Tesla (TSLA) 2026 Deep Dive Report: Behind the 5x Pricing Divergence, a Sunset Automaker or AI Giant?

AI Podcast

Tesla faces polarized market views, debated as a carmaker versus an AI/robotics leader, with a $750 billion valuation premium linked to AI potential like Cybercab and FSD data moat. The AI platform transition, with FSD accumulating 8.4 billion miles, and Robotaxi subscription model, offer high-margin revenue. Core business shows margin recovery to 20.1% and energy storage growth. However, auto sales declined in 2025, facing BYD competition. High interest rates and regulatory hurdles for autonomous driving pose risks, alongside significant 2026 CapEx. Key 2026 milestones include Cybercab production, regulatory approval, margin maintenance, and Optimus robot ramp-up.

Source: TradingView

In the current global capital markets, Tesla (TSLA) is at an unprecedented crossroads. Top Wall Street investment banks have produced extremely polarized target price forecasts: the most optimistic analysts see it as high as $600, while the most pessimistic prediction is a mere $119. This fivefold pricing disparity is extremely rare among S&P 500 components, essentially reflecting a fundamental debate in the market over Tesla’s underlying logic: Is the company a traditional hardware manufacturing factory with stalling growth momentum, or an AI and robotics giant on the verge of explosive growth?

Source: TickerNerd

The core of this controversy lies in a valuation premium of approximately $750 billion. If looking strictly at delivery data, Tesla has experienced a growth slowdown or even a decline for two consecutive years; however, if one examines its 8.4 billion miles of autonomous driving training data and the Cybercab, which is set to enter mass production in April 2026, its valuation model will completely deviate from the framework of the traditional automotive manufacturing industry.

AI Transformation: Data Moat and the Robotaxi Business Loop

Tesla’s current valuation logic is undergoing a paradigm shift from "automotive manufacturing" to an "AI robotics platform." Morgan Stanley, in an in-depth report released on March 18, 2026, officially defined Tesla as an AI platform company. The core catalyst for this transformation is the Cybercab, which is set to begin mass production in April. This model eliminates the traditional steering wheel and pedals, marking another leap in Tesla’s vertical integration of manufacturing processes. Through innovative manufacturing techniques, Tesla expects to compress the cost per Cybercab to an industry-disrupting level and plans to rapidly expand this business to seven core cities in the United States in the first half of 2026.

In the field of autonomous driving, data volume is the only moat that determines victory. To date, the cumulative mileage of Tesla's Full Self-Driving (FSD) has exceeded 8.4 billion miles, a figure 42 times that of competitor Waymo (approximately 200 million fully driverless miles). While there are differences in the definition of driving automation between the two, from the perspective of AI neural network training, Tesla’s massive data covering complex global road conditions, weather, and driving habits constitutes an insurmountable barrier. FSD version 14 recently won MotorTrend's 2026 Driver Assistance System of the Year award, further validating its technical leadership.

From a financial perspective, the deployment of Robotaxi will enable Tesla to transition its profit model from "hardware sales" to "high-margin software subscriptions." Currently, FSD subscribers have reached 1.1 million. Since fully transitioning to a subscription model (monthly fees of $99 to $199) in February 2026, this business alone can generate $1.3 billion to $2.6 billion in high-margin revenue annually. Bank of America (BofA) assesses the potential value of the Robotaxi business at as much as $750 billion, accounting for about 52% of Tesla's total market capitalization.

Source: Tesla

Financial Fundamentals: Margin Recovery and Energy Business’s Second Growth Curve

