Silver’s Quiet Shift: The Key Variables You Should Know

AI Podcast

Silver's traditional correlation with real rates and the USD is shifting due to rising global debt and fiscal strain, repositioning it as a hedge against credit risk. Industrial demand, driven by photovoltaics and AI data centers, now exceeds 60% of total demand, creating structural deficits projected to continue through 2026. Supply remains inelastic as most silver is a by-product. A significant correction in January 2026, triggered by the Warsh nomination, cleared leveraged positions, but the underlying fundamentals of debt hedging and industrial scarcity remain intact, supporting silver's role as a strategic, high-beta asset.

TradingKey - Silver (XAGUSD) has been treated as gold’s higher‑beta twin — a “shadow asset” whose price largely moved with real rates and the U.S. dollar. But that relationship is breaking down. As the world moves deeper into an era of high debt, heavy fiscal strain, and energy transition, silver’s underlying logic is changing. Its independence — and its strategic value — are being re‑priced.

Rates and Credit: From Carry Trade to Debt Hedge

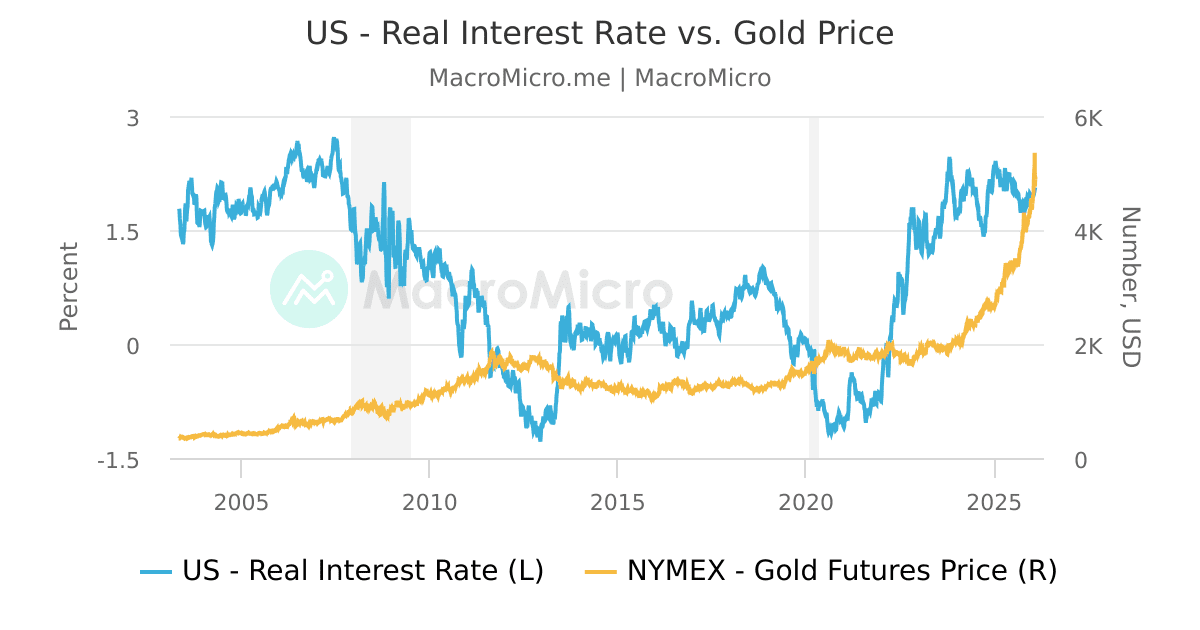

Traditionally, rising real interest rates spelled trouble for silver. The metal pays no yield; higher rates boost its opportunity cost and depress prices. That rule simply stopped working between 2025 and early 2026. The decoupling signals a market shift: investors are no longer calibrating small changes in carry—they’re pricing sovereign credit risk. With public debt at or beyond a tipping point, the real fear is that governments will use inflation and currency depreciation to erode what they owe. In that world, gold/silver has evolved from a rate‑sensitive cyclical asset into a structural hedge against debt and credit anxiety.

