Red Gold: What You Need to Know About Copper Mining Stocks

AI Podcast

Copper prices experienced a technical correction after reaching record highs in early 2026, but the underlying trend remains strong due to surging demand from AI and global electrification. Supply constraints, with a widening deficit and declining ore grades, suggest a "new normal" above $12,000 per ton. Copper miners offer leveraged exposure, though company-specific risks exist. Commodity ETFs provide direct price exposure but are tactical, while miner ETFs amplify returns. Freeport-McMoRan and Southern Copper are highlighted as core equity holdings, benefiting from strong reserves, low costs, and robust balance sheets.

TradingKey - If you’ve already locked in profits from gold’s surge, now may be the perfect moment to turn your attention to its red‑hued counterpart — “red gold.”

After reaching a record high above US $13,000 per ton in early 2026, copper prices pulled back roughly 10% in what was purely a technical correction, not the end of the trend. What seems like noise on the macro level barely scratches the structural reality underneath — the clash between a supply chain under strain and a demand revolution that continues to fortify the market’s base.

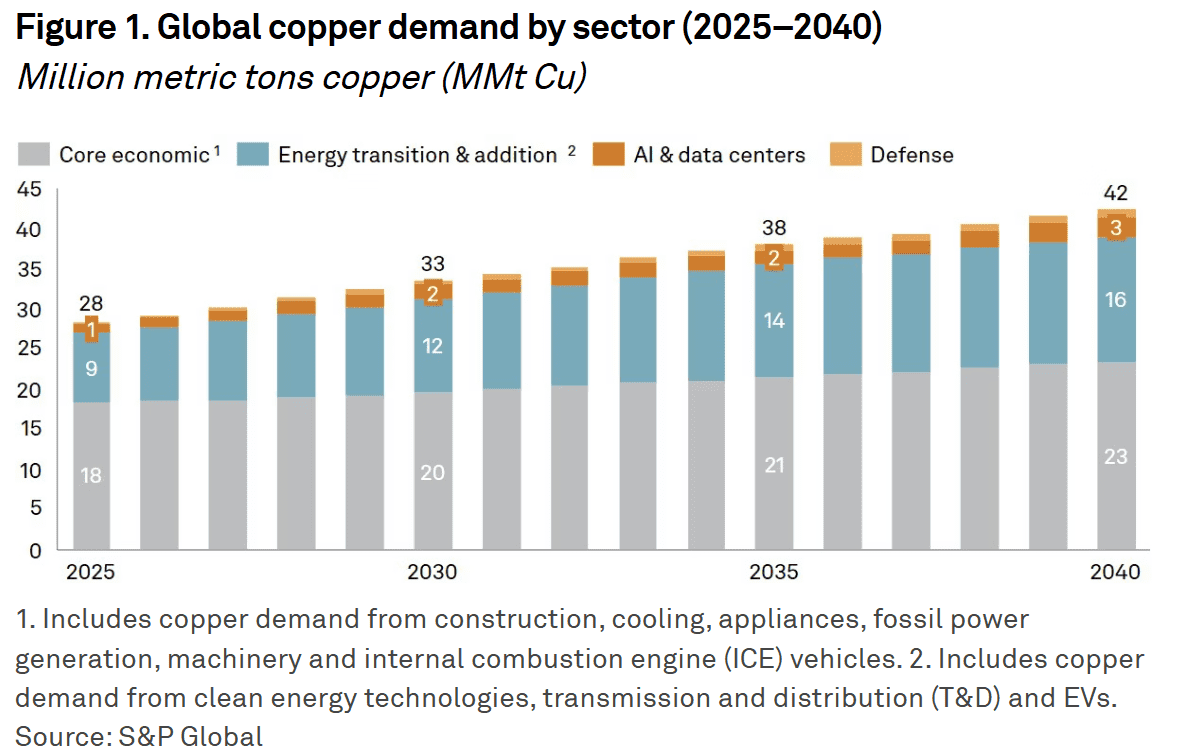

Copper’s identity has undergone a structural mutation. One AI data center consumes nearly ten times as much copper as a traditional facility, and an electric vehicle uses three to four times more copper than a gasoline car. By 2026, rigid demand from AI infrastructure and global grid reconstruction has more than offset weakness in real estate cycles. Each megawatt of data‑center capacity alone requires 20 to 40 tons of copper. As long as humanity’s appetite for computing power and clean energy remains unquenched, copper demand will keep moving one way — forward.