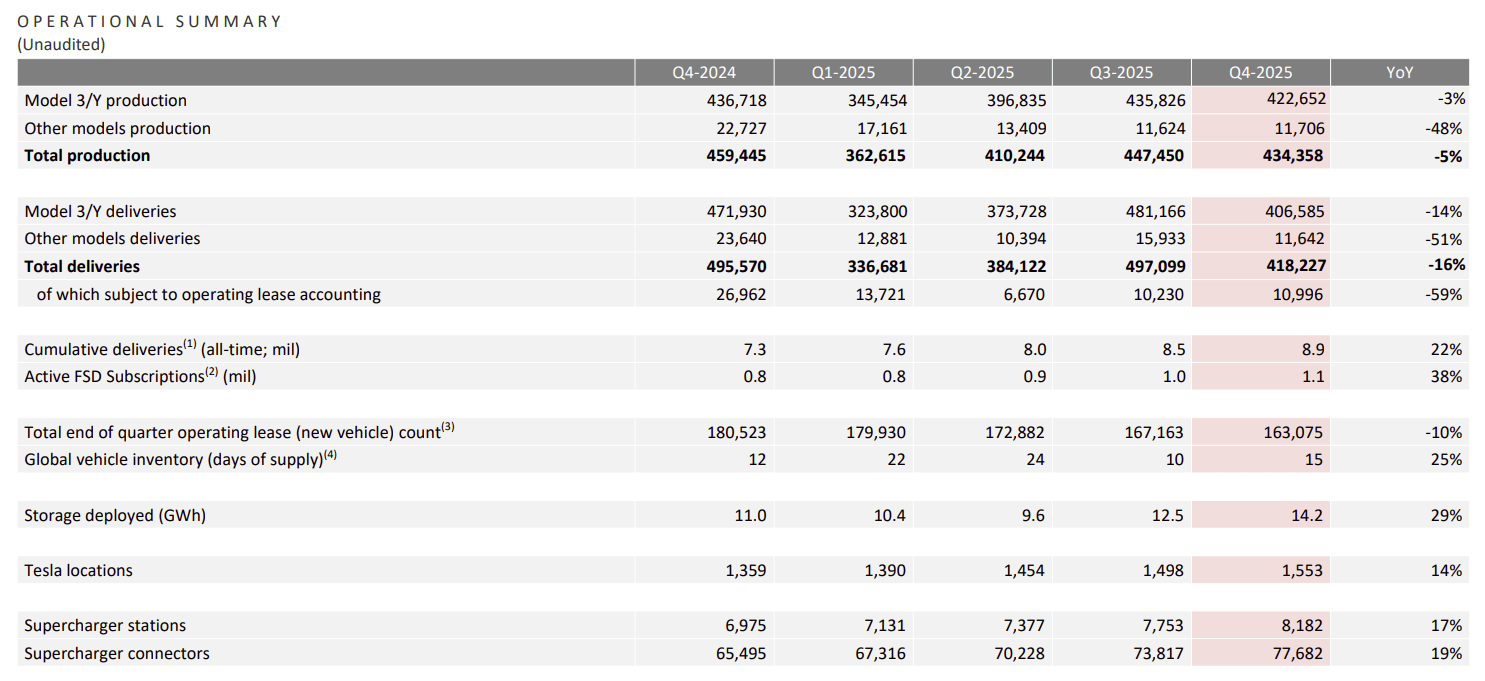

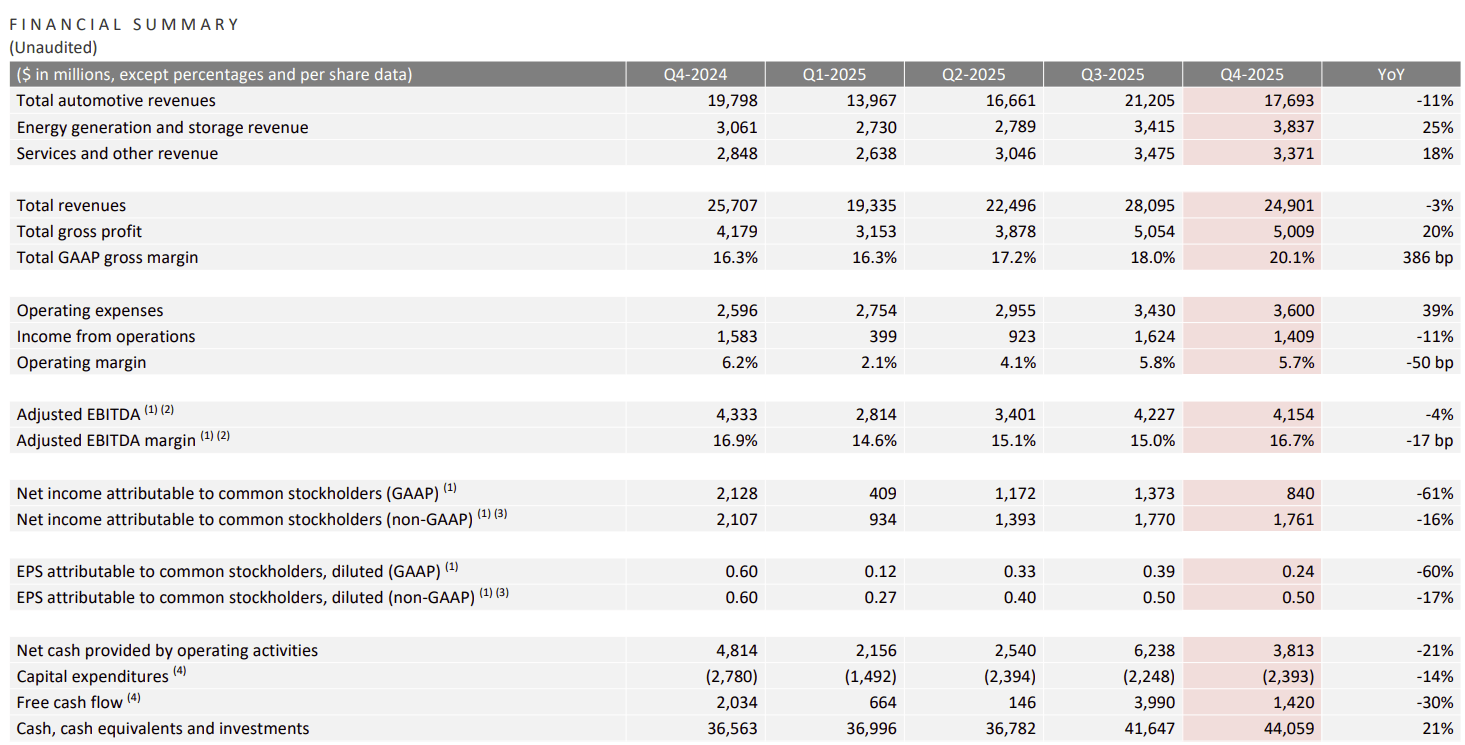

Despite the enticing AI prospects, Tesla's current stock price is still supported by its solid core business. Q4 2025 financial results show that Tesla's consolidated gross margin has rebounded to 20.1%, reaching a two-year peak. Notably, after excluding regulatory credit revenue, its core automotive gross margin also significantly recovered from 15.4% to 17.7%, indicating that the company has regained pricing initiative through deep supply chain optimization amidst an intense global EV price war.

