Do More Volatile Gold Stocks Mean Greater Opportunity?

AI Podcast

Gold experienced a flash crash in early 2026 after record highs, yet saw significant ETF inflows. Major banks maintain bullish gold price targets, suggesting dips offer re-entry opportunities. Gold miners, due to operating leverage, offer amplified gains (and losses) compared to physical gold. Newmont Corp. provides stability and dividends, while Barrick Gold emphasizes efficiency and cash flow. Institutional capital is increasingly treating gold as a permanent allocation, adding on weakness. Miner ETFs like GDX and GDXJ offer exposure to the sector's leveraged upside.

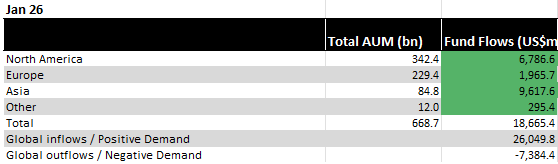

TradingKey - After a record‑breaking 2025, the gold (XAUUSD) market opened 2026 with a jarring flash crash. Prices fell abruptly from record highs, at one point marking the steepest one‑day drop in a decade. Yet the data told another story. In January, even as prices whipped back and forth, global gold ETFs saw an extraordinary US $26 billion in net inflows.

Source: WGC

This adjustment looks less like the end of a cycle and more like what happens when a market catches its breath after sprinting too far. Both J.P. Morgan (JPM) and Goldman Sachs (GS) remain committed to gold‑price targets above US $5,000. For investors, every dip driven by short‑term profit‑taking is effectively an opportunity to re‑enter at a stronger base.

