struggling under the weight of flashy revenue data.

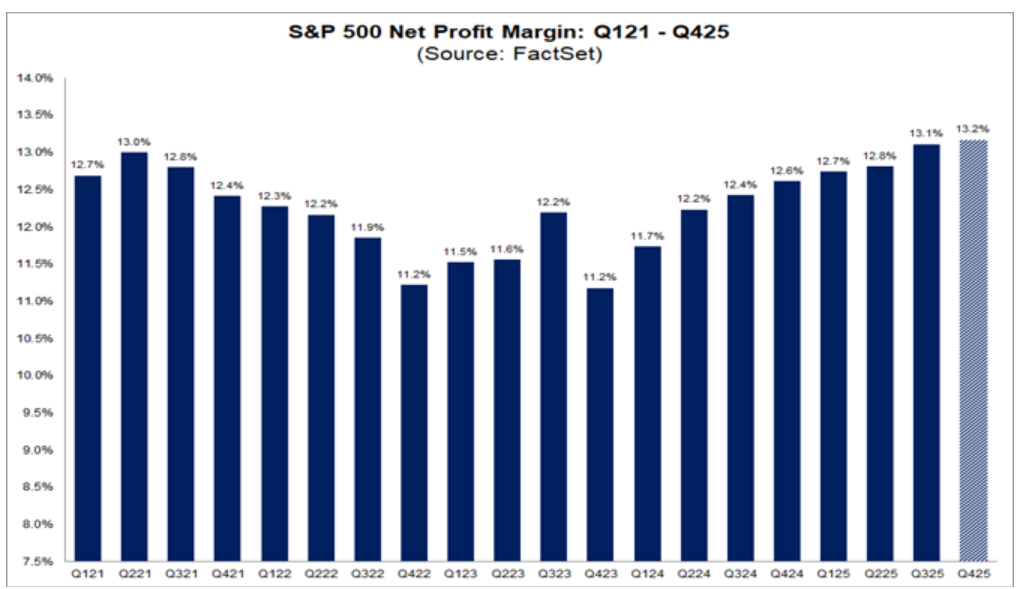

I. 13.2%: The "Passing Grade" for Excellence in U.S. Stocks

To evaluate a company's earnings efficiency, one must first establish an industry benchmark. According to the latest data from FactSet, the overall net profit margin for the S&P 500 index reached 13.2% in the fourth quarter of 2025.

Source: FactSet

This figure is a significant milestone; it not only marks a 16-year high since 2009 but also reflects the collective strengthening of cost control and pricing power among leading U.S. companies. Market analysts generally expect that as AI technology further unleashes productivity, this figure could rise to 13.9% by 2026. Therefore, 13.2% constitutes a survival "passing grade" for outstanding U.S. companies. In the current interest rate plateau, if a company's profit margin remains consistently below this standard, it means its earnings efficiency fails to even outperform the market average, and its resilience will face severe tests during economic cycles.

II. The Earnings Paradox of Star Stocks: The Scale Dilemma of Tesla and Amazon

Among high-profile tickers, Tesla (TSLA) and Amazon (AMZN) show a clear lack of earnings efficiency, reflecting the disadvantage of capital-intensive or highly competitive industries in profit distribution.

1. Tesla: A Valuation Gamble from 15.5% to 4.0%

Tesla's net profit margin at the end of 2025 was alarming at just 4.0%, less than a third of the S&P 500's passing grade. Looking back at 2022, Tesla's margin once reached 15.5%; in just three years, its profit space has shrunk by approximately 75%. The core reason for this sharp decline lies in frequent price cuts caused by intensifying competition in the global EV market, as well as capital depreciation pressure from massive production expansion.

Nevertheless, the market still awards it a P/E ratio exceeding 300, which is essentially a bet on its future business model transformation. Investors are not buying its current hardware profits but are betting on FSD (Full Self-Driving) and Robotaxi. Currently, FSD has approximately 1.1 million paying users. Although the current annualized revenue scale is relatively small, the gross margin of its software licensing business is typically above 80%. Tesla's logic is a classic case of " hardware paving the way, software reaping the rewards ", and if the software business does not achieve explosive growth as a percentage of revenue, its 4% margin will struggle to support its valuation as a tech giant.

2. Amazon: The "Double Persona" of the Revenue King

As a revenue giant in the U.S. stock market, Amazon's annual revenue has exceeded $710 billion, yet its overall net profit margin consistently hovers around 11%, failing to cross the 13.2% benchmark.