Source: Tesla

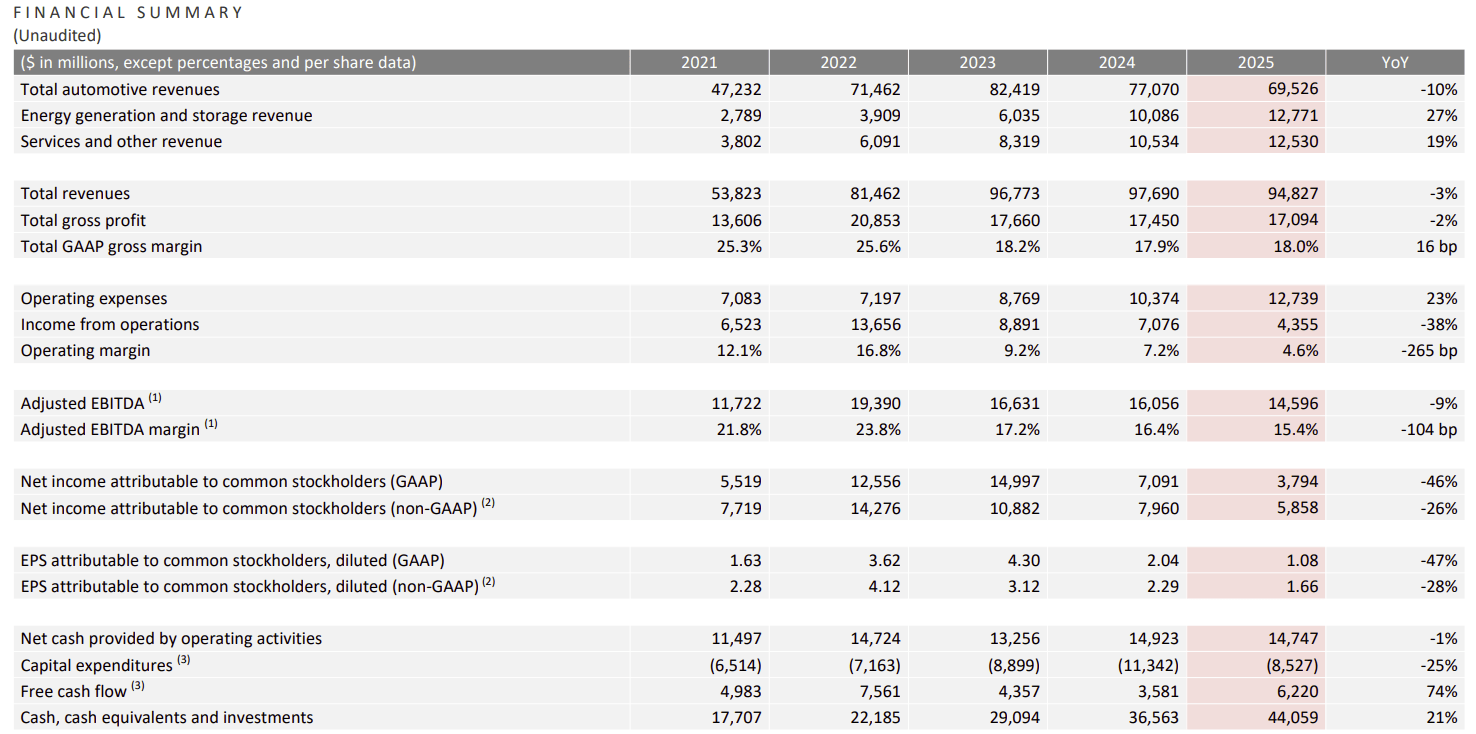

Meanwhile, the energy storage business is growing into Tesla's second growth engine. In Q4 2025, Tesla's energy storage deployments reached a record 14.2 GWh, with annual energy revenue reaching $12.8 billion, up nearly 30% year-over-year. By the end of 2025, the company's cash reserves increased to $44.1 billion, a 21% increase from the previous year. Ample cash flow provides strong support for its "fault tolerance" in high-tech R&D.

