No AI Bubble: AWS Growth Hits Bottom, Amazon's Earnings Explode

Key Performance Highlights

TradingKey - Amazon's Q3 2025 earnings report showed strong overall performance, with both revenue and profit exceeding Wall Street expectations. This was primarily driven by accelerating growth in AWS cloud services, significant returns on AI investments, and continued expansion in the advertising business.

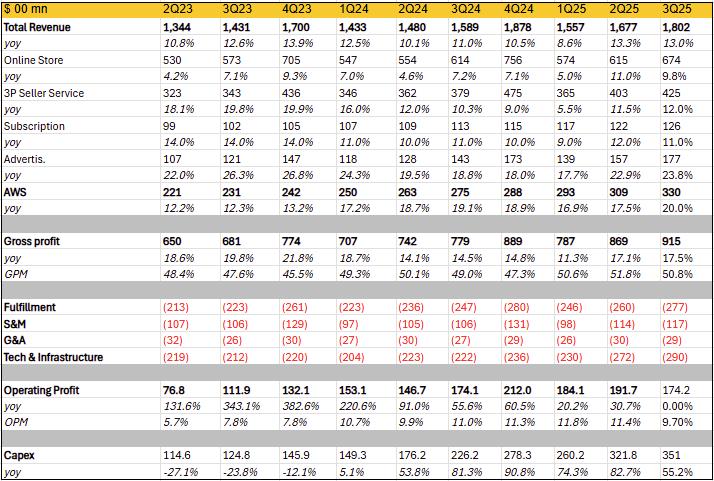

In the quarter, Amazon reported revenue of $180.2 billion, up 13% year-over-year, surpassing market expectations of $177.8 billion. Gross margin expanded by 1.8% to 50.8%, with the above-expectation improvement mainly attributable to robust growth in high-margin businesses like advertising and favorable foreign exchange impacts. Net income rose 39% to $21.2 billion, with earnings per share at $1.95, far exceeding the expected $1.56. Operating income was $17.42 billion, impacted by $4.3 billion in one-time charges (including a $2.5 billion FTC settlement and $1.8 billion in severance costs); adjusted operating income reached $21.7 billion, significantly above market forecasts. Net income of $21.2 billion included a $9.5 billion pre-tax gain from Amazon's investment in the AI company Anthropic.

E-commerce and Subscription Businesses Remain Strong

Amazon's retail segment continued its strong performance this quarter. Online Store sales revenue reached $67.4 billion, up nearly 10% year-over-year, driven mainly by Prime Day promotions, inventory optimization, and AI-powered recommendation systems (such as the Rufus chatbot). Additionally, through robotics and logistics improvements, the company achieved faster delivery and expanded same-day service to more cities, significantly enhancing online sales efficiency.

Third-party seller services revenue was $42.5 billion, up 12% year-over-year, benefiting from AI-enhanced seller tools (such as the Creative Studio ad tool) and global seller base expansion. Subscription service revenue grew 11% to $12.6 billion, fueled by global Prime membership growth (over 200 million active users) and new offerings (such as Prime Video live sports and Alexa Plus). By bundling AI features, the company increased user stickiness and plans further investment in rural market expansion. This segment, with its high margins, is a key pillar of the company's recurring revenue.

The advertising business, one of the company's growth engines, continued to perform exceptionally. It primarily includes sponsored ads, display ads, and video ads, targeting sellers, suppliers, publishers, and authors. This quarter, revenue grew nearly 24% to $17.7 billion, marking the third consecutive quarter of accelerating growth, driven by portfolio expansion and momentum from a large base. The company increased investment in video and streaming ads, with Prime Video becoming a significant revenue source. Though still in early stages, growth has been substantial.

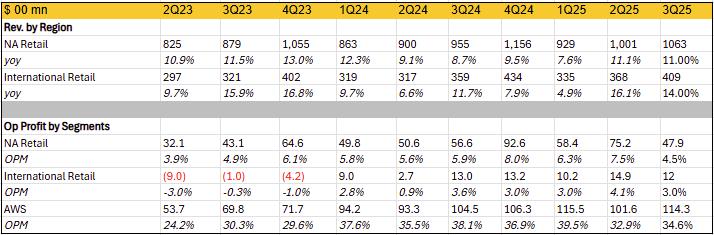

Geographically, both North America and international segments achieved double-digit growth. Operating income declined year-over-year mainly due to FTC legal settlement costs and severance expenses, but adjusted figures show Amazon's core e-commerce profitability remains on an upward trend.