A deep dive into its financial structure reveals that Amazon is driven by two starkly different business logics:

- Retail Business: Margins are razor-thin, only 2%-3%. Its essence relies on an extremely high asset turnover rate—earning returns by cycling every dollar multiple times a year through efficient logistics.

- AWS Cloud Services: The operating profit margin for the cloud computing business has long remained above 30%, contributing the vast majority of the group's operating profit.

Amazon's case proves that a low profit margin is not synonymous with a lack of investment value, but it dictates that the company must maintain extremely high revenue growth and market share. Once growth slows, the slim margins make its stock price highly susceptible to volatility in a "neutral-to-tight" monetary environment.

III. Ultimate Profit Models: The "Asset-Light" Dimensionality Reduction Strike of Visa and NVIDIA

Unlike the aforementioned companies struggling to sell hardware and manage logistics, Visa (V) and NVIDIA (NVDA) demonstrate what a true "money-printing machine" looks like.

1. Visa: The "Toll Road" Logic of Global Payment Networks

Visa's annual revenue is approximately $41.4 billion—less than half of Tesla's scale—yet its net profit margin is as high as 50.23%. This means Visa has almost no substantial marginal costs: it carries no credit risk (banks bear that), requires no inventory, and needs no massive fleet. As the maintainer of global payment infrastructure, Visa collects a "toll" on every transaction. This business model, built on global network effects, enables its profitability to reach 3.8 times the S&P 500 benchmark.

2. NVIDIA: Monopoly Pricing of an Exclusive Pass

NVIDIA's performance in 2025 redefined perceptions of the semiconductor industry. Its annual revenue soared to $215.9 billion, while its net profit margin reached a staggering 55.6%. Maintaining over 50% net profit at such a massive scale is extremely rare in industrial history.

NVIDIA's moat is no longer just the AI chips themselves but its monopoly position built on the CUDA ecosystem. When giants like Microsoft, Google, and Meta purchase GPUs regardless of cost, NVIDIA wields absolute pricing power. Its 55.6% margin reflects an extreme supply-demand mismatch: in the AI arms race, it is the sole premier arms dealer.

IV. A Model of Steady Growth: Apple's Ecosystem Stickiness

Apple Inc. (AAPL) 's path represents another kind of success: steady expansion of profit margins. Rising from 21% in 2020 to the current 27%, this consistently upward curve is more imposing than short-term high profits.

By using the iPhone as an entry point, Apple has built a closed-loop ecosystem including iCloud, the App Store, and Apple Music. This layered lock-in effect significantly increases user switching costs, allowing the company to drive margins by raising prices or increasing service fees even in a saturated smartphone market. A consistently rising margin report is the best testimony to a company's increasing control over its customers.

V. Concerns Behind High Profits: Capital Expenditure and the Threat of Customer In-house Development

High profit margins often attract challengers and can even make customers uneasy.

- Microsoft (MSFT) : While possessing an excellent profit margin of 39.04%, the surge in its capital expenditure (CapEx) cannot be ignored. Projected CapEx for fiscal year 2026 is expected to reach $145 billion. If AI subscription conversion rates for enterprise customers fall short of expectations, massive depreciation and amortization will quickly erode this 39% margin.

- Broadcom (AVGO): Net profit margin remains around 37%, with a $73 billion order backlog. However, its risk lies in high customer concentration; the primary motivation for giants like Google to accelerate in-house chip development is to escape the high profit margins paid to Broadcom.

- Adobe (ADBE): A profit margin of approximately 29.5% is facing a generational challenge from AI. The traditional "pay-per-seat" model may face a collapse of its business logic as AI increases individual output and reduces the need for designers.

In summary, net profit margin is not just a financial metric but a quantitative reflection of a company's pricing power. Against a backdrop of neutral-to-tight interest rates and intensified market volatility, companies with high net margins possess a thicker "safety cushion." When inflation rises or demand shrinks, companies like Visa, NVIDIA, and Apple have the ability to survive by passing on costs or leveraging their monopoly positions; companies with margins below the 13.2% passing grade have a very low margin for error. For investors, it comes back to a common-sense evaluation: Does this company have the confidence to raise prices without losing customers? Only companies with such confidence can continue to serve as a non-stop money-printing machine through the changing cycles.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.