The problem lies on the other side of the ledger. Supply is hitting a physical wall. Morgan Stanley (MS) estimates that the refined‑copper deficit will widen to 590,000 tons in 2026, the largest in two decades. The global average ore grade has dropped below 0.4%, and London Metal Exchange (LME) inventories would cover less than three days of global use. With production capacity unable to ramp up in the near term, any price pullback is merely a mirage within an environment of historic scarcity.

At above US $12,000 per ton, copper is establishing a “new normal.” Short‑term swings still mirror fluctuations in macro data, but the physical shortage in electrical systems doesn’t lie. The reality of a high‑volatility yet high‑anchored market is becoming the defining shape of this cycle.

Copper Miners: High‑Beta Machines for Amplified Profits

Like gold miners, copper stocks deliver returns with built‑in leverage. Their valuations are tightly correlated to spot prices, but the relationship is never one‑to‑one — operating leverage makes them inherently more elastic.

Imagine a miner with an all‑in sustaining cost of US $6,000 per ton. If copper rises from US $9,000 to US $12,000 — a 33% increase — its per‑ton profit doubles from US $3,000 to US $6,000. In other words, a 30% gain in the commodity translates into a 100% surge in profit. That leverage effect becomes even stronger during valuation recoveries.

Still, copper miners are not pure copper plays. Investors face company‑specific risks. Geopolitics and licensing remain key variables: much of the world’s copper supply sits in Chile and Peru, where tax‑policy shifts or mining‑right disputes can immediately affect share prices. Another crucial factor is ore grade. As legacy mines decline, operators with low‑cost, high‑quality reserves are developing the strongest competitive moats.

ETF Choices: Buying the “Product” or the “Factory”?

When allocating through ETFs, the first step is to distinguish between commodity‑based exposure and equity‑based exposure.