Source: Tesla

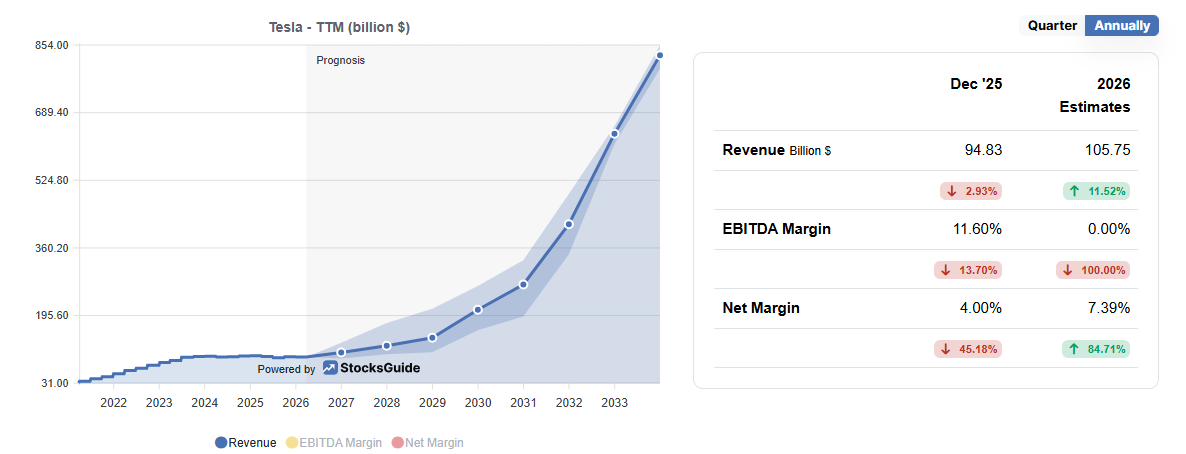

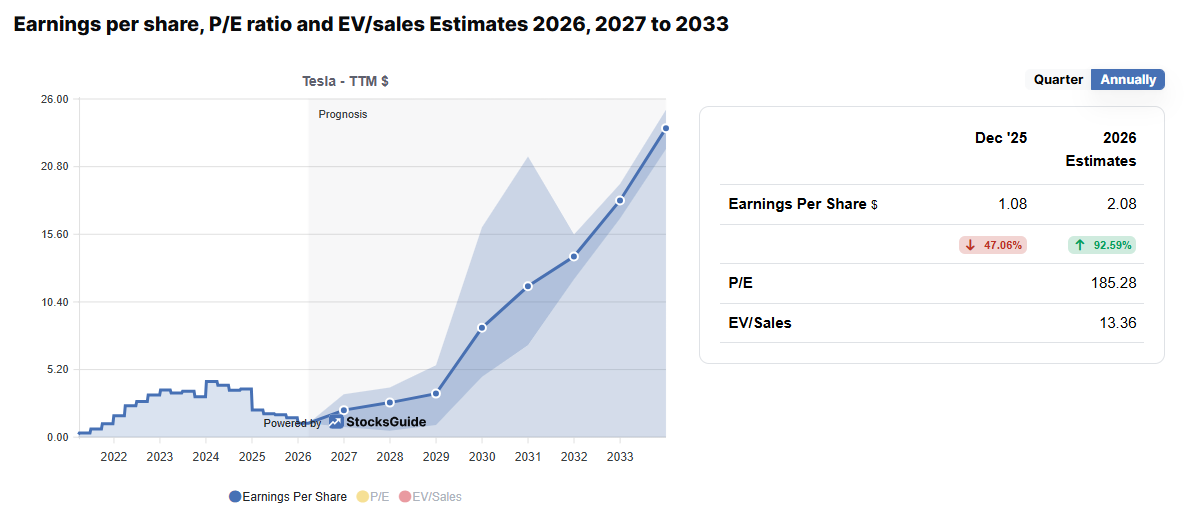

For the 2026 full-year performance outlook, the consensus expectation of 56 market analysts shows that Tesla's total revenue is expected to reach $105 billion, with earnings per share (EPS) projected at $2.08, representing nearly double the growth compared to 2025. This profit growth logic primarily stems from the improvement in manufacturing gross margins and the scale effect of the energy business, and it has not yet fully priced in the dividends brought by the large-scale commercialization of Robotaxi. Meanwhile, the third-generation Optimus robot, acting as a long-term call option, is expected to enter mass production in the second half of 2026; although its short-term contribution to revenue is limited, it determines the upper limit of Tesla's valuation.

Source: stocksguide

Risk Assessment: Sales Stall, Macro Pressures, and Regulatory Walls

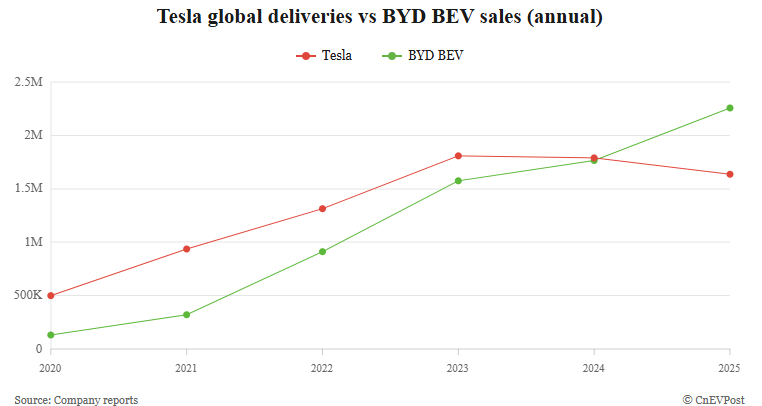

However, the logic of the bear camp is equally rigorous. As Tesla's only current profit engine, the automotive business is facing clear growth pressure. In 2025, Tesla delivered 1.63 million units, an 8.5% year-over-year decrease. This is the first time in the company's history that sales have declined for two consecutive years, and the drop set a record. In terms of global market share, Tesla is facing a strong challenge from Chinese automaker BYD, whose 2025 BEV sales reached 2.257 million units. Particularly in the European market, Tesla's new car registrations recorded a significant 28% drop, reflecting a dilution of brand competitiveness.