AI Potential Fully Unleashed

While the e-commerce business performed well, it was insufficient to drive Amazon's after-hours stock surge of over 13%. The real catalyst was the market recognizing the gradual emergence of Amazon's AI potential. If Amazon's artificial intelligence potential is likened to a marathon, with AWS's dominant position in cloud infrastructure, Amazon has already secured a leading starting position. This means that while competitors like Microsoft and Google are still catching up in AWS's cloud business and laying foundations, Amazon has pulled ahead and is preparing to sprint through the later stages.

Amazon's AI advantage has created the company's economic flywheel effect, primarily reflected in two aspects in this earnings report: AWS business acceleration and internal process optimization.

AWS: Growth Bottoms Out and Rebounds

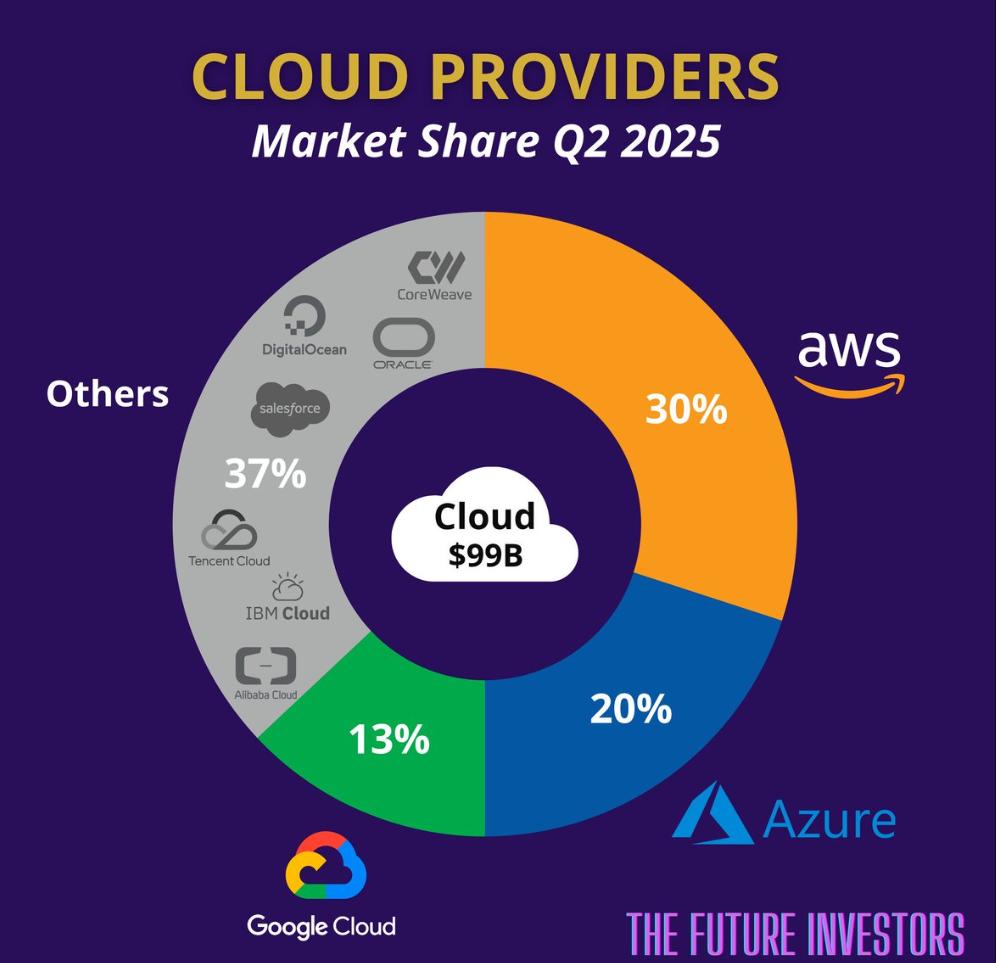

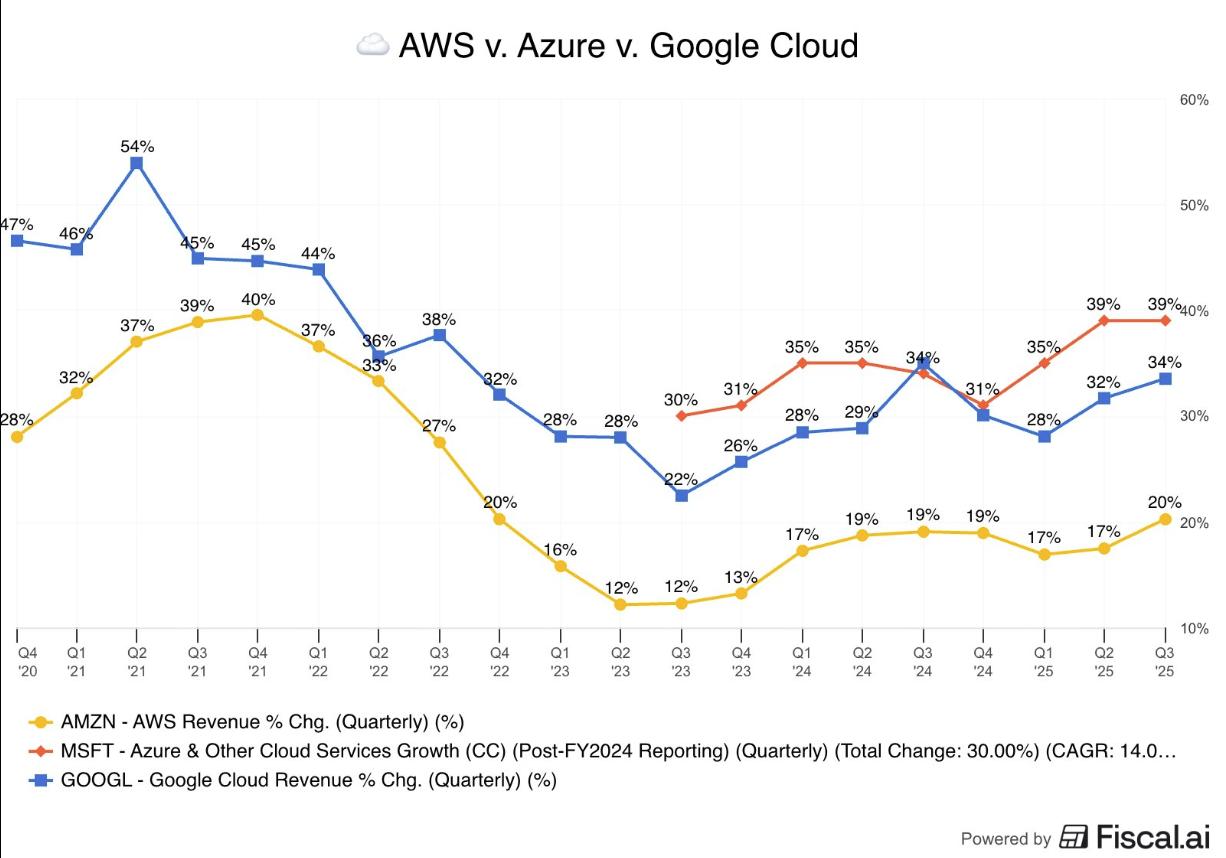