Industrial Demand: Scarcity Returns

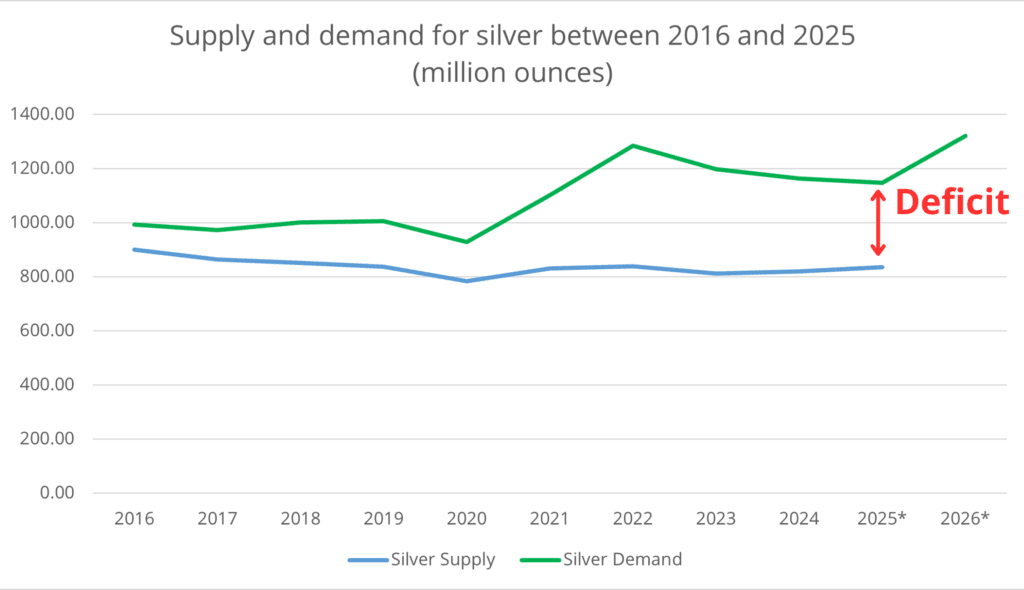

Unlike gold, where investment drives over 90 per cent of demand, silver’s base is genuinely industrial. As photovoltaic installations smashed expectations in 2025 and AI‑era data centers began consuming vast volumes of high‑performance electronic paste, industrial use of silver climbed past 60 per cent of total demand. Prices followed. At one point in 2025 silver rallied almost 180 per cent — triple gold’s 60 per cent advance — driven by a persistent structural deficit. Global shortfalls are projected to remain near 7,000 to 8,000 tonnes in 2026.

Source: The Silver Institute

Roughly 70 per cent of mined silver comes as a by‑product of copper, lead, or zinc extraction. That makes supply unusually rigid: even steep price rises cannot easily trigger incremental output. The combination of inelastic supply and explosive end‑use demand gives silver one of the highest upside betas in the metals complex — volatility, but with leverage to structural scarcity.