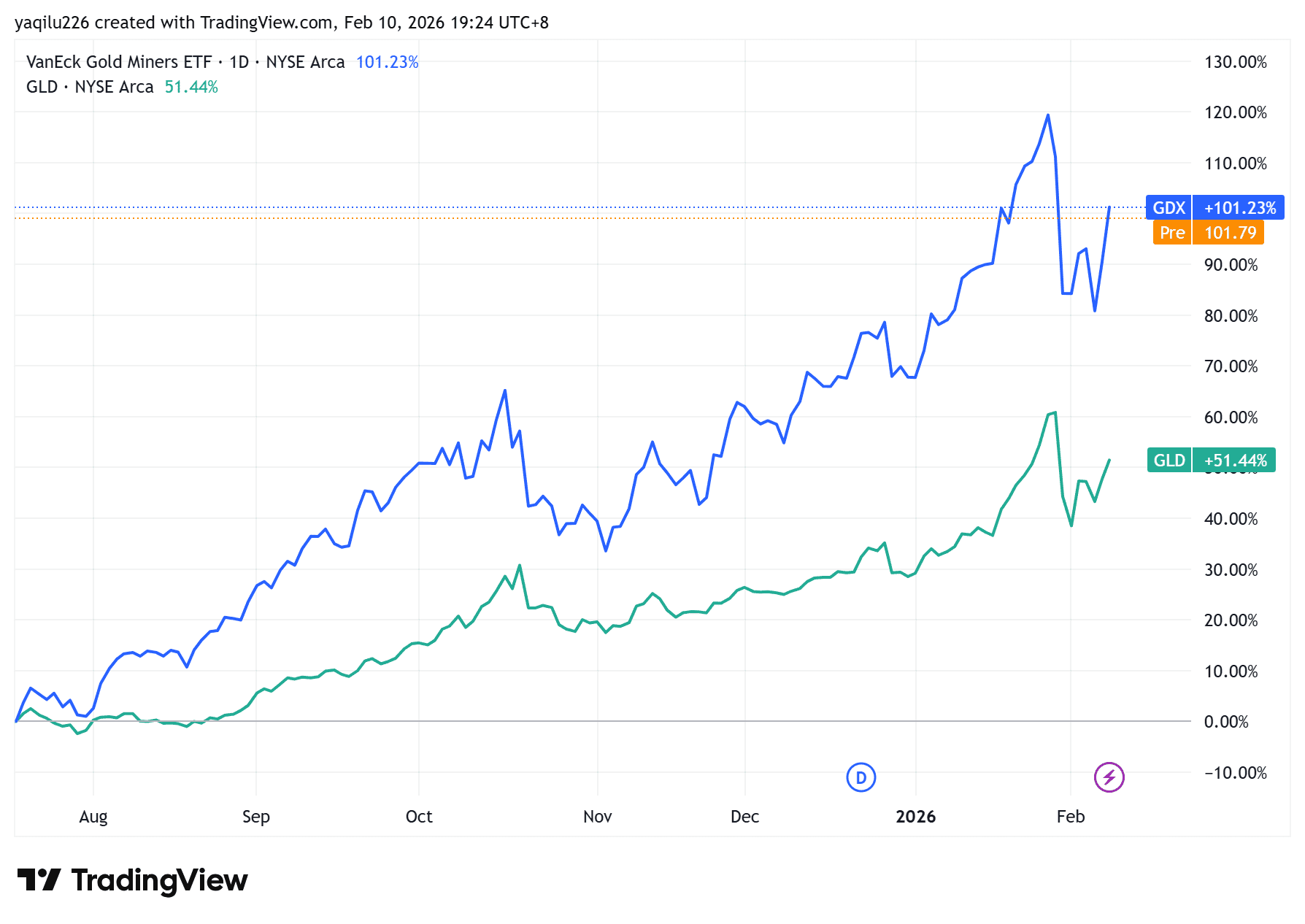

If a US $5,000 gold price already feels daunting, consider this: over the past year, when the physical ETF SPDR Gold Shares (GLD) gained around 90%, the VanEck Gold Miners ETF (GDX) index of major miners surged 200%, and some leveraged hybrid funds like GDMN (Franklin Gold and Precious Metals ETF) jumped 239%.

Gold‑mining stocks move in tandem with the metal, but never one‑to‑one. Their sensitivity to gold is captured by what analysts call the “gold beta,” and it is almost always above one. The reason lies in operating leverage. Imagine a miner with an all‑in sustaining cost of US $1,500 per ounce: if gold rises from US $2,000 to US $2,200 —a 10% move — the company’s profit per ounce jumps from US $500 to US $700, a 40% increase. Gold itself produces no cash flow; a mining company, by contrast, turns metal into margin. Its fixed costs function as embedded leverage. That is why miners tend to deliver roughly one‑and‑a‑half to three times gold’s gains in an upswing.

Of course, that leverage works both ways. In the U.S. market, the VanEck Gold Miners ETF shows far higher volatility than physical ETFs such as SPDR Gold MiniShares Trust (GLDM). Over time, the annual amplitude of mining shares is typically 1.5 to 2 times that of the underlying metal. Get the direction right and you capture a premium over price; get it wrong or exit too late and you absorb a deeper drawdown than gold itself.

Among the leading mining names, Newmont Corp. (NEM) stands as the industry’s aircraft carrier. It remains the largest producer globally and owns an exceptionally high‑quality asset base, heavily weighted toward stable jurisdictions in North America and Australia. After a wave of strategic acquisitions in 2025, its production capacity expanded while operational costs stayed among the lowest in the sector. Even through the 2026 correction, its all‑in sustaining cost remained competitive, leaving profit margins resilient. For investors prioritizing stability and yield, Newmont offers both gold‑price exposure and consistent dividends — a blend that makes the stock resemble a high‑quality bond with growth upside.

Barrick Gold Corp. (GOLD), by contrast, embodies efficiency and cash‑flow strength. Known for tight cost control and disciplined capital allocation, Barrick’s 2025 fourth‑quarter report showed free‑cash‑flow growth that outpaced the rise in gold itself. It now emphasizes profitability over volume, a stance that preserves margins even when prices fluctuate. Its deep operations in Nevada and other core mining hubs secure multi‑decade reserves. For investors looking for skilled execution and profit momentum in any subsequent gold rebound, Barrick offers a more aggressive expression of the same theme.

At the institutional level, a structural change in flows has become evident. In 2025, the World Gold Council reported average daily turnover in gold markets hitting a record US $361 billion. In North America alone, daily trading in gold ETFs averaged US $5 billion, more than double the 2024 figure. Even during the bouts of sharp selling in early 2026, flagship ETFs continued to register net inflows. That pattern underlines the behavior of long‑horizon capital — central banks, sovereign funds, pension pools — now treating gold as a permanent allocation, adding on weakness rather than chasing rallies. The price midpoint of the market is being raised progressively, not built on leveraged speculation.

For investors seeking additional elasticity beyond spot gold, miner‑focused ETFs remain effective vehicles. The broad‑based VanEck Gold Miners ETF (GDX) concentrates on the world’s largest producers such as Newmont and Barrick, offering lower volatility, stronger cost discipline, and reliable dividends. The VanEck Junior Gold Miners ETF (GDXJ) tilts toward smaller, high‑growth producers and reacts far more sharply to price movement — an instrument suited for the acceleration phase of a bull cycle.

After the early‑2026 shake‑out, the leverage embedded in mining equities remains very much alive. For patient capital, the same volatility that unnerves traders continues to create asymmetry. In every major gold cycle, miners start as amplifiers, endure the purge, and then lead the next leg higher.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.