Source: cnevpost

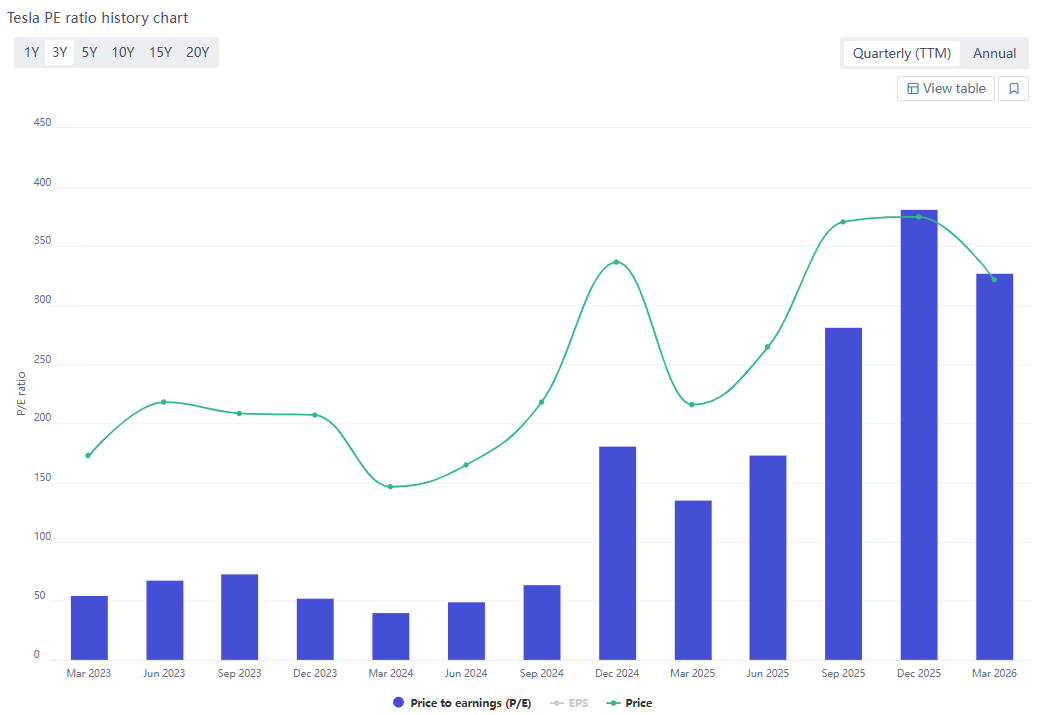

On a macro level, the sensitivity of Tesla's stock price to interest rates has significantly exceeded its sensitivity to energy prices. Although geopolitical conflicts pushed crude oil prices past $150 at one point, the Federal Reserve maintained a benchmark interest rate of 3.5% to 3.75% under a high-inflation background, causing market expectations for rate cuts to be repeatedly deferred. For a high-valuation growth stock like Tesla, which possesses a forward Price-to-Earnings (P/E) ratio of 300 to 370 times, a high-interest-rate environment exerts intense valuation suppression.

Source: fullratio

In addition, regulatory risk is a "black swan" that cannot be ignored. While Cybercab mass production is imminent, Tesla has not yet obtained legal approval for "fully autonomous driving" from agencies like the National Highway Traffic Safety Administration (NHTSA). Organizations such as GLJ Research have pointed out that the accident frequency of Tesla’s Robotaxi is still higher than human driving levels, which could hinder its commercialization progress. Regarding financial pressure, Tesla's capital expenditure (CapEx) in 2026 is expected to exceed $200 billion; if auto sales continue to be sluggish, in the most pessimistic scenario, its free cash flow (FCF) could turn to negative $6.3 billion.

2026 Key Signal Map: Investor Observation Post

Facing a P/E ratio as high as 370 times, Tesla can no longer afford any errors in execution. Investors should focus on the following key milestones in 2026:

- April Production Ramp-up and Regulatory Approval: Observe whether the Cybercab can obtain road exemptions in key states during its initial mass production phase; a failure to match production capacity with regulatory progress will translate directly into inventory pressure.

- Late April Earnings Gross Margin: Pay attention to whether the automotive gross margin, excluding carbon credits, can maintain the 17.7% baseline; a drop below 15% would mean the price war has damaged the company’s operational foundation.

- May Fed Personnel Changes: The policy stance of incoming Chair Kevin Warsh will determine the discount rate, which in turn will affect Tesla's valuation center.

- H2 Optimus Mass Production Costs: Focus on whether the third-generation robot can achieve supply chain standardization and whether the seven-city Robotaxi expansion plan projected by BofA is realized as scheduled.

- SpaceX IPO Diversion Effect: A possible SpaceX IPO in mid-2026 (valuation of $1.5 trillion to $1.75 trillion) may have a diversionary impact on capital within the same sector.

Tesla is no longer a simple "passenger tool" but an ongoing, highly uncertain, and complex technological experiment. Bears often remain correct in their factual analysis but tend to underestimate the market's premium on disruptive innovation; bulls, while enjoying the valuation dividends, must also remain vigilant against the massive volatility caused by a collapse of the "perfect growth narrative." In 2026, the depth of data tracking will directly determine the success or failure of investment decisions.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.