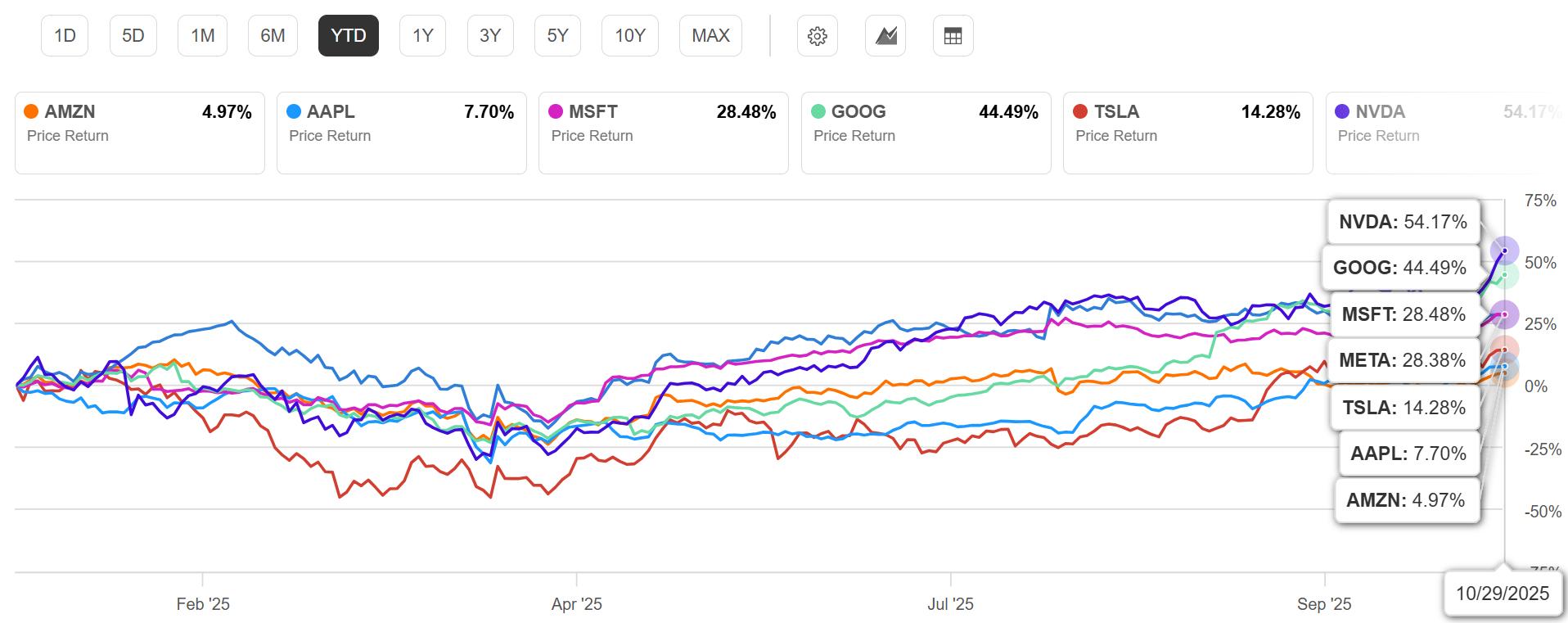

AWS remains the dominant player in the cloud sector, but compared to Azure's 39% and Google Cloud's 34% growth this quarter, AWS had seen its growth stagnate for six consecutive quarters, raising some market doubts about Amazon and explaining why its stock significantly underperformed other big tech peers year-to-date. While the mainstream explanation was compute capacity bottlenecks, it also sparked concerns about AWS competitiveness.