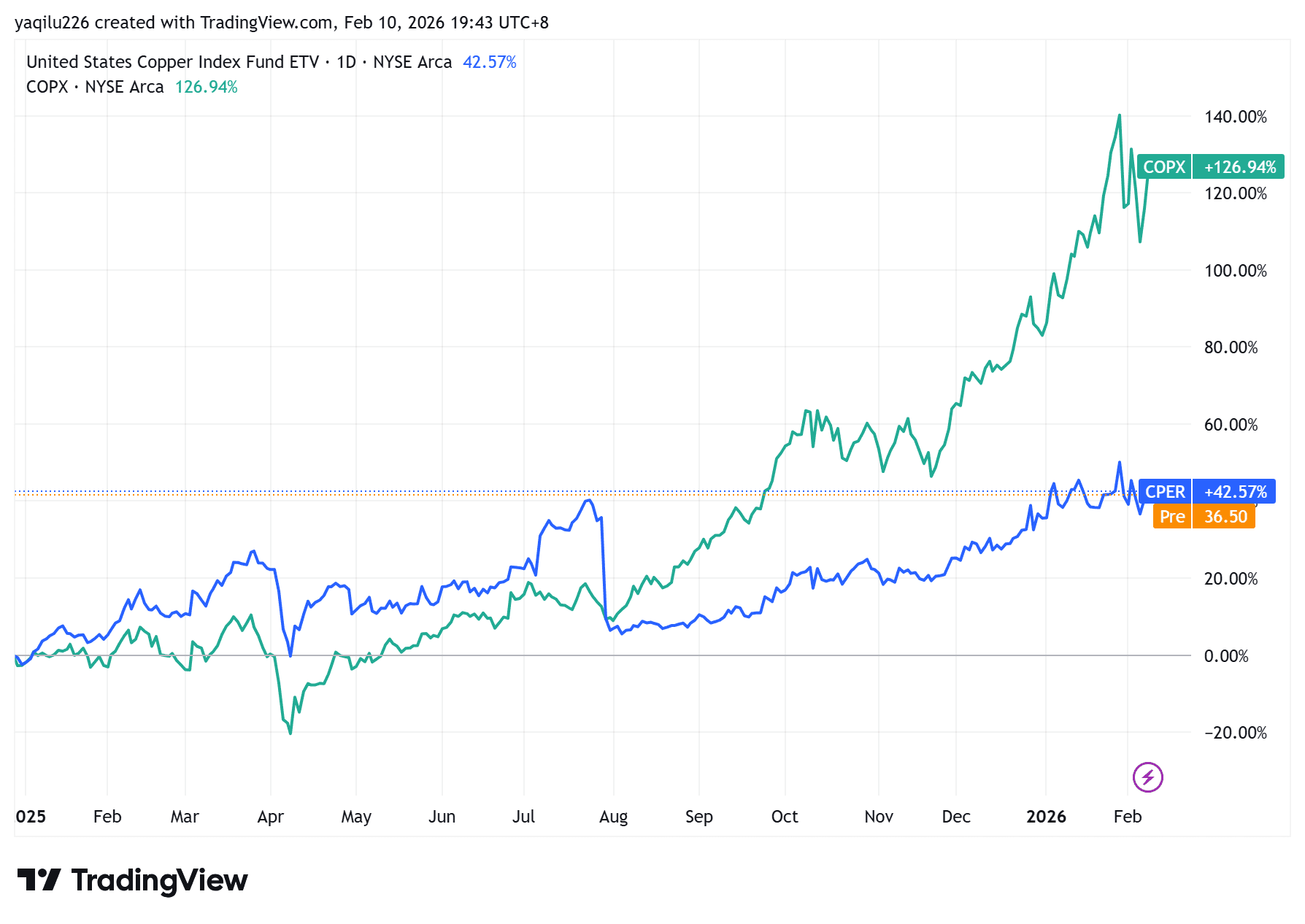

A copper‑price ETF — such as United States Copper Index Fund (CPER) or iPath Series B Bloomberg Copper Subindex Total Return ETN (JJCTF) — offers the purest directional exposure. These funds track copper prices through rolling a series of futures contracts. For investors who simply want to express a bullish view on copper without evaluating management efficiency or balance‑sheet risk, this is the most direct route. However, futures‑roll costs can quietly erode returns over time, meaning such ETFs are not designed for passive, long‑term holding. They work better as tactical instruments — for short‑term allocations or as hedges against market positioning.

A copper‑miner ETF, such as Global X Copper Miners ETF (COPX), works differently; it delivers equity‑style leverage to the metal’s price. In 2025, COPX returned more than 100%, dramatically outperforming spot copper. The fund invests in a global basket of mining producers whose margins expand faster than the commodity when prices rise. Although COPX declined sharply during the early‑2026 pullback, valuation compression followed — average portfolio P/E ratios retreated to around 20 times. For investors who believe in copper’s long‑term story and can tolerate volatility, this structure provides a more aggressive way to capture rebounds, translating the metal’s momentum into amplified corporate earnings.

Core Holdings: Two Copper Giants Worth Watching

Beyond ETFs, positioning directly in industry leaders can generate more precise alpha.

Freeport‑McMoRan Inc. (FCX) is the world’s largest publicly listed copper producer. Its crown jewel is the colossal Grasberg mine in Indonesia, one of the most prolific copper‑gold deposits on the planet and the foundation of its low‑cost operations. Freeport remains the most liquid and pure‑play copper leader in U.S. equities. According to early‑2026 guidance, production is projected to rise sharply by 2027. The company’s balance sheet is exceptionally strong, with net debt‑to‑EBITDA at just 0.5 times — evidence of resilience during price volatility and capacity for continued share buybacks.

Southern Copper Corp. (SCCO) is the undisputed king of reserves. Among all listed miners, it holds the largest copper resource base, with primary operations in Peru and Mexico. Its edge lies in an extraordinarily low all‑in sustaining cost, making it one of the most profitable copper producers globally. For long‑term investors, Southern Copper’s generous dividend policy — maintained at consistently high payout ratios — adds an additional layer of return. In an environment of rising copper prices, shareholders benefit not only from capital appreciation but also from a robust, recurring cash yield that underscores the company’s strength and discipline.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.