The Warsh Shock: Clearing the Leverage

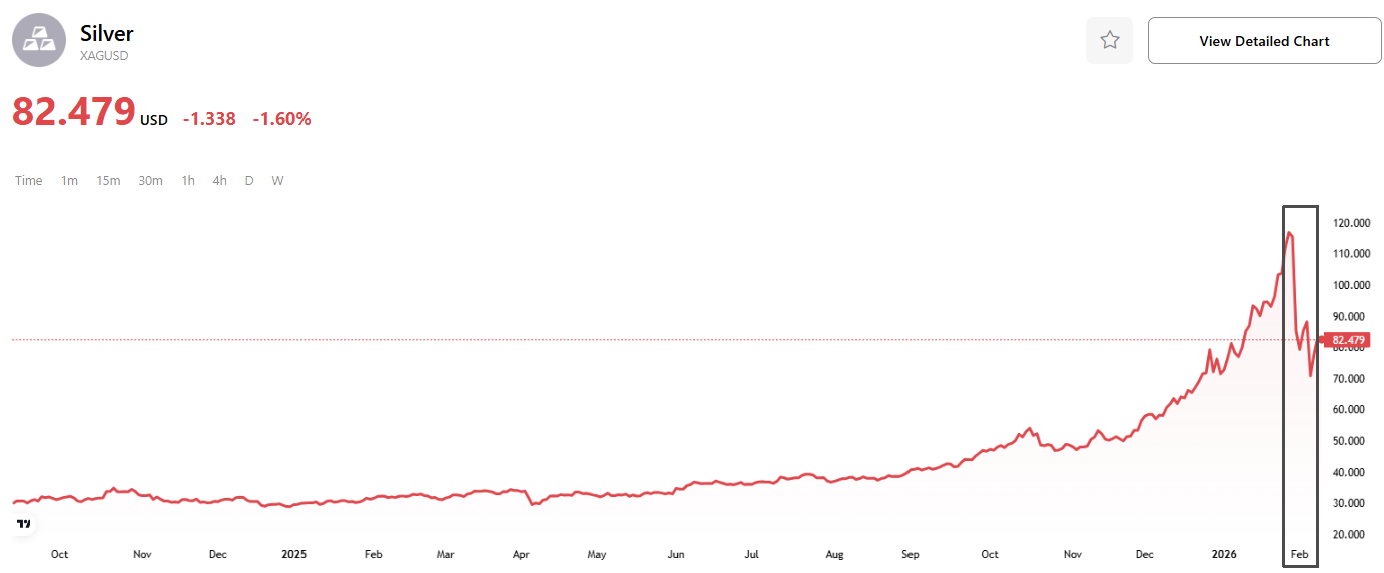

The Federal Reserve’s leadership change added fuel to short‑term turbulence. When Kevin Warsh — a critic of quantitative easing and the Fed’s bloated balance sheet — was nominated as the next Chair, markets immediately priced in tighter liquidity. The result was brutal. In late January 2026, dubbed “Black Friday” for metals, silver collapsed 40 per cent in three trading days, retreating from a record $120 per ounce. The move wiped out leveraged long positions that had hinged on perpetual dollar debasement.

Yet the correction wasn’t the end of the story. It effectively reset positioning, pulling silver out of a one‑way speculative bubble and back into a high‑volatility range anchored by fundamentals. As long as global debt remains excessive and fiscal expansion continues, silver’s medium‑term role as both hedge and store of optionality is intact.

The New Hedging Paradigm

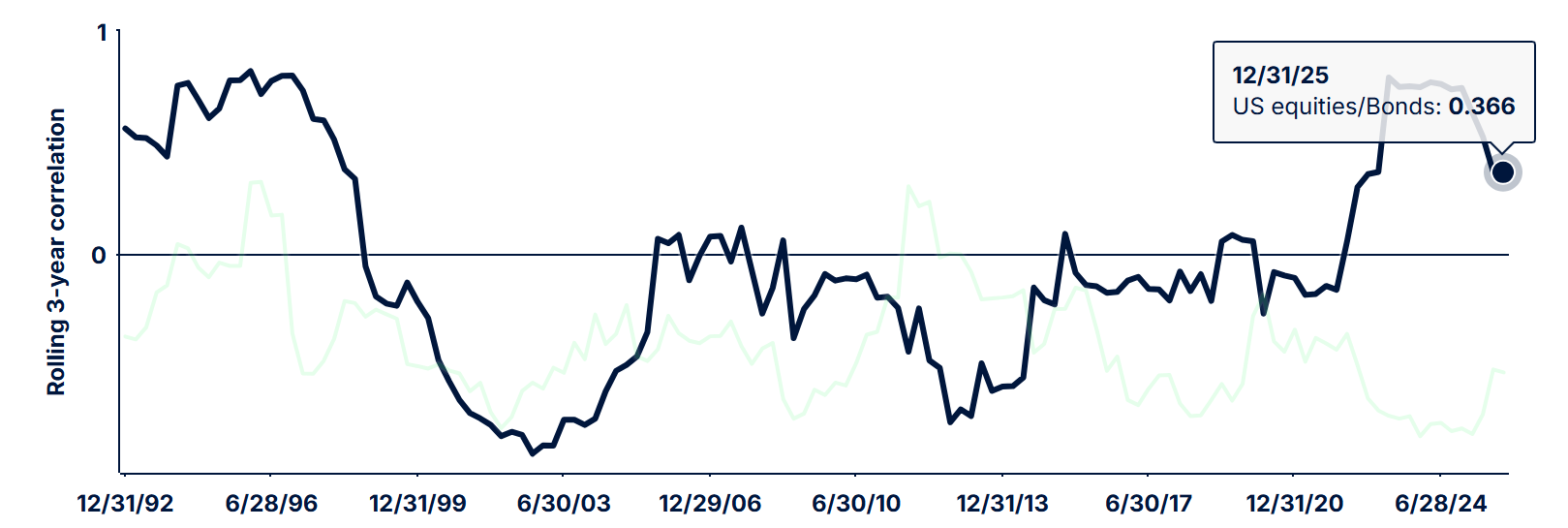

In today’s environment — high debt, sticky inflation, and violent swings in long‑dated Treasury yields — duration risk has become a central macro variable. The stock‑bond correlation in the U.S. has surged to its highest in 30 years, undermining the traditional 60/40 portfolio’s ability to buffer shocks.

Within this new regime, silver’s higher volatility (about 1.7 times that of gold) and its low correlation to conventional assets have made it an increasingly popular hedge against duration risk and monetary dilution. As the dollar weakened in early 2026 on growing credit concerns, haven flows left U.S. assets and found a new home in silver — magnifying both its financial‑hedge appeal and its catch‑up potential as a physical commodity.

US Equities/Bond

At the intersection of industrial transformation, sovereign‑credit stress, and accelerating de‑dollarization, silver is graduating into a high‑beta strategic asset. The Warsh shock may have cleared excess leverage, but it hasn’t changed the direction of travel — it simply reset the stage for the next phase of repricing.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.