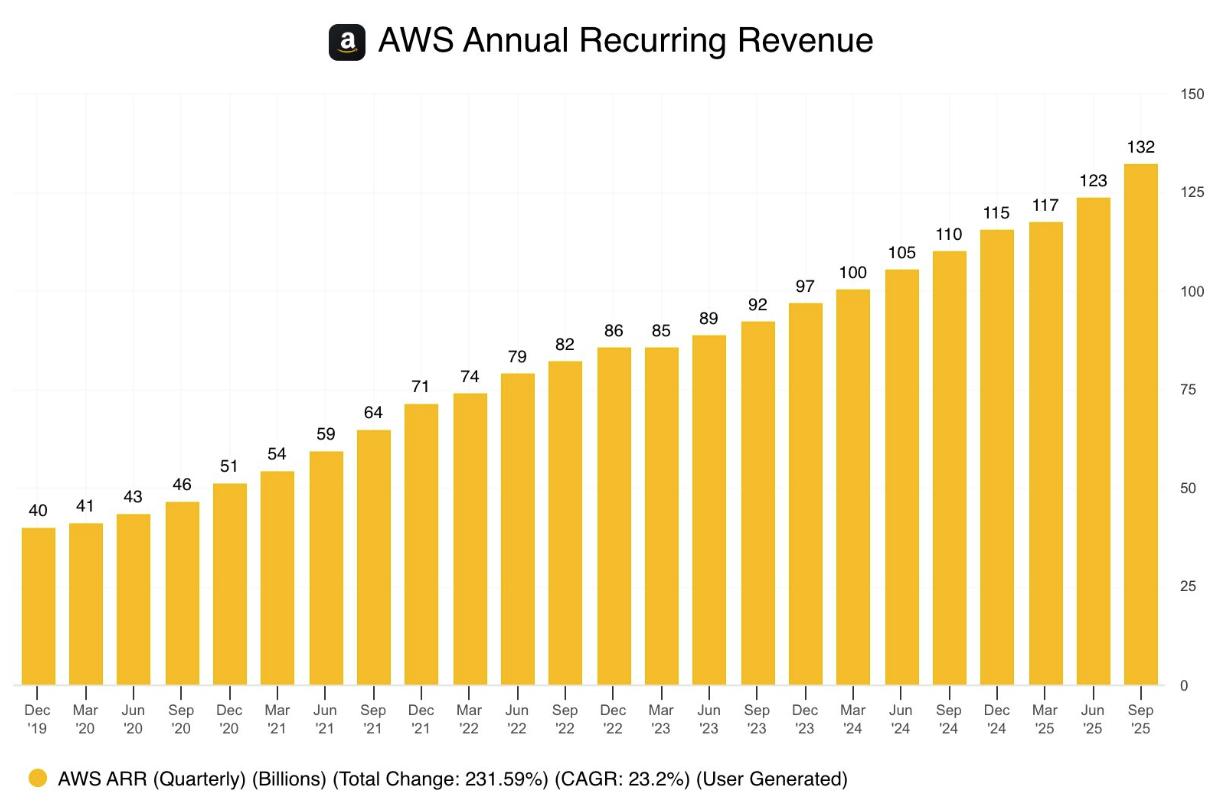

Thus, AWS growth is currently Amazon's single most important metric. It is not only a profit pillar but also the core driver of the AI flywheel—training AI models with massive data, which in turn enhances cloud service appeal, creating a positive feedback loop. This quarter, AWS revenue reached $33.0 billion, up 20.2% year-over-year, marking the highest growth in 11 quarters and exceeding analyst expectations. This was mainly driven by exploding AI demand, infrastructure expansion, and accelerating customer adoption. Operating profit was $11.4 billion, with an operating margin of 34.6%; the year-over-year contraction may relate to higher Capex, depreciation, and R&D spending.

More importantly, AWS backlog reached $200 billion by the end of Q3, excluding several undisclosed new deals closed in October, which management said collectively exceeded total Q3 deal volume. AWS has invested over $100 billion in AI data centers and custom chips (such as Trainium), alleviating capacity bottlenecks. Though growth rates lag competitors, AWS's scale effect (annualized revenue over $132 billion) makes it stickier in enterprise migrations. More AI demand generates data feedback, improving model accuracy and further attracting developers, creating a "scale is advantage" cycle.

Internal Efficiency Surge: AI-Driven Layoffs and Automation

Amazon has initiated a new round of layoffs, primarily due to significantly increased AI application rates in internal processes. Specifically, the company announced layoffs of approximately 14,000 corporate employees, or 4% of its roughly 350,000 corporate staff, with the process continuing into early 2026 and potentially scaling to 30,000.

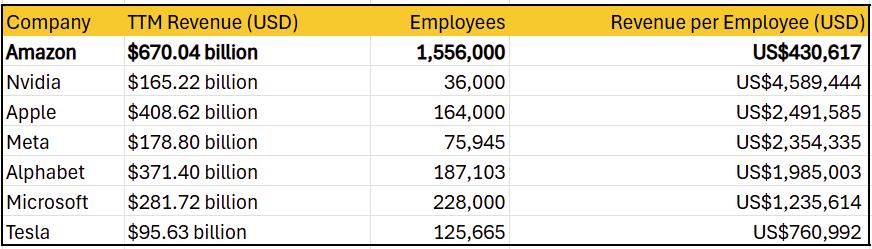

We believe the layoffs in 2025 so far may only be the beginning of a larger-scale initiative, particularly targeting auxiliary or non-core roles. From a Revenue per Employee perspective, whether based on total headcount or the 350,000 corporate employees, Amazon's operational efficiency remains low. As AI automation deepens, the company has deployed 1 million robots; on a 1.5 million employee base, it plans to replace over 600,000 positions with robots by 2033, achieving 75% operational automation to handle doubled sales volume. This implies at least 600,000 more potential layoffs in coming years.

With stable double-digit revenue growth from cloud and AI-driven businesses, plus long-term cost savings potential of tens of billions from AI and robotics replacing labor, we are highly optimistic about Amazon's future margin expansion.

Forward Guidance and Long-Term Strategy

Amazon expects Q4 net sales of $206 billion to $213 billion, with the market's prior consensus midpoint at $208 billion. The new guidance midpoint ($209.5 billion) is slightly above expectations. Operating profit is projected at $21 billion to $26 billion, above the company's prior forecast of $21.2 billion and market expectations of $23.8 billion.

