Here Are US Stock Winners Following the Iran Attacks

AI Podcast

Rising oil prices and geopolitical tensions surrounding Iran have caused a broad sell-off in U.S. equities. However, defense and energy stocks have shown resilience, trading near highs. Oil majors like Exxon Mobil and Chevron are benefiting from elevated crude prices, with analysts expecting volatility. Natural gas prices have also surged, particularly LNG, following disruptions to Qatari supply. Defense contractors, including Lockheed Martin and RTX, are seeing renewed interest due to increased military spending and the use of precision weapons. While these sectors offer a hedge against geopolitical risk, valuations for defense stocks are considered high.

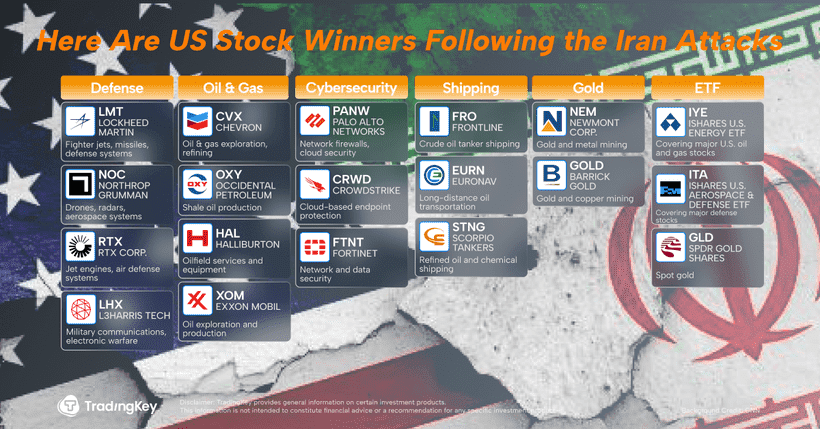

Tradingkey - On Tuesday, U.S. equities extended their slide as rising oil prices and the specter of war in Iran rippled through global markets. The Dow Jones Industrial Average at one point plunged more than 1,000 points. Yet amid that sea of red, two sectors stood firm. Defense and energy stocks defied the downturn: Lockheed Martin Corp. (LMT), RTX Corp. (RTX), and Northrop Grumman Corp. (NOC) hovered near 52‑week highs, while oil producers rallied in tandem with crude climbing from the low‑$70 range toward $80 per barrel. In a landscape ruled by uncertainty, they have become the market’s few reliable hedges against geopolitical risk.

Chevron and Exxon Lead Energy Shares Higher

Investors rushed into U.S. oil majors, rotating toward names such as Exxon Mobil Corp. (XOM), ConocoPhillips (COP), Occidental Petroleum Corp. (OXY), Diamondback Energy Inc. (FANG), and Chevron Corp. (CVX). The latter two have come to embody what traders now call the “Iran premium.”

The weekend strikes renewed fears that Brent crude could soon reach triple digits. Citigroup (C) analysts expect prices to fluctuate between $80 and $90 this week before potentially retreating toward $70 if hostilities subside. Still, they warn that prolonged domestic unrest in Iran or wider regional escalation could keep oil elevated for far longer.

Strategists at Piper Sandler added that U.S. energy shares may continue to benefit from portfolio rebalancing as investors cut exposure to technology stocks.

Natural‑gas prices have surged as well. Euro‑zone benchmarks jumped 39% to €44.51 per megawatt‑hour—the highest in roughly a year—while U.S. natural gas gained 3.5% to $2.96 per MMBtu. In 2023 the United States surpassed Qatar and Australia to become the world’s largest exporter of LNG (liquefied natural gas).

This latest shock began after Iranian drone attacks forced Qatar Energy (state‑owned) to shut its Ras Laffan LNG facility, which supplies about one‑fifth of global gas. The company has yet to detail the extent of damage or when production might resume. LNG from Qatar and the UAE normally flows through the Strait of Hormuz—now closed by Tehran in response to the U.S.–Israeli offensive.

In North America, exporters Venture Global LNG Inc. (VLNG) and Cheniere Energy Inc. (LNG) are scrambling to lift output from their Texas and Louisiana facilities to fill potential supply gaps. On Monday, Venture Global shares surged nearly 20% and Cheniere rose 5.6% as investors priced in windfall profits from higher spot prices. Both pulled back Tuesday, but sentiment remains buoyant on expectations of stronger export demand.

Defense Names Rise on Munitions Demand

The U.S. military’s heavy use of precision weapons during strikes on Iran has reignited interest in the defense complex. Lockheed Martin and RTX rallied sharply. Drone maker AeroVironment Inc. (AVAV) surged more than 10% over two sessions, while Kratos Defense & Security Solutions Inc. (KTOS) jumped 9.6% Monday before easing Tuesday.

Former President Donald Trump has urged European and Asian allies to boost security spending, adding fresh momentum to global defense budgets. Jefferies Financial Group Inc. (JEF) analyst Sheila Kahaoğlu expects this renewed appetite for military investment to spill into the Middle East, where U.S. contractors already capture a sizable share of overseas arms sales.

Still, valuations are not cheap. After years of rerating driven by the Russia–Ukraine war, Western defense stocks are no longer bargains. The new conflict layer merely adds an extra risk premium to already elevated multiples—good for near‑term positioning but a potential amplifier of future pullbacks.

Key Stocks to Watch as Tensions Rise in Iran

The traditional titans—Lockheed Martin, Northrop Grumman, and RTX—continue to anchor U.S. defense spending. Their portfolios span the F‑35 fighter jet, missile and air‑defense systems, radar technologies, and maintenance support, backed by deep order books and long contract cycles.

In systems integration, L3Harris Technologies Inc. (LHX) and General Dynamics Corp. (GD) play key roles in communications networks, command‑and‑control systems, and ground and naval platforms—all positioned to benefit from reliably expanding military budgets.

A newer generation of digital‑defense companies includes Palantir Technologies Inc. (PLTR) and privately held Anduril Industries Inc. Palantir is synonymous with battlefield data analysis, while Anduril specializes in autonomous and AI‑enabled defense systems.

Investors can obtain diversified exposure through ETFs such as the iShares U.S. Aerospace & Defense ETF (ITA), which concentrates on the major primes, or the SPDR S&P Aerospace & Defense ETF (XAR), which holds a more evenly weighted mix of mid‑cap defense and aerospace suppliers.

Among integrated oil majors, Exxon Mobil and Chevron remain top choices, offering exposure across upstream, refining, and marketing operations worldwide. For investors seeking greater oil‑price leverage, upstream‑focused producers such as Occidental Petroleum, ConocoPhillips, and EOG Resources Inc. (EOG) provide higher sensitivity—though also higher volatility.

Popular ETFs include the Energy Select Sector SPDR Fund (XLE), anchored by Exxon and Chevron, and the iShares U.S. Energy ETF (IYE), which tracks the broader U.S. oil‑and‑gas universe.

Beyond producers, the wider “energy‑security” theme extends to service and infrastructure firms such as Schlumberger N.V. (SLB), Halliburton Co. (HAL), and Baker Hughes Co. (BKR), all likely to benefit if sustained high prices spur new drilling and capital‑spending cycles. Meanwhile, demand for oil tankers and LNG carriers could rise as Hormuz Strait disruptions lengthen voyages and push up insurance premiums and freight rates.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.