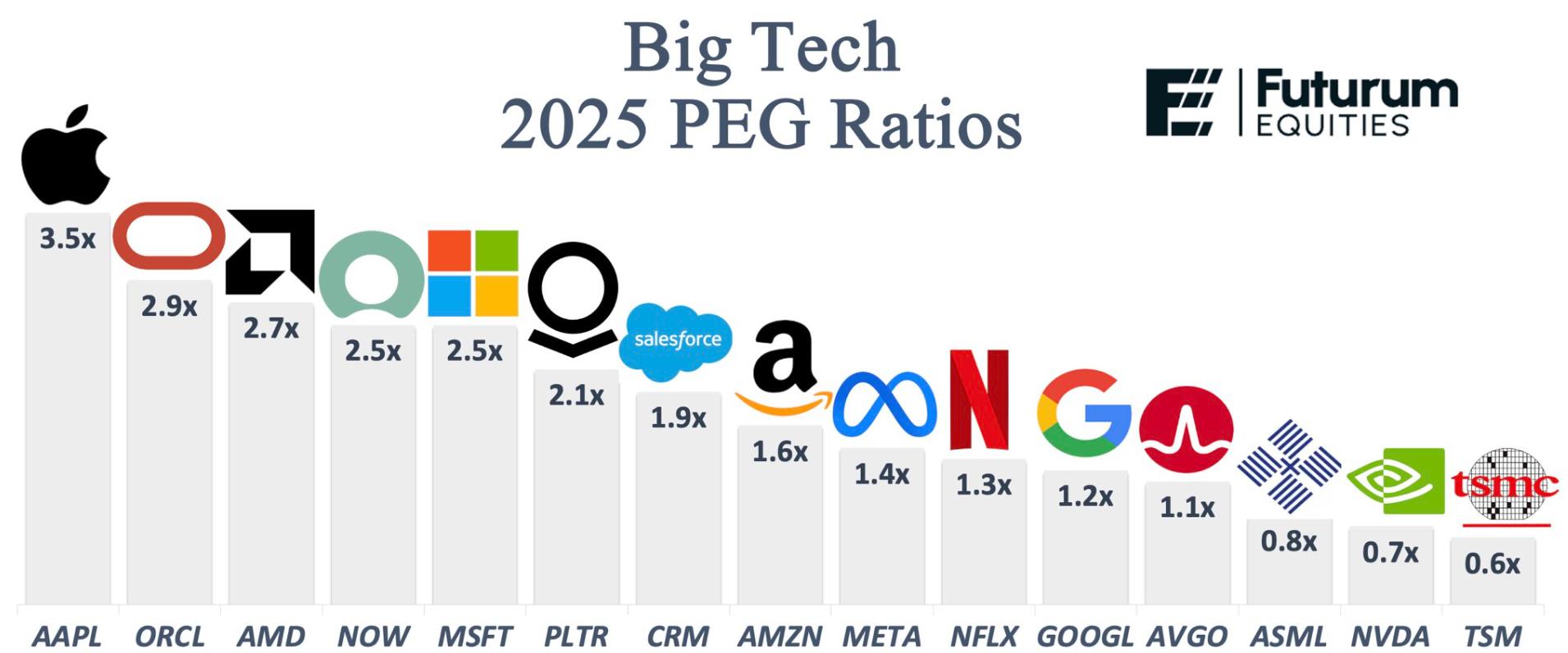

Currently, Amazon's PEG ratio is in a reasonably conservative range. The market's biggest concern—AWS growth slowdown—has been thoroughly alleviated in this report, while advertising and core e-commerce also performed steadily. Despite operating profit "missing" due to massive one-time charges and short-term impacts like AWS outages, Amazon's long-term fundamentals remain rock-solid.

Going forward, Amazon will continue heavy investments, especially in artificial intelligence. Management believes AI holds enormous opportunities and will deliver substantial long-term returns. Capital expenditures for fiscal 2025 are expected to reach $125 billion, above analysts' forecast of $118.7 billion, with further growth projected for 2026 to support doubling AWS compute capacity by 2027. As Amazon entered this AI investment cycle relatively late—unlike Microsoft, whose Capex growth is already moderating—Amazon is currently in its investment peak and ramp-up phase to match surging demand. In the AI wave, Amazon has shifted from "follower" to "leader," with long-term growth potential worth